|

市場調查報告書

商品編碼

1928891

紡織廢棄物回收機械市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)Textile Waste Recycling Machine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

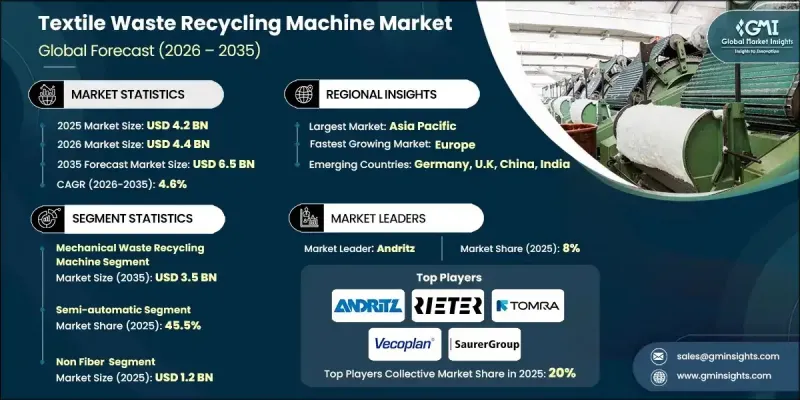

全球紡織廢棄物回收機械市場預計到 2025 年將達到 42 億美元,到 2035 年將達到 65 億美元,年複合成長率為 4.6%。

這一成長的驅動力源於人們對紡織品消費和處置的環保意識不斷增強,以及監管機構對永續生產實踐的支持力度不斷加大。業界日益重視減少廢棄物和材料回收,推動了對將廢棄紡織品轉化為可重複使用纖維的機械設備的需求。公共和私營部門為減少對掩埋的依賴和提高資源利用效率而採取的舉措,進一步促進了市場擴張。製造商正積極回應,提高產能,減少環境影響,並推動符合循環經濟目標的回收技術。此外,紡織品生產商在負責任地管理消費前和消費後廢棄物面臨的壓力不斷增加,也使該行業受益匪淺。隨著永續性成為服裝和技術紡織品行業的核心營運要求,對先進回收機械的投資持續成長,有助於市場的長期穩定發展,並促進已開發經濟體和新興經濟體的穩步普及。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 42億美元 |

| 預測金額 | 65億美元 |

| 複合年成長率 | 4.6% |

預計2025年,機械式回收設備市場規模將達23億美元,2035年將達35億美元。由於其成本效益高、能耗低,該細分市場仍是紡織廢棄物回收設備市場的支柱。機械系統能夠處理各種紡織廢棄物,因此成為尋求實用且擴充性回收解決方案的製造商的首選。

預計到2025年,半自動機械設備將佔據45.5%的市場。該細分市場之所以領先,是因為其兼具價格優勢和操作便利性。半自動系統允許操作人員在保持對核心回收流程控制的同時,實現重複性功能的自動化,從而降低勞動強度,而無需像全自動設備那樣投入大量資金。

預計2025年,美國紡織廢棄物回收機械市佔率將達90.5%。政府重視減少紡織廢棄物、制定國家回收戰略以及訂定促進回收基礎設施改善的新立法舉措,都為區域成長提供了支撐。這些措施正在推動對大規模紡織廢料回收機械的投資增加。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 產業影響因素

- 促進要素

- 對永續和環保材料的需求日益成長

- 回收技術的進步

- 政府關於紡織廢棄物的法規和政策

- 產業潛在風險與挑戰

- 前期投資和機器成本高。

- 高昂的維護和營運成本

- 機會

- 促進永續性政策和循環經濟

- 整合物聯網和預測性維護解決方案

- 促進要素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按模型

- 按地區

- 監管環境

- 標準和合規要求

- 區域法規結構

- 認證標準

- 貿易統計(HS編碼8445)

- 主要進口國

- 主要出口國

- 差距分析

- 風險評估與緩解

- 波特分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 按車型分類的市場估計與預測,2022-2035年

- 機械回收設備

- 化學回收機

- 熱回收機

第6章 按材料類型分類的市場估算與預測,2022-2035年

- 棉布

- 聚酯纖維

- 尼龍

- 羊毛

- 其他

第7章 2022-2035年各細分市場的估計與預測

- 手動的

- 半自動

- 自動的

第8章 依產能分類的市場估計與預測,2022-2035年

- 最高可達 1,000 公斤/小時

- 最高可達 2,000 公斤/小時

- 最高可達 3000 公斤/小時

- 3000公斤/小時或以上

第9章 按應用領域分類的市場估算與預測,2022-2035年

- 纖維到纖維的回收利用

- 不紡織應用

- 服裝製造

- 家用紡織品

- 技術紡織品

第10章 依採購方式分類的市場估計與預測,2022-2035年

- 消費前廢棄物

- 消費後廢棄物

第11章 按分銷管道分類的市場估算與預測,2022-2035年

- 直銷

- 間接

第12章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第13章:公司簡介

- Andritz

- Autefa Solutions

- Balkan Textile Machinery

- Dell'Orco &Villani

- HSN Machinery

- Loptex

- Margasa Projects and Textile Engineering

- Masias Machinery

- Multipro

- Rieter

- SN Surgicare and Healthcare Science

- Starlinger

- Saurer Group

- TOMRA Systems

- Vecoplan

The Global Textile Waste Recycling Machine Market was valued at USD 4.2 billion in 2025 and is estimated to grow at a CAGR of 4.6% to reach USD 6.5 billion by 2035.

Growth is driven by rising environmental awareness surrounding textile consumption and disposal, as well as stronger regulatory support for sustainable manufacturing practices. Industries are increasingly focused on minimizing waste and improving material recovery, which has accelerated demand for machinery capable of converting discarded textiles back into usable fiber forms. Public and private sector initiatives aimed at reducing landfill dependency and improving resource efficiency further support market expansion. Manufacturers are responding by advancing recycling technologies that improve throughput, reduce environmental impact, and align with circular economy goals. The industry also benefits from increasing pressure on textile producers to manage post-consumer and pre-consumer waste responsibly. As sustainability becomes a core operational requirement across apparel and industrial textile sectors, investment in advanced recycling machinery continues to rise, supporting long-term market stability and consistent adoption across developed and emerging economies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.2 Billion |

| Forecast Value | $6.5 Billion |

| CAGR | 4.6% |

The mechanical recycling machines segment generated USD 2.3 billion in 2025 and is projected to reach USD 3.5 billion by 2035. This segment remains the backbone of the textile waste recycling machine market due to its cost efficiency and lower energy requirements. Mechanical systems can process a wide range of textile waste streams, making them a preferred choice for manufacturers seeking practical and scalable recycling solutions.

The semi-automatic machines segment accounted for 45.5% share in 2025. This segment leads the market due to its balance of affordability and operational control. Semi-automatic systems allow operators to manage key recycling stages while automating repetitive functions, reducing labor intensity without the high investment associated with fully automated equipment.

United States Textile Waste Recycling Machine Market represented 90.5% share in 2025. Regional growth is supported by increased government focus on textile waste reduction, the development of national recycling strategies, and new legislative measures that encourage improved recycling infrastructure. These efforts are driving higher investment in large-scale textile recycling machinery.

Key companies operating in the Global Textile Waste Recycling Machine Market include Rieter, Andritz, Starlinger, TOMRA Systems, Saurer Group, Vecoplan, Autefa Solutions, Masias Machinery, Loptex, Balkan Textile Machinery, Dell'Orco & Villani, Margasa Projects, Textile Engineering, Multipro, HSN Machinery, and SN Surgicare and Healthcare Science. Companies in the Global Textile Waste Recycling Machine Market focus on strengthening their market position through continuous technology upgrades and sustainability-driven innovation. Manufacturers invest heavily in research and development to enhance machine efficiency, energy performance, and material recovery rates. Strategic collaborations with textile producers and waste management firms help expand customer reach and ensure long-term equipment demand. Firms also prioritize modular machine designs that allow scalability and customization based on processing needs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Machine Type

- 2.2.3 Fabric Type

- 2.2.4 Operation

- 2.2.5 Capacity

- 2.2.6 Application

- 2.2.7 Sourcing Type

- 2.2.8 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for sustainable and eco-friendly materials

- 3.2.1.2 Advancements in recycling technologies

- 3.2.1.3 Government regulations and policies on textile waste

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment and machine cost

- 3.2.2.2 High maintenance and operational costs

- 3.2.3 Opportunities

- 3.2.3.1 Sustainability policies & circular economy push

- 3.2.3.2 Integration of IoT & predictive maintenance solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By machine type

- 3.6.2 By region

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics (HS code 8445)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Gap analysis

- 3.10 Risk assessment and mitigation

- 3.11 Porter';s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Machine Type, 2022-2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Mechanical Recycling Machines

- 5.3 Chemical Recycling Machines

- 5.4 Thermal Recycling Machines

Chapter 6 Market Estimates & Forecast, By Fabric Type, 2022-2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Cotton

- 6.3 Polyester

- 6.4 Nylon

- 6.5 Wool

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Operation, 2022-2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Manual

- 7.3 Semi-automatic

- 7.4 Automatic

Chapter 8 Market Estimates & Forecast, By Capacity, 2022-2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Up to 1,000 kg/h

- 8.3 Up to 2,000 kg/h

- 8.4 Up to 3000 kg/h

- 8.5 Above 3000 kg/h

Chapter 9 Market Estimates & Forecast, By Application, 2022-2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Fiber-to-fibre Recycling

- 9.3 Non-fibre Applications

- 9.4 Apparel Manufacturing

- 9.5 Home Textiles

- 9.6 Technical Textiles

Chapter 10 Market Estimates & Forecast, By Sourcing Type, 2022-2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Pre-consumer Waste

- 10.3 Post-consumer Waste

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 Direct

- 11.3 Indirect

Chapter 12 Market Estimates & Forecast, By Region, 2022-2035 (USD Billion) (Thousand Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 France

- 12.3.3 UK

- 12.3.4 Italy

- 12.3.5 Spain

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Andritz

- 13.2 Autefa Solutions

- 13.3 Balkan Textile Machinery

- 13.4 Dell'Orco & Villani

- 13.5 HSN Machinery

- 13.6 Loptex

- 13.7 Margasa Projects and Textile Engineering

- 13.8 Masias Machinery

- 13.9 Multipro

- 13.10 Rieter

- 13.11 SN Surgicare and Healthcare Science

- 13.12 Starlinger

- 13.13 Saurer Group

- 13.14 TOMRA Systems

- 13.15 Vecoplan

食用油回收市場:依原料、製程及應用分類-2026-2032年全球市場預測

食用油回收市場:依原料、製程及應用分類-2026-2032年全球市場預測 2026年全球容器玻璃回收市場報告2026年全球廢棄物和回收市場報告2026年全球廢棄物回收再利用市場報告2026年全球廢棄物回收服務市場報告溫度控制租賃解決方案市場:按產品類型、溫度範圍、租賃期限、銷售管道、最終用戶產業和應用分類-全球預測,2026-2032年廢油回收市場按原料類型、技術類型和最終用途分類,全球預測(2026-2032年)

2026年全球容器玻璃回收市場報告2026年全球廢棄物和回收市場報告2026年全球廢棄物回收再利用市場報告2026年全球廢棄物回收服務市場報告溫度控制租賃解決方案市場:按產品類型、溫度範圍、租賃期限、銷售管道、最終用戶產業和應用分類-全球預測,2026-2032年廢油回收市場按原料類型、技術類型和最終用途分類,全球預測(2026-2032年) 廢棄物回收服務市場分析及預測(至2035年):依類型、產品類型、服務、技術、應用、材料類型、製程、最終用戶、設備分類

廢棄物回收服務市場分析及預測(至2035年):依類型、產品類型、服務、技術、應用、材料類型、製程、最終用戶、設備分類 全球酒精飲料瓶回收市場規模、佔有率、趨勢和成長分析報告(2026-2034)2026年全球化學品市場報告:循環經濟視角

全球酒精飲料瓶回收市場規模、佔有率、趨勢和成長分析報告(2026-2034)2026年全球化學品市場報告:循環經濟視角