|

市場調查報告書

商品編碼

1928976

干涉合成孔徑雷達市場機會、成長要素、產業趨勢分析及2026年至2035年預測Interferometric Synthetic Aperture Radar (InSAR) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球干涉合成孔徑雷達(InSAR)市場預計到 2025 年將達到 5.692 億美元,到 2035 年將達到 15 億美元,年複合成長率為 10%。

這一成長軌蹟的驅動力源於對高精度地表監測日益成長的需求、雷達數據與人工智慧、機器學習和雲端分析技術的融合,以及其在能源、自然資源和公共部門航太專案中的廣泛應用。具備頻繁重訪能力的衛星星系的日益普及,持續提升了資料的可用性和監測精度。該技術能夠提供不受天氣或光照條件影響的一致、廣域測量數據,這使其在長期規劃、風險緩解和資產管理中的重要性日益凸顯。隨著分析平台的日趨成熟,各組織機構越來越依賴干涉合成孔徑雷達的洞察數據來支援預測建模和營運決策。政府支持的觀測項目和商業性應用增強了市場的擴充性,而處理技術和平台整合的持續創新則擴大了其在各行業的應用範圍。這些因素共同促成了乾涉合成孔徑雷達成為支援基礎設施韌性、環境監測和全球戰略規劃的關鍵地理空間情報工具。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 5.692億美元 |

| 預測金額 | 15億美元 |

| 複合年成長率 | 10% |

由於干涉雷達能夠探測地表隨時間推移發生的細微變化,因此持續維護和監測應用正加速普及。持續觀測有助於制定預防性維護計劃,降低結構故障的可能性,減少長期維修成本,並增強災害應對策略。在能源和資源領域,該技術發揮日益重要的作用,它能夠精確測量作業區域周圍的地面運動,從而幫助實現安全目標,最大限度地減少環境影響,並提高合規性。大規模監測增強了預測性維護和運作風險評估,同時減少了對人工巡檢的依賴。

截至2025年,雙影像合成孔徑雷達市場規模達3.317億美元。該技術因其實施成本低、處理簡單以及在形變和穩定性評估方面具有可靠的精度而廣泛應用。對於許多用戶而言,它在解析度品質和高效工作流程之間取得了良好的平衡,無需採用更複雜的多影像技術。

機載和天載平台是主要的應用類別,到 2025 年市場規模將達到 3.225 億美元。這些平台提供廣泛的地理覆蓋範圍和一致的觀測週期,使其成為需要頻繁數據更新和廣域可視性的大規模監視和國家觀測舉措必不可少的工具。

預計到2025年,北美干涉合成孔徑雷達(InSAR)市場佔有率將達到33.5%,並透過對先進分析、太空技術和監視解決方案的持續投資,保持主導地位。公共和商業領域的廣泛應用,正在提升對高解析度雷達資料集和分析服務的需求,進一步鞏固了該地區市場的優勢。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 基礎設施監控和維護

- 與人工智慧、機器學習和雲端分析的整合

- 石油、天然氣和採礦應用

- 國防和政府航太計劃

- 衛星星系和頻繁重訪

- 挑戰與困難

- 安裝和系統成本高昂

- 技術複雜性和技能要求

- 機會:

- 基礎設施韌性與智慧城市計劃

- 環境監測與災害管理

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 新興經營模式

- 合規要求

- 永續發展計劃

- 供應鏈韌性

- 地緣政治分析

- 數位轉型

- 併購和策略聯盟

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 主要企業的競爭標竿分析

- 產品系列比較

- 產品線的廣度

- 科技

- 創新

- 按地區分類的企業發展比較

- 全球企業發展分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導企業

- 受讓人

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 產品系列比較

- 2022-2025 年主要發展動態

- 併購

- 合作夥伴關係和合資企業

- 技術進步

- 擴張與投資策略

- 永續發展計劃

- 數位轉型計劃

- 新興/Start-Ups競賽的趨勢

第5章 按類型分類的市場估算與預測,2022-2035年

- 兩幅合成孔徑雷達(SAR)影像

- 多幅合成孔徑雷達(SAR)影像

第6章 2022-2035年各平台市場估算與預測

- 機載和星載

- 地面類型

- 其他

7. 2022-2035年按組件分類的市場估算與預測

- 硬體

- 軟體

- 服務

第8章 按應用領域分類的市場估算與預測,2022-2035年

- 導航

- 影響評估

- 洪水和乾旱

- 地震災害

- 露天礦

- 其他

- 監測

- 地層下陷和地殼運動

- 基礎設施穩定性

- 冰川和冰蓋

- 火山活動

- 其他

- 地圖繪製與規劃

- 其他

9. 依最終用途分類的市場估計與預測,2022-2035 年

- 航太/國防

- 農業

- 土木工程/建築

- 環境監測

- 礦業

- 石油和天然氣

- 其他

第10章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第11章:公司簡介

- 主要企業

- Airbus Defence and Space

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Raytheon Technologies

- Thales Group

- BAE Systems

- Leonardo SpA

- L3 Harris Technologies

- 按地區分類的主要企業

- 北美洲

- Capella Space

- MDA Ltd.

- Orbital Insight

- SkyGeo

- 歐洲

- GAMMA Remote Sensing AG

- CGG

- Tre Altamira

- Tele-Rilevamento Europa

- sarmap SA

- 亞太地區

- ICEYE

- Synspective

- 北美洲

- 小眾/顛覆性公司

- 3vGeomatics

- GroundProbe

- PCI Geomatics

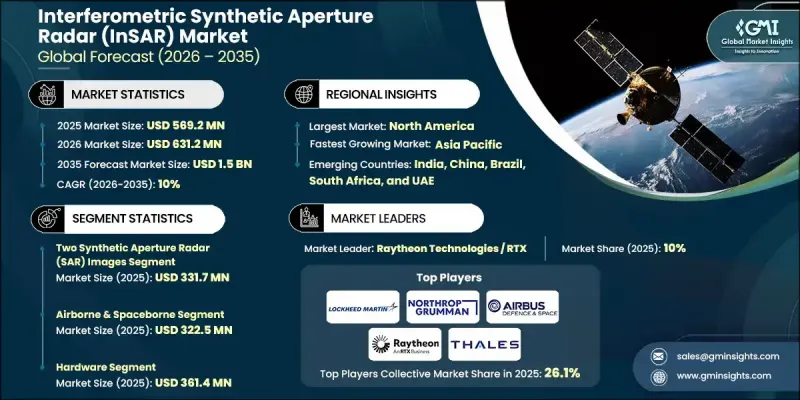

The Global Interferometric Synthetic Aperture Radar (InSAR) Market was valued at USD 569.2 million in 2025 and is estimated to grow at a CAGR of 10% to reach USD 1.5 billion by 2035.

The growth trajectory is driven by rising demand for high-precision surface monitoring, the convergence of radar data with artificial intelligence, machine learning, and cloud-based analytics, and expanding use across energy, natural resource, and public-sector space initiatives. The increasing deployment of satellite constellations with frequent revisit capabilities continues to enhance data availability and improve monitoring accuracy. Technology's ability to deliver consistent, large-area measurements regardless of weather or lighting conditions has elevated its importance for long-term planning, risk mitigation, and asset management. As analytical platforms mature, organizations increasingly rely on interferometric radar insights to support predictive modeling and operational decision-making. Government-backed observation programs and commercial adoption are reinforcing market scalability, while continuous innovation in processing techniques and platform integration is expanding accessibility across industries. These combined factors position interferometric synthetic aperture radar as a critical geospatial intelligence tool supporting infrastructure resilience, environmental oversight, and strategic planning worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $569.2 Million |

| Forecast Value | $1.5 Billion |

| CAGR | 10% |

Ongoing maintenance and monitoring applications are accelerating adoption due to the capability of interferometric radar to detect minute surface changes over time. Continuous observation supports proactive maintenance planning, lowers the probability of structural failures, reduces long-term repair costs, and strengthens disaster readiness strategies. In the energy and resource sectors, technology plays a growing role by enabling precise measurement of land movement around operational zones, supporting safety objectives, minimizing environmental exposure, and improving regulatory compliance. Large-scale monitoring reduces dependence on manual inspections while enhancing predictive maintenance and operational risk assessment.

The two-image synthetic aperture radar segment reached USD 331.7 million in 2025. This method remains widely adopted due to its lower implementation costs, reduced processing complexity, and reliable accuracy for deformation and stability assessments. For many users, the balance between resolution quality and streamlined workflows eliminates the need for more complex multi-image techniques.

The airborne and spaceborne platforms formed the leading deployment category, generating USD 322.5 million in 2025. These platforms support extensive geographic coverage and consistent observation cycles, making them essential for large-scale monitoring and national observation initiatives that require frequent data updates and broad visibility.

North America Interferometric Synthetic Aperture Radar (InSAR) Market accounted for 33.5% share in 2025, maintaining leadership through sustained investment in advanced analytics, space technologies, and monitoring solutions. Strong adoption across public agencies and commercial sectors has increased demand for high-resolution radar datasets and analytical services, reinforcing regional market strength.

Key companies active in the Global Interferometric Synthetic Aperture Radar (InSAR) Market include Airbus Defence and Space, ICEYE, Capella Space, Lockheed Martin Corporation, Northrop Grumman Corporation, Leonardo S.p.A., Thales Group, Raytheon Technologies, L3Harris Technologies, BAE Systems, MDA Ltd., Synspective, GAMMA Remote Sensing AG, CGG, GroundProbe, Orbital Insight, PCI Geomatics, SkyGeo, sarmap SA, Tre Altamira, Tele-Rilevamento Europa, and 3vGeomatics. Companies in the Global Interferometric Synthetic Aperture Radar (InSAR) Market strengthen their competitive position through continuous technology innovation, expansion of satellite and airborne capabilities, and integration of advanced analytics. Strategic investments in AI-driven data processing and cloud-based delivery platforms improve scalability and customer accessibility. Partnerships with government agencies, infrastructure operators, and energy companies help secure long-term contracts and recurring revenue streams.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Platform trends

- 2.2.3 Component trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Infrastructure monitoring & maintenance

- 3.2.1.2 Integration with AI, ML, and cloud analytics

- 3.2.1.3 Oil, gas & mining applications

- 3.2.1.4 Defense & government space programs

- 3.2.1.5 Satellite constellations & high-frequency revisit

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 High deployment & system costs

- 3.2.2.2 Technical complexity & skill requirements

- 3.2.3 Opportunities:

- 3.2.3.1 Infrastructure Resilience & Smart City Projects

- 3.2.3.2 Environmental Monitoring & Disaster Management

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Sustainability Initiatives

- 3.11 Supply Chain Resilience

- 3.12 Geopolitical Analysis

- 3.13 Digital Transformation

- 3.14 Mergers, Acquisitions, and Strategic Partnerships Landscape

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Two Synthetic Aperture Radar (SAR) Images

- 5.3 Multiple Synthetic Aperture Radar (SAR) Images

Chapter 6 Market Estimates and Forecast, By Platform, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Airborne & spaceborne

- 6.3 Ground-based

- 6.4 Others

Chapter 7 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Hardware

- 7.3 Software

- 7.4 Services

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Navigation

- 8.3 Impact assessment

- 8.3.1 Flood and drought

- 8.3.2 Seismic hazard

- 8.3.3 Open-pit mine

- 8.3.4 Others

- 8.4 Monitoring

- 8.4.1 Subsidence & field

- 8.4.2 Infrastructure stability

- 8.4.3 Glacier and ice sheet

- 8.4.4 Volcanic activity

- 8.4.5 Others

- 8.5 Mapping & planning

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By End use, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Aerospace & defense

- 9.3 Agriculture

- 9.4 Civil engineering & construction

- 9.5 Environmental monitoring

- 9.6 Mining

- 9.7 Oil & gas

- 9.8 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Airbus Defence and Space

- 11.1.2 Lockheed Martin Corporation

- 11.1.3 Northrop Grumman Corporation

- 11.1.4 Raytheon Technologies

- 11.1.5 Thales Group

- 11.1.6 BAE Systems

- 11.1.7 Leonardo S.p.A.

- 11.1.8. L3 Harris Technologies

- 11.2 Regional Key Players

- 11.2.1 North America

- 11.2.1.1 Capella Space

- 11.2.1.2 MDA Ltd.

- 11.2.1.3 Orbital Insight

- 11.2.1.4 SkyGeo

- 11.2.2 Europe

- 11.2.2.1 GAMMA Remote Sensing AG

- 11.2.2.2 CGG

- 11.2.2.3 Tre Altamira

- 11.2.2.4 Tele-Rilevamento Europa

- 11.2.2.5 sarmap SA

- 11.2.3 Asia Pacific

- 11.2.3.1 ICEYE

- 11.2.3.2 Synspective

- 11.2.1 North America

- 11.3 Niche / Disruptors

- 11.3.1 3vGeomatics

- 11.3.2 GroundProbe

- 11.3.3 PCI Geomatics

合成孔徑雷達市場:依產品、平台、頻段及應用分類-2026-2032年全球市場預測

合成孔徑雷達市場:依產品、平台、頻段及應用分類-2026-2032年全球市場預測 2026年全球合成孔徑雷達市場報告合成孔徑雷達衛星市場:按應用、最終用戶、軌道類型、頻段和組件分類的全球預測(2026-2032年)

2026年全球合成孔徑雷達市場報告合成孔徑雷達衛星市場:按應用、最終用戶、軌道類型、頻段和組件分類的全球預測(2026-2032年) 太空領域合成孔徑雷達市場:依平台、頻段、應用和地區分類

太空領域合成孔徑雷達市場:依平台、頻段、應用和地區分類 全球合成孔徑雷達市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球合成孔徑雷達市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 星載合成孔徑雷達 (SAR) 資料和服務市場:依頻段(X 波段、L 波段、C 波段、S 波段)、成像模式(聚束、條帶、掃描 SAR)、組件、應用和最終用戶劃分 - 全球預測至 2036 年

星載合成孔徑雷達 (SAR) 資料和服務市場:依頻段(X 波段、L 波段、C 波段、S 波段)、成像模式(聚束、條帶、掃描 SAR)、組件、應用和最終用戶劃分 - 全球預測至 2036 年 合成孔徑雷達市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、平台、頻段、地區和競爭格局分類,2021-2031年

合成孔徑雷達市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、平台、頻段、地區和競爭格局分類,2021-2031年 合成孔徑雷達市場規模、佔有率和成長分析(按組件、平台、頻寬、模式、應用和地區分類)—產業預測(2026-2033 年)合成孔徑雷達 (SAR) 成像市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測 (2024-2032)

合成孔徑雷達市場規模、佔有率和成長分析(按組件、平台、頻寬、模式、應用和地區分類)—產業預測(2026-2033 年)合成孔徑雷達 (SAR) 成像市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測 (2024-2032) 合成孔徑雷達市場規模、佔有率和趨勢分析報告:2024-2030 年按組件、平台、頻段、模式、應用、區域和細分市場進行的預測

合成孔徑雷達市場規模、佔有率和趨勢分析報告:2024-2030 年按組件、平台、頻段、模式、應用、區域和細分市場進行的預測