|

市場調查報告書

商品編碼

1928911

海洋雷達市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)Marine Radar Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球海洋雷達市場預計到 2025 年將達到 19.8 億美元,到 2035 年將達到 34.8 億美元,年複合成長率為 5.8%。

海上貿易量的成長和船舶擁塞加劇,推動了對可靠導航和監視系統的需求。繁忙航道上日益成長的海上事故防範意識,促使人們對先進雷達解決方案的投資不斷增加。雷達技術的持續創新加速了升級週期,而老化的商用和軍用雷達船隊則推動了雷達的更新換代需求。固態雷達解決方案因其耐用性、運作穩定性和較低的維護需求而日益受到青睞。如今,船舶雷達系統與電子海圖平台和船舶辨識技術整合得越來越頻繁,以提高情境察覺。不斷擴展的船舶交通監控服務也支撐了對沿海和陸基雷達安裝的需求。對低能見度下導航精度的日益重視,進一步提高了雷達的性能標準。船隊現代化舉措也為雷達更換的持續需求做出了貢獻。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 19.8億美元 |

| 預測金額 | 34.8億美元 |

| 複合年成長率 | 5.8% |

2025年, X波段市佔率達到44%,預計2026年至2035年將以5.3%的複合年成長率成長。這些系統廣泛應用於中短程導航、防撞和作業控制。國際海事法規強制要求總噸位超過300噸的船舶安裝雷達,這推動了該波段雷達市場的需求。

預計到 2025 年,天線部分將佔 35% 的市場佔有率,到 2035 年將以 5.3% 的複合年成長率成長。天線在雷達維護成本中佔很大一部分,因為性能精度、探測範圍和解析度高度依賴商用和漁船隊的天線品質。

預計到 2025 年,美國海洋雷達市場將佔 88% 的佔有率,達到 5.745 億美元。商業船舶、海軍行動和休閒划船的高採用率,加上嚴格的海上安全標準和密集的沿海交通,繼續支持對現代雷達系統的持續需求。

目錄

第1章調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 世界海運貿易的成長

- 更嚴格的海事安全法規

- 沿海和港口水域交通堵塞日益嚴重

- 技術升級和數位化融合

- 產業潛在風險與挑戰

- 安裝和維護成本高昂

- 擁擠海域中的訊號干擾與雜訊

- 市場機遇

- 全球老舊機隊對維修的需求日益成長

- 離岸風電和海上能源計劃的擴張

- 固態和數位雷達的應用趨勢

- 成長潛力分析

- 監管環境

- 北美洲

- 美國海岸警衛隊(USCG)雷達機載及觀測人員要求

- 美國海岸警衛隊隊(USCG) 根據《聯邦法規》第 46 篇對雷達設備核准

- 美國聯邦通訊委員會(FCC)雷達認證標準

- 加拿大運輸部海事雷達合規指南

- 歐洲

- 歐洲海事安全局 (EMSA) 的監督和執法

- 船舶設備指令 (MED) 型式核准要求

- 歐盟船旗國和港口國監管部門的雷達檢查

- 雷達設備的歐洲協調標準 (EN)

- 亞太地區

- 中國船級社(CCS)雷達型式核准標準

- 印度航運總局雷達合規條例

- 國土交通省雷達條例

- 韓國海事局(KR)雷達要求

- 東協區域海上安全和雷達協調指南

- 拉丁美洲

- 巴西海事局(ANTAQ)雷達設備標準

- 阿根廷海岸警衛隊雷達合規條例

- 墨西哥海軍和運輸部雷達法規

- 區域SOLAS實施狀況及船旗國管制

- 中東和非洲

- 阿拉伯聯合大公國聯邦交通管理局海事雷達標準

- 沙烏地阿拉伯港務局雷達要求

- 南非海事安全局 (SAMSA) 條例

- 各區域採用國際海事組織 (IMO) 和國際電工委員會 (IEC) 雷達性能標準的情況

- 北美洲

- 波特分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 生產統計

- 生產基地

- 消費中心

- 出口和進口

- 成本細分分析

- 雷達系統購置成本

- 安裝和整合成本

- 營運和維護成本

- 軟體升級和校準成本

- 監理認證和型式核准費用

- 培訓和船員熟悉成本

- 專利分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

- 海洋雷達系統結構與整合框架

- 獨立式橋樑系統與整合艦橋系統(IBS)

- 雷達與電子海圖顯示與資訊系統(ECDIS)、自動識別系統(AIS)、高階雷達定位系統(ARPA)和慣性導航系統(INS)整合

- 開放式和專有式導航系統結構

- 雷達在感測器融合環境中的作用

- OEM差異化與技術定位因素

- 檢測範圍、解析度和雜波抑制基準測試

- 區分固態雷達和磁控管雷達

- 軟體定義雷達能力

- 可靠性、平均故障間隔時間 (MTBF) 和生命週期性能指標

- 改裝和新船的需求趨勢

- SOLAS、IMO 和海軍採購標準的影響

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 企業擴張計畫和資金籌措

第5章 雷達市場估算與預測,2022-2035年

- X波段

- S波段

- C波段雷達

- 其他

第6章 按組件分類的市場估算與預測,2022-2035年

- 發送器

- 天線

- 接收器

- 處理器

- 展示

- 其他

第7章 2022-2035年各地區市場估算與預測

- 短程雷達(1至20海浬)

- 中程雷達(20-50海浬)

- 遠程雷達(50-100海裡或更遠)

第8章 按應用領域分類的市場估算與預測,2022-2035年

- 導航

- 避免碰撞

- 監控與安防

- 捕魚活動

- 沿海交通監測

- 天氣監測

- 其他

9. 依最終用途分類的市場估計與預測,2022-2035 年

- 商船

- 海軍/國防/軍艦

- 休閒船艇/遊艇

- 私人船主

- 漁船

- 其他

第10章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 荷蘭

- 瑞典

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 新加坡

- 泰國

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

第11章:公司簡介

- 世界玩家

- BAE Systems

- Furuno Electric

- Garmin

- Hensoldt

- Kongsberg Gruppen

- Leonardo

- Lockheed Martin

- Navico

- Northrop Grumman

- Raymarine

- Raytheon RTX

- Saab

- Sperry Marine

- Teledyne FLIR

- Thales

- 區域玩家

- GEM Elettronica

- JRC Nisshinbo

- Koden Electronics

- Samyung ENC

- TOKIO KEIKI

- 新興企業/顛覆者

- Alphatron Marine

- Rutter

- Terma

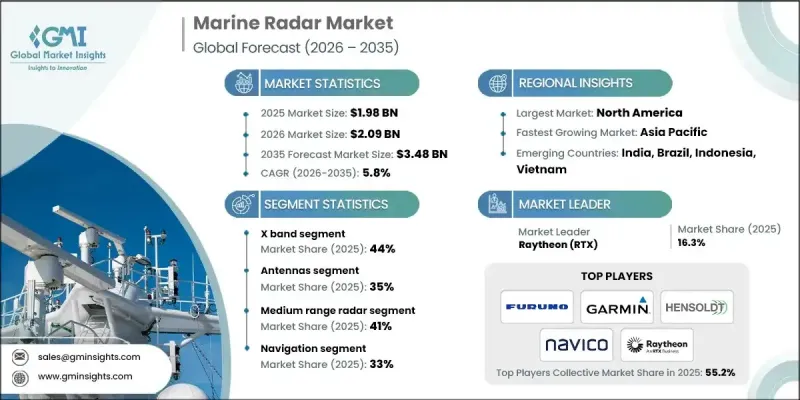

The Global Marine Radar Market was valued at USD 1.98 billion in 2025 and is estimated to grow at a CAGR of 5.8% to reach USD 3.48 billion by 2035.

Rising seaborne trade volumes and growing vessel congestion are increasing the need for reliable navigation and surveillance systems. Heightened awareness around maritime accidents in heavily trafficked waterways is encouraging greater investment in advanced radar solutions. Continuous innovation in radar technology is accelerating upgrade cycles, while aging commercial and defense fleets are driving replacement demand. Solid-state radar solutions are increasingly favored due to their durability, operational stability, and reduced maintenance needs. Marine radar systems are now more frequently integrated with electronic charting platforms and vessel identification technologies to improve situational awareness. Expansion of vessel traffic monitoring services is supporting demand for coastal and shore-based radar installations. Growing focus on navigational accuracy in poor visibility conditions is further improving radar performance standards. Fleet modernization initiatives are also contributing to sustained demand for radar replacements.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.98 Billion |

| Forecast Value | $3.48 Billion |

| CAGR | 5.8% |

The X-band segment held a 44% share in 2025 and is forecast to grow at a CAGR of 5.3% from 2026 to 2035. These systems are widely used for navigation support, collision avoidance, and operational control over short to medium ranges. International maritime regulations mandate radar installation on vessels exceeding 300 gross tons, reinforcing segment demand.

The antenna segment accounted for 35% share in 2025 and will grow at a CAGR of 5.3% through 2035. Antennas represent a major share of radar maintenance expenditure, as performance accuracy, detection range, and resolution heavily depend on antenna quality across commercial and fishing fleets.

United States Marine Radar Market held an 88% share and reached USD 574.5 million in 2025. High adoption across commercial shipping, naval operations, and recreational boating, combined with strict maritime safety standards and dense coastal traffic, continues to support ongoing demand for modern radar systems.

Key companies operating in the Global Marine Radar Market include Garmin, Furuno Electric, Raytheon RTX, Kongsberg Gruppen, Raymarine, Navico, Hensoldt, Sperry Marine, JRC Nisshinbo, and Terma. Companies in the Marine Radar Market are strengthening their competitive position by investing heavily in solid-state radar innovation and enhanced signal processing capabilities. Strategic product upgrades focused on higher resolution, improved target detection, and seamless system integration are a core priority. Manufacturers are expanding their aftermarket and service offerings to capture recurring revenue from maintenance and replacement cycles. Partnerships with shipbuilders and fleet operators are helping firms secure long-term supply agreements.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Radar

- 2.2.3 Component

- 2.2.4 Range

- 2.2.5 Application

- 2.2.6 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Growth in global seaborne trade

- 3.2.1.3 Stricter maritime safety regulations

- 3.2.1.4 Increasing traffic congestion in coastal and port waters

- 3.2.1.5 Technology upgrades and digital integration

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High installation and maintenance costs

- 3.2.2.2 Signal interference and clutter in congested waters

- 3.2.3 Market opportunities

- 3.2.3.1 Retrofit demand from aging global fleets

- 3.2.3.2 Expansion of offshore wind and offshore energy projects

- 3.2.3.3 Adoption of solid state and digital radar

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 United States Coast Guard (USCG) Radar Carriage and Observer Requirements

- 3.4.1.2 USCG Approval of Radar Equipment under 46 CFR

- 3.4.1.3 Federal Communications Commission (FCC) Radar Certification Standards

- 3.4.1.4 Canada Transport Canada Marine Radar Compliance Guidelines

- 3.4.2 Europe

- 3.4.2.1 European Maritime Safety Agency (EMSA) Oversight and Implementation

- 3.4.2.2 Marine Equipment Directive (MED) Type Approval Requirements

- 3.4.2.3 EU Flag State and Port State Control Radar Inspections

- 3.4.2.4 Harmonized EN Standards for Radar Equipment

- 3.4.3 Asia Pacific

- 3.4.3.1 China Classification Society (CCS) Radar Type Approval Standards

- 3.4.3.2 India Directorate General of Shipping Radar Compliance Rules

- 3.4.3.3 Japan Ministry of Land Infrastructure Transport Radar Regulations

- 3.4.3.4 South Korea Korean Register of Shipping Radar Requirements

- 3.4.3.5 ASEAN Regional Maritime Safety and Radar Harmonization Guidelines

- 3.4.4 Latin America

- 3.4.4.1 Brazil Maritime Authority (ANtaq) Radar Equipment Standards

- 3.4.4.2 Argentina Prefectura Naval Radar Compliance Regulations

- 3.4.4.3 Mexico Secretariat of Navy and Transport Radar Rules

- 3.4.4.4 Regional SOLAS Implementation and Flag State Controls

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE Federal Transport Authority Maritime Radar Standards

- 3.4.5.2 Saudi Arabia Ports Authority Radar Requirements

- 3.4.5.3 South Africa Maritime Safety Authority (SAMSA) Regulations

- 3.4.5.4 Regional Adoption of IMO and IEC Radar Performance Standards

- 3.4.1 North America

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.10.1 Radar system acquisition costs

- 3.10.2 Installation and integration costs

- 3.10.3 Operational and maintenance costs

- 3.10.4 Software upgrade and calibration costs

- 3.10.5 Regulatory certification and type approval costs

- 3.10.6 Training and crew familiarization costs

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Marine radar system architecture & integration framework

- 3.13.1 Standalone vs integrated bridge systems (IBS)

- 3.13.2 Radar integration with ECDIS, AIS, ARPA, and INS

- 3.13.3 Open vs proprietary navigation system architectures

- 3.13.4 Role of radar in sensor fusion environments

- 3.14 OEM differentiation & technology positioning factors

- 3.14.1 Detection range, resolution, and clutter suppression benchmarks

- 3.14.2 Solid-state vs magnetron radar differentiation

- 3.14.3 Software-defined radar capabilities

- 3.14.4 Reliability, MTBF, and lifecycle performance metrics

- 3.15 Retrofit vs newbuild demand dynamics

- 3.16 Impact of SOLAS, IMO & naval procurement standards

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Radar, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 X-band

- 5.3 S-band

- 5.4 C-Band radar

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Transmitters

- 6.3 Antennas

- 6.4 Receivers

- 6.5 Processors

- 6.6 Displays

- 6.7 Other

Chapter 7 Market Estimates & Forecast, By Range, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Short-range radar (1-20 NM)

- 7.3 Medium-range radar (20-50 NM)

- 7.4 Long-range radar (50-100 NM and above)

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Navigation

- 8.3 Collision Avoidance

- 8.4 Surveillance & Security

- 8.5 Fishing Operations

- 8.6 Monitoring Coastal Traffic

- 8.7 Weather Monitoring

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Commercial vessels

- 9.3 Naval & Defense / Military Naval

- 9.4 Recreational Boats / Yachts

- 9.5 Private boat owners

- 9.6 Fishing vessels

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.3.8 Netherlands

- 10.3.9 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Turkey

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 BAE Systems

- 11.1.2 Furuno Electric

- 11.1.3 Garmin

- 11.1.4 Hensoldt

- 11.1.5 Kongsberg Gruppen

- 11.1.6 Leonardo

- 11.1.7 Lockheed Martin

- 11.1.8 Navico

- 11.1.9 Northrop Grumman

- 11.1.10 Raymarine

- 11.1.11 Raytheon RTX

- 11.1.12 Saab

- 11.1.13 Sperry Marine

- 11.1.14 Teledyne FLIR

- 11.1.15 Thales

- 11.2 Regional Players

- 11.2.1 GEM Elettronica

- 11.2.2 JRC Nisshinbo

- 11.2.3 Koden Electronics

- 11.2.4 Samyung ENC

- 11.2.5 TOKIO KEIKI

- 11.3 Emerging Players/Disruptors

- 11.3.1 Alphatron Marine

- 11.3.2 Rutter

- 11.3.3 Terma