|

市場調查報告書

商品編碼

1928949

工業滅菌設備市場機會、成長要素、產業趨勢分析及2026年至2035年預測Industrial Pasteurizers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

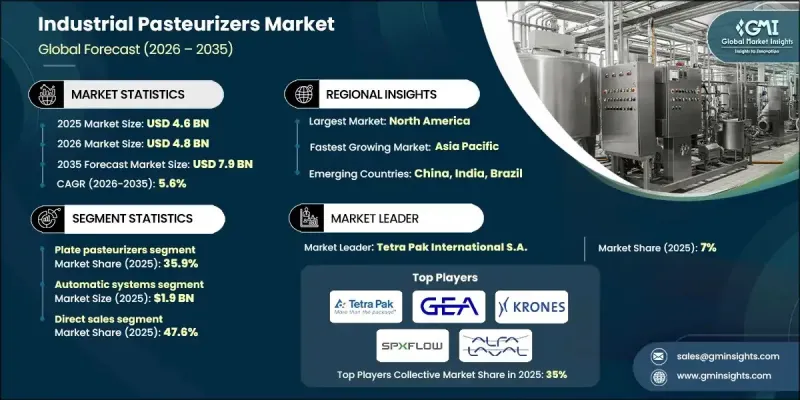

全球工業滅菌設備市場預計到 2025 年將達到 46 億美元,到 2035 年將達到 79 億美元,年複合成長率為 5.6%。

市場擴張得益於人們對食品安全、營運效率和永續加工方法的日益重視。主要製造商之間不斷加劇的整合活動也影響著競爭格局,併購活動增強了創新能力並拓展了產品線。同時,傳統的手工熱處理流程日益被認為效率低且對環境有害。現代熱處理解決方案越來越受歡迎,因為先進的熱回收和再生系統能夠最大限度地減少能源消耗並降低對環境的影響。這些技術與流質食品生產產業普遍採用的永續性目標高度契合。北美對自動化液體處理和無菌填充設備的需求持續成長,而歐洲和亞太部分地區對食品飲料基礎設施的投資增加,也提高了工業滅菌設備在當地市場的商業性可行性。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 46億美元 |

| 預測金額 | 79億美元 |

| 複合年成長率 | 5.6% |

到 2025 年,板式滅菌器市佔率將達到 35.9%。由於這些系統能夠在保持高效傳熱和降低能耗的同時處理大量物料,因此它們將繼續廣泛應用,尤其是在流質食品生產環境中。

預計到2025年,自動化滅菌系統細分市場將佔據42.3%的市場佔有率,並創造19億美元的收入。自動化正日益普及,因為它能夠提高生產效率、改善營運安全性並降低對勞動力的依賴。先進的控制技術提高了系統的精度和可靠性,有助於企業在受監管行業中滿足嚴格的品質和安全標準。

受自動化食品加工領域強勁投資和高階飲料生產擴張的推動,美國工業巴氏殺菌機市場預計到2035年將維持5.8%的複合年成長率。巴氏殺菌機在大規模乳製品分銷網路中發揮關鍵作用,而自動化、高速加工解決方案在這些網路中的應用正日益普及。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 產業影響因素

- 促進要素

- 潔淨標示和機能飲料的激增

- 嚴格的食品安全標準和《食品安全現代化法案》(FSMA)法規

- 永續性和熱效率

- 產業潛在風險與挑戰

- 初始投資額高,投資回收期長

- 現有設施維修的複雜性

- 機會

- 數位雙胞胎和即時監測

- 混合式和模組化滅菌器

- 促進要素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按類型

- 監管環境

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 依產品類型分類的市場估算與預測,2022-2035年

- 板式滅菌器

- 隧道式滅菌器

- 大量滅菌器

- 高溫短時 (HTST) 系統

- 其他

6. 2022-2035年按營運方式分類的市場估計與預測

- 手動的

- 半自動

- 自動的

第7章 按技術分類的市場估計與預測,2022-2035年

- 電動消毒器

- 瓦斯消毒器

- 蒸氣消毒器

第8章 依產能分類的市場估計與預測,2022-2035年

- 少於1000公升

- 1000至5000公升

- 超過5000公升

第9章 按應用領域分類的市場估算與預測,2022-2035年

- 乳製品業

- 牛奶和奶油

- 乳酪生產

- 優格生產

- 冰淇淋加工

- 飲料業

- 酒精飲料

- 不含酒精的飲料

- 食品加工

- 其他(藥品、寵物食品等)

第10章 按分銷管道分類的市場估算與預測,2022-2035年

- 直接地

- 間接

第11章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- Alfa Laval AB

- Dion Engineering

- Feldmeier Equipment, Inc.

- GEA Group AG

- Hiperbaric

- HRS Heat Exchangers

- IDMC Limited

- JBT Corporation

- KHS Group

- Krones AG

- Milkron GmbH

- Paul Mueller Company

- Sidel

- SPX FLOW, Inc.

- Tetra Pak International SA

The Global Industrial Pasteurizers Market was valued at USD 4.6 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 7.9 billion by 2035.

Market expansion is supported by rising awareness around food safety, operational efficiency, and sustainable processing practices. Growing consolidation activity among leading manufacturers is also influencing the competitive landscape, as mergers and acquisitions are strengthening innovation capabilities and expanding product offerings. At the same time, traditional manual heat treatment processes are increasingly viewed as inefficient and environmentally burdensome. Modern thermal processing solutions are gaining preference due to their ability to minimize energy usage and reduce environmental impact through advanced heat recovery and regenerative systems. These technologies align closely with the sustainability goals adopted across the liquid food production industry. Demand for automated liquid processing and aseptic filling facilities continues to rise in North America, while increasing investments in food and beverage infrastructure across Europe and parts of the Asia Pacific region are improving the commercial viability of industrial pasteurization equipment in local markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.6 Billion |

| Forecast Value | $7.9 Billion |

| CAGR | 5.6% |

The plate-based pasteurizers segment held 35.9% share in 2025. These systems remain widely adopted due to their ability to handle large processing volumes while maintaining efficient heat transfer and reduced energy consumption, particularly in liquid food production environments.

The automatic pasteurization systems segment accounted for 42.3% share in 2025 and generated USD 1.9 billion. Automation is increasingly favored as it enhances throughput, improves operational safety, and lowers labor dependency. Advanced control technologies are improving system accuracy and reliability, supporting compliance with strict quality and safety standards across regulated industries.

U.S. Industrial Pasteurizers Market held 5.8% CAGR through 2035, supported by strong investments in automated food processing and the expansion of premium beverage production. Pasteurization equipment plays a critical role in large-scale dairy distribution networks, where automated high-speed processing solutions are seeing increased adoption.

Leading companies active in the Global Industrial Pasteurizers Market include Tetra Pak International S.A., GEA Group AG, Alfa Laval AB, SPX FLOW, Inc., Krones AG, Sidel, JBT Corporation, KHS Group, Paul Mueller Company, Feldmeier Equipment, Inc., Milkron GmbH, HRS Heat Exchangers, IDMC Limited, Dion Engineering, and Hiperbaric. Companies operating in the Industrial Pasteurizers Market are reinforcing their market positions through technology upgrades, strategic partnerships, and portfolio diversification. Manufacturers are investing in energy-efficient designs and automation-ready systems to meet evolving customer requirements. Expansion into emerging markets and localized manufacturing strategies are helping improve market reach and cost competitiveness. Continuous investment in research and development is enabling companies to enhance system performance, reliability, and compliance with food safety standards.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Operation

- 2.2.4 Technology

- 2.2.5 Capacity

- 2.2.6 Application

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in clean-label and functional beverages

- 3.2.1.2 Strict food safety and FSMA regulations

- 3.2.1.3 Sustainability and thermal efficiency

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial CAPEX & long ROI

- 3.2.2.2 Complexity of retrofitting legacy sites

- 3.2.3 Opportunities

- 3.2.3.1 Digital twins and real-time monitoring

- 3.2.3.2 Hybrid and modular pasteurization units

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter';s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Plate pasteurizers

- 5.3 Tunnel pasteurizers

- 5.4 Batch pasteurizers

- 5.5 HTST (high temperature short time) systems

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Operation, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Semi-automatic

- 6.4 Automatic

Chapter 7 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Electric pasteurizers

- 7.3 Gas pasteurizers

- 7.4 Steam pasteurizers

Chapter 8 Market Estimates and Forecast, By Capacity, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Below 1000 litres

- 8.3 Between 1000-5000 litres

- 8.4 Above 5000 litres

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Dairy industry

- 9.2.1 Milk and cream

- 9.2.2 Cheese production

- 9.2.3 Yogurt manufacturing

- 9.2.4 Ice cream processing

- 9.3 Beverage industry

- 9.3.1 Alcoholic beverage

- 9.3.2 Non-Alcoholic beverage

- 9.4 Food processing

- 9.5 Others (pharmaceuticals, pet food, etc.)

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct

- 10.3 Indirect

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Alfa Laval AB

- 12.2 Dion Engineering

- 12.3 Feldmeier Equipment, Inc.

- 12.4 GEA Group AG

- 12.5 Hiperbaric

- 12.6 HRS Heat Exchangers

- 12.7 IDMC Limited

- 12.8 JBT Corporation

- 12.9 KHS Group

- 12.10 Krones AG

- 12.11 Milkron GmbH

- 12.12 Paul Mueller Company

- 12.13 Sidel

- 12.14 SPX FLOW, Inc.

- 12.15 Tetra Pak International S.A.

乳品巴氏殺菌設備市場按類型、行動/固定式、技術、應用和最終用戶分類-2025-2032年全球預測

乳品巴氏殺菌設備市場按類型、行動/固定式、技術、應用和最終用戶分類-2025-2032年全球預測 全球工業巴氏殺菌機市場

全球工業巴氏殺菌機市場 巴氏滅菌器和滅菌器市場機會、成長動力、產業趨勢分析和 2024 - 2032 年預測

巴氏滅菌器和滅菌器市場機會、成長動力、產業趨勢分析和 2024 - 2032 年預測