|

市場調查報告書

商品編碼

1928936

天然油多元醇市場機會、成長要素、產業趨勢分析及2026年至2035年預測Natural Oil Polyols Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

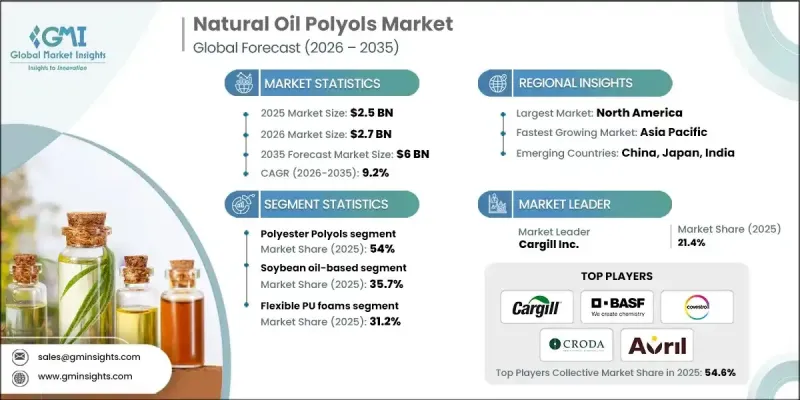

全球天然油多元醇市場預計到 2025 年將達到 25 億美元,到 2035 年將達到 60 億美元,年複合成長率為 9.2%。

市場成長要素來自日益嚴格的環境法規、消費者對永續產品日益成長的需求,以及在汽車、建築、家具和工業等領域不斷擴大的應用。製造商正致力於研發生物基配方技術,以提升產品的機械、熱學和化學性能,從而在實現高性能應用的同時減少碳排放。在全球環境法規不斷演變和消費者對社會責任日益重視的推動下,對環保解決方案的需求不斷成長,加速了生物基多元醇的應用。各行業正積極將天然來源的多元醇應用於聚氨酯泡棉、黏合劑、塗料和彈性體的生產,以提高永續性並減少碳足跡。用於高階泡棉、塗料、黏合劑和彈性體應用的生物基多元醇的最新進展,正幫助企業實現產品系列多元化,進軍高階產品市場,並推動環保生產和採購流程的創新。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 25億美元 |

| 預測金額 | 60億美元 |

| 複合年成長率 | 9.2% |

預計從 2025 年到 2035 年,聚醚多元醇市場將以 10.3% 的複合年成長率成長。這一成長得益於消費者對永續、高性能材料(尤其是在汽車應用領域)日益成長的興趣,以及生物基配方技術和可客製化多元醇功能的進步。

預計到 2025 年,軟性聚氨酯泡棉市佔率將達到 31.2%,到 2035 年將以 7.1% 的複合年成長率成長。該細分市場受益於泡棉的柔軟性、回彈性和環保特性,使其在床墊、靠墊和座椅等應用中廣受歡迎。

預計2025年,北美天然油多元醇市場規模將達到8.218億美元,並在預測期內保持強勁成長。美國和加拿大對永續材料的高接受度推動了對用於聚氨酯泡棉、黏合劑、塗料和密封劑的生物基多元醇的需求。政府支持綠色化學的舉措以及強大的研發生態系統進一步鞏固了該地區的市場領先地位,並促進了環保替代品的採用。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 多個產業對環境永續多元醇的需求不斷成長

- 增加柔軟性及硬質聚氨酯泡棉。

- 政府獎勵促進生物基化學品和產品的推廣

- 產業潛在風險與挑戰

- 與石油基多元醇相比,生產成本較高

- 穩定、高品質的原料供應有限

- 與合成多元醇相比,其性能存在技術局限性

- 市場機遇

- 對油漆、黏合劑、密封劑和彈性體的需求不斷成長

- 人們對綠色建築材料的興趣日益濃厚,並且廣泛應用。

- 擴大全球生物基化學品市場

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利狀態

- 貿易統計(HS編碼)(註:僅提供主要國家的貿易統計)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續努力

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 考慮到碳足跡

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 按類型分類的市場估算與預測,2022-2035年

- 聚酯多元醇

- 聚醚多元醇

6. 2022-2035年按來源分類的市場估計與預測

- 大豆油基

- 蓖麻油基

- 棕櫚油基

- 菜籽/菜籽油

- 葵花籽油基底

- 其他

第7章 按應用領域分類的市場估算與預測,2022-2035年

- 軟聚氨酯泡棉

- 硬質聚氨酯泡棉

- 塗層

- 黏合劑

- 密封劑

- 彈性體

- 其他

第8章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- BASF SE

- Biobased Technologies LLC

- Cargill, Incorporated

- Covestro AG

- Croda International Plc

- Econic Technologies

- Emery Oleochemicals

- Global Bio-chem Technology Group

- Oleon Novance(arvil)

- The Dow Chemical Company

The Global Natural Oil Polyols Market was valued at USD 2.5 billion in 2025 and is estimated to grow at a CAGR of 9.2% to reach USD 6 billion by 2035.

The market is driven by stricter environmental regulations, rising consumer demand for sustainable products, and increasing use across automotive, construction, furniture, and industrial sectors. Manufacturers are focusing on bio-based formulations that improve mechanical, thermal, and chemical performance, enabling high-performance applications while reducing carbon emissions. The growing demand for eco-friendly solutions has accelerated the adoption of bio-polyols, fueled by global environmental legislation and consumer preference for socially responsible products. Industries are increasingly incorporating natural polyols in the production of polyurethane foams, adhesives, coatings, and elastomers to enhance sustainability and reduce their carbon footprint. Recent developments include bio-based polyols for premium foam, coating, adhesive, and elastomer applications, allowing companies to diversify portfolios, enter high-end product markets, and drive innovation in eco-conscious production and procurement processes.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.5 Billion |

| Forecast Value | $6 Billion |

| CAGR | 9.2% |

The polyether polyols segment is forecasted to grow at a CAGR of 10.3% between 2025 and 2035. Growth is supported by increasing consumer focus on sustainable, high-performance materials, especially in automotive applications, along with advances in bio-based formulation technologies and customizable polyol functionality.

The flexible polyurethane foams segment held a 31.2% share in 2025 and is expected to grow at a CAGR of 7.1% by 2035. The segment benefits from the foam's softness, resilience, and eco-friendly properties, making it popular in applications like mattresses, cushions, and seating.

North America Natural Oil Polyols Market reached USD 821.8 million in 2025 and is expected to show robust growth during the forecast period. The high adoption of sustainable materials in the U.S. and Canada drives demand for bio-based polyols used in PU foams, adhesives, coatings, and sealants. Government initiatives supporting green chemistry and strong R&D ecosystems further strengthen the region's market leadership and adoption of eco-friendly alternatives.

Major players operating in the Global Natural Oil Polyols Market include BASF SE, Biobased Technologies LLC, Cargill, Incorporated, Covestro AG, Croda International Plc, Econic Technologies, Emery Oleochemicals, Global Bio-chem Technology Group, Oleon Novance (Arvil), and The Dow Chemical Company. Companies in the Natural Oil Polyols Market are employing strategies to expand their market presence by focusing on R&D for high-performance, bio-based polyols and diversifying their product portfolios for premium applications. Collaborations with automotive, construction, and industrial manufacturers are boosting adoption across sectors. Firms are investing in sustainable production processes to reduce carbon footprints and improve eco-certifications, enhancing brand reputation. Regional expansion into North America, Europe, and Asia Pacific, combined with strategic acquisitions, strengthens market foothold.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Source

- 2.2.4 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for eco-friendly and sustainable polyols across multiple industries

- 3.2.1.2 Increasing usage of polyols in flexible and rigid polyurethane foams

- 3.2.1.3 Government incentives promoting bio-based chemicals and products

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs compared to petroleum-based polyols

- 3.2.2.2 Limited availability of consistent, high-quality feedstocks

- 3.2.2.3 Technical limitations in performance compared to synthetic polyols

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand in coatings, adhesives, sealants, and elastomers

- 3.2.3.2 Increasing awareness and adoption of green building materials

- 3.2.3.3 Expansion of global bio-based chemical market

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polyester Polyols

- 5.3 Polyether Polyols

Chapter 6 Market Estimates and Forecast, By Source, 2022-2035 (USD billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Soybean Oil-Based

- 6.3 Castor Oil-Based

- 6.4 Palm Oil-Based

- 6.5 Canola/Rapeseed Oil-Based

- 6.6 Sunflower Oil-Based

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Flexible PU Foams

- 7.3 Rigid PU Foams

- 7.4 Coatings

- 7.5 Adhesives

- 7.6 Sealants

- 7.7 Elastomers

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 BASF SE

- 9.2 Biobased Technologies LLC

- 9.3 Cargill, Incorporated

- 9.4 Covestro AG

- 9.5 Croda International Plc

- 9.6 Econic Technologies

- 9.7 Emery Oleochemicals

- 9.8 Global Bio-chem Technology Group

- 9.9 Oleon Novance (arvil)

- 9.10 The Dow Chemical Company