|

市場調查報告書

商品編碼

1928919

林業潤滑劑市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)Forestry Lubricants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

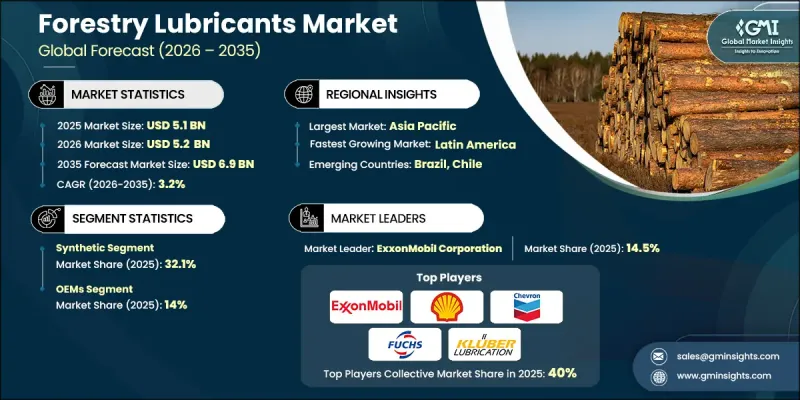

全球林業潤滑油市場預計到 2025 年將達到 51 億美元,到 2035 年將達到 69 億美元,年複合成長率為 3.2%。

市場擴張的驅動力在於林業作業中高度機械化和先進設備的日益普及。這些設備需要專用潤滑油,以確保即使在惡劣條件下也能可靠運作。由於林業機械通常在偏遠地區運作,因計劃外設備停機造成的經濟損失促使人們採用使用壽命更長、磨損防護性能更佳的高品質潤滑油。操作人員不斷尋求能夠承受極端氣候下常見的嚴重機械應力、高溫和高濕度的解決方案。法律規範也在影響市場需求,特別是透過推廣使用環保潤滑油的政策。這些法規有望促進商業性應用,同時也有助於永續產業的就業成長。合規要求和日益增強的環保意識推動了對這類潤滑油的需求。高可再生原料含量產品的日益普及正在增強市場的長期發展勢頭,這與向永續材料和生產方式的更廣泛轉變不謀而合。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 51億美元 |

| 預測金額 | 69億美元 |

| 複合年成長率 | 3.2% |

2025年,合成潤滑油市佔率達到32.1%,預計2035年將以3.3%的複合年成長率成長。其主導地位歸功於其在嚴苛的林業環境中的卓越性能,在這些環境中,設備會承受持續的壓力、污染和長時間的運作週期。與傳統潤滑油相比,合成潤滑油具有更強的熱解和抗氧化性能,這加速了其在林業作業中的應用。

2025年,OEM(整車製造商)細分市場佔14%,預計2026年至2035年將以3.2%的複合年成長率成長。大型伐木作業中使用的多種機械系統潤滑油消耗量高,是推動此細分市場需求成長的主要因素。林業作業高度依賴可靠的潤滑系統,以確保關鍵機械和液壓系統在惡劣環境下正常運作。

預計到2025年,北美林業潤滑油市佔率將達到31%。高度機械化、先進潤滑油配方的廣泛應用以及環保法規支撐了該地區的市場需求。氣候條件以及設備製造商與潤滑油供應商之間的密切合作,進一步延長了機械設備的使用壽命,提高了作業效率。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利狀態

- 貿易統計(HS編碼)(註:僅提供主要國家的貿易統計)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續努力

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 考慮到碳足跡

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 2022-2035年按產品分類的市場估算與預測

- 合成油

- 合成油混合物

- 生物基

- 礦物油

第6章 按應用領域分類的市場估算與預測,2022-2035年

- 引擎潤滑油

- 變速箱/齒輪油

- 油壓

- 潤滑脂

- 銷軸和襯套用潤滑脂

- 軸承潤滑脂

- 鏈條油/鋸導油

- 造紙機油

- 循環油

- 專用造紙機油

- 壓縮機油

- 冷卻液/防凍液

- 其他

- 滑道油

- 防鏽抑制劑

- 開式齒輪潤滑劑

7. 依最終用途分類的市場估計與預測,2022-2035 年

- OEM

- 鋸木廠

- 造紙廠

- 木製品製造廠

- 伐木和採伐公司

- 生質能顆粒燃料廠

- 紙漿廠

- 林業承包商/經營者

- 木材運輸服務

- 其他

第8章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- Amsoil Inc.

- Bioblend Renewable Resources

- BP plc(Castrol)

- Chevron Corporation

- China Petroleum &Chemical Corporation(Sinopec Corp)

- Elba Lubrication Inc.

- Exxon Mobil Corporation

- Frontier Performance Lubricants

- Fuchs Petrolub SE

- Klondike Lubricants Corporation

- Kluber Lubrication

- Lubrizol Corporation

- Pennine Lubricants

- Petro-Canada Lubricants

- Petronas Lubricants International(PLI)

- Phillips 66 Company

- Repsol SA

- Rymax Lubricants

- Shell plc

- TotalEnergies SE

- Others

The Global Forestry Lubricants Market was valued at USD 5.1 billion in 2025 and is estimated to grow at a CAGR of 3.2% to reach USD 6.9 billion by 2035.

Market expansion is supported by the increasing deployment of advanced, highly mechanized equipment across forestry operations, which requires specialized lubricants to ensure reliable performance under demanding conditions. As forestry machinery is often operated in remote locations, the financial impact of unplanned equipment stoppages has encouraged the use of premium lubricant formulations that offer extended service life and improved wear protection. Operators consistently seek solutions that can withstand heavy mechanical stress, elevated operating temperatures, and high moisture exposure commonly encountered in extreme climatic regions. Regulatory frameworks are also shaping market demand, particularly through policies promoting the use of environmentally acceptable lubricants. These regulations are expected to support commercial adoption while contributing to employment growth within sustainable industries. Demand for such lubricants is being driven by compliance requirements and growing environmental awareness. Products with high renewable content are gaining traction, aligning with broader shifts toward sustainable materials and production practices, which is reinforcing long-term market momentum.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.1 Billion |

| Forecast Value | $6.9 Billion |

| CAGR | 3.2% |

The synthetic lubricants segment accounted for 32.1% share in 2025 and is expected to grow at a CAGR of 3.3% through 2035. Their leading position is attributed to superior performance in harsh forestry environments, where equipment is exposed to continuous stress, contamination, and extended operating cycles. Enhanced resistance to thermal breakdown and oxidation compared to conventional alternatives has accelerated adoption across forestry operations.

The OEM segment held 14% share in 2025 and is forecast to grow at a CAGR of 3.2% between 2026 and 2035. High lubricant consumption across multiple machinery systems used in core harvesting activities is driving demand in this segment. Forestry operations depend heavily on reliable lubrication to maintain the uninterrupted functionality of essential mechanical and hydraulic systems in challenging environments.

North America Forestry Lubricants Market accounted for 31% share in 2025. High levels of mechanization, widespread use of advanced lubricant formulations, and environmental regulations are supporting regional demand. Climatic conditions and close collaboration between equipment manufacturers and lubricant suppliers further contribute to extended machinery life and operational efficiency.

Key companies operating in the Global Forestry Lubricants Market include Shell plc, Exxon Mobil Corporation, BP plc (Castrol), TotalEnergies SE, Fuchs Petrolub SE, Chevron Corporation, Petro-Canada Lubricants, Amsoil Inc., Lubrizol Corporation, Phillips 66 Company, Kluber Lubrication, Petronas Lubricants International (PLI), Repsol S.A., Sinopec Corp, Rymax Lubricants, Klondike Lubricants Corporation, Frontier Performance Lubricants, Bioblend Renewable Resources, Pennine Lubricants, and Elba Lubrication Inc. Companies operating in the Global Forestry Lubricants Market are strengthening their market positions through aggressive technology development, pilot programs, and ecosystem partnerships. Many players are investing in artificial intelligence, autonomous navigation, and fleet optimization software to improve reliability and scalability. Strategic collaborations with retailers, logistics firms, and municipalities help accelerate deployment and regulatory acceptance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Application

- 2.2.4 End use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Synthetic

- 5.3 Synthetic blend oil

- 5.4 Bio-based

- 5.5 Mineral

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Engine Lubrication

- 6.3 Transmission & Gear Oils

- 6.4 Hydraulic Fluids

- 6.5 Greases

- 6.5.1 Pin & Bushing Greases

- 6.5.2 Bearing Greases

- 6.6 Chain Oils / Saw Guide Oils

- 6.7 Paper Machine Oils

- 6.7.1 Circulating Oils

- 6.7.2 Specialty Paper Machine Oils

- 6.8 Compressor Oils

- 6.9 Coolants / Antifreeze

- 6.10 Others

- 6.10.1 Slideway Oils

- 6.10.2 Rust Preventives

- 6.10.3 Open Gear Lubricants

Chapter 7 Market Estimates and Forecast, By End Use, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 OEMs

- 7.3 Sawmills

- 7.4 Paper & Paperboard Mills

- 7.5 Wood Products Manufacturing Units

- 7.6 Logging / Harvesting Companies

- 7.7 Biomass Pellet Mills

- 7.8 Pulp Mills

- 7.9 Forest Contractors / Operators

- 7.10 Timber Transport Services

- 7.11 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Amsoil Inc.

- 9.2 Bioblend Renewable Resources

- 9.3 BP plc (Castrol)

- 9.4 Chevron Corporation

- 9.5 China Petroleum & Chemical Corporation (Sinopec Corp)

- 9.6 Elba Lubrication Inc.

- 9.7 Exxon Mobil Corporation

- 9.8 Frontier Performance Lubricants

- 9.9 Fuchs Petrolub SE

- 9.10 Klondike Lubricants Corporation

- 9.11 Kluber Lubrication

- 9.12 Lubrizol Corporation

- 9.13 Pennine Lubricants

- 9.14 Petro-Canada Lubricants

- 9.15 Petronas Lubricants International (PLI)

- 9.16 Phillips 66 Company

- 9.17 Repsol S.A.

- 9.18 Rymax Lubricants

- 9.19 Shell plc

- 9.20 TotalEnergies SE

- 9.21 Others

2034年林業生物防治市場預測-全球分析(依防治劑類型、目標害蟲、森林類型、應用方法、最終用戶和地區分類)

2034年林業生物防治市場預測-全球分析(依防治劑類型、目標害蟲、森林類型、應用方法、最終用戶和地區分類) 林業潤滑油市場規模、佔有率和成長分析:按產品類型、基礎油類型、設備類型、應用、最終用戶、分銷管道和地區分類-2026-2033年產業預測

林業潤滑油市場規模、佔有率和成長分析:按產品類型、基礎油類型、設備類型、應用、最終用戶、分銷管道和地區分類-2026-2033年產業預測 全球林業潤滑劑市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球林業潤滑劑市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球林業潤滑劑市場報告

2026年全球林業潤滑劑市場報告 林業化學品市場按類型、配方、技術、應用、最終用途和通路管道分類-全球預測(2026-2032 年)林業生物防治市場依產品類型、配方、應用方法、最終用戶和通路分類,全球預測(2026-2032年)

林業化學品市場按類型、配方、技術、應用、最終用途和通路管道分類-全球預測(2026-2032 年)林業生物防治市場依產品類型、配方、應用方法、最終用戶和通路分類,全球預測(2026-2032年) 全球林業潤滑油市場

全球林業潤滑油市場