|

市場調查報告書

商品編碼

1928889

核能機器人市場機會、成長要素、產業趨勢分析及2026年至2035年預測Nuclear Robots Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

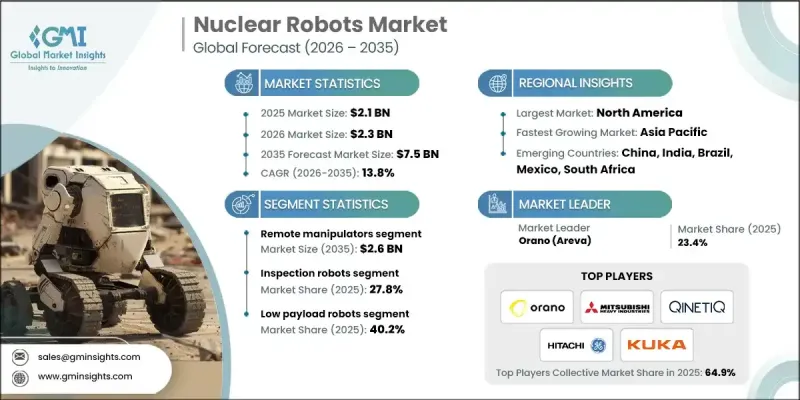

全球核能機器人市場預計到 2025 年將達到 21 億美元,到 2035 年將達到 75 億美元,年複合成長率為 13.8%。

在全球範圍內,尤其是歐洲和北美地區,老舊核能數量的不斷增加推動了市場成長。這些核子反應爐和燃料循環設施已超過設計壽命。退役這些設施需要在高放射性和危險環境中作業,因此遠端操作、檢查和廢棄物管理對於保障工人安全和遵守法規至關重要。政府和公共部門對核能安和現代化項目的投資進一步推動了對先進機器人技術的需求。核能機器人專為檢查、維護、拆除和放射性廢棄物管理而設計,可在提高精度和運作效率的同時,最大限度地減少人員暴露。人工智慧和自主技術的整合使這些機器能夠在充滿挑戰的放射性環境中自主運行,從而提高性能和安全性,並減少對專業人員的需求。退役和場地修復項目持續推動對這些先進解決方案的穩定需求。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 21億美元 |

| 預測金額 | 75億美元 |

| 複合年成長率 | 13.8% |

預計到2035年,遙控機械手臂市場規模將達26億美元。遙控機械手臂因其能夠在輻射強度高的區域安全地組裝、維護和搬運核能部件而被廣泛應用。觸覺回饋和直覺控制介面的創新提高了操作人員的精確度,同時降低了輻射暴露的風險。

預計到 2025 年,檢測機器人領域將佔 27.8% 的市場佔有率。這些機器人配備了人工智慧驅動的導航和基於感測器的異常檢測功能,能夠對核子反應爐、管道和倉儲設施進行自主檢測,從而確保持續監測,同時減少人工運作、停機時間和輻射暴露。

預計到2025年,北美核能機器人市佔率將達到38.9%。該地區的成長主要得益於其龐大的核能基礎設施、大規模的核設施退役活動以及強調安全和自動化的強力的監管政策。人工智慧驅動的檢測、維護和廢棄物管理機器人的日益普及,以及政府資助的研發舉措,正在推動市場擴張。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 更加重視事故預防和緊急應變準備

- 老舊核能設施退役數量不斷增加

- 核能產業勞動力短缺和技能缺口

- 政府撥款和公共部門投資用於核能安基礎建設

- 產業潛在風險與挑戰

- 高昂的資本成本和生命週期成本

- 核能設施缺乏標準化和互通性

- 市場機遇

- 將機器人即服務 (RaaS) 模式擴展到退役計劃

- 開發適用於多站點的模組化、可重構機器人

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

- 地緣政治和貿易趨勢

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 主要企業的競爭標竿分析

- 財務績效比較

- 收入

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線的廣度

- 科技

- 創新

- 區域比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導企業

- 受讓人

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年主要發展動態

- 併購

- 合作夥伴關係和合資企業

- 技術進步

- 擴張與投資策略

- 數位轉型計劃

- 新興/Start-Ups競賽的趨勢

第5章 按類型分類的市場估算與預測,2022-2035年

- 遙控機械手臂

- 履帶

- 無人機

- 水下機器人(ROV)

- 人形機器人

第6章 依機器人類型分類的市場估算與預測,2022-2035年

- 檢查機器人

- 消毒機器人

- 維護和維修機器人

- 廢棄物機器人

- 緊急應變機器人

7. 2022-2035年按貨運能力分類的市場估算與預測

- 低負載容量機器人

- 負載容量機器人

- 高負載容量機器人

第8章 依最終用途產業分類的市場估算與預測,2022-2035年

- 核廢棄物處置

- 核能設施退役

- 輻射去污

- 核能發電廠

- 勘測和探勘

- 其他

第9章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 主要企業

- Orano

- Mitsubishi Heavy Industries

- Hitachi-GE Nuclear Energy

- Westinghouse Electric Company

- 按地區分類的主要企業

- 北美洲

- Amentum Services

- Mirion Technologies

- GE Inspection Robotics

- 歐洲

- QinetiQ Group

- Framatome

- Babcock International Group

- 亞太地區

- KUKA AG

- ABB

- Cybernetix(TechnipFMC)

- 北美洲

- 小眾玩家/顛覆者

- Boston Dynamics

- James Fisher &Sons

- Veolia Environnement

- Nuvia Group

- Oceaneering International

- Honeybee Robotics

- Inuktun Services

The Global Nuclear Robots Market was valued at USD 2.1 billion in 2025 and is estimated to grow at a CAGR of 13.8% to reach USD 7.5 billion by 2035.

Market growth is driven by the rising number of aging nuclear facilities worldwide, particularly in Europe and North America, where reactors and fuel cycle plants are exceeding their operational lifespans. Decommissioning these facilities involves working in highly radioactive and hazardous environments, which makes remote handling, inspection, and waste management critical for worker safety and regulatory compliance. Government funding and public sector investment in nuclear safety and modernization programs are further propelling demand for advanced robotics. Nuclear robots are specifically engineered for inspection, maintenance, deconstruction, and radioactive waste management, offering enhanced accuracy, operational efficiency, and minimized human exposure. The integration of artificial intelligence and autonomous technologies allows these machines to operate independently in challenging radioactive environments, reducing the need for expert personnel while increasing performance and safety. Decommissioning and site remediation programs continue to drive steady demand for these advanced solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.1 Billion |

| Forecast Value | $7.5 Billion |

| CAGR | 13.8% |

The remote manipulators segment is projected to reach USD 2.6 billion by 2035. Remote manipulators are widely adopted in radiation-heavy zones due to their capability to assemble, maintain, and handle nuclear components safely. Innovations in haptic feedback and intuitive control interfaces have improved operator precision while keeping exposure risks low.

The inspection robots segment accounted for 27.8% share in 2025. These robots are evolving with AI-powered navigation and sensor-based anomaly detection, enabling autonomous inspection of reactors, pipelines, and storage facilities. They reduce manual labor, operational downtime, and radiation exposure for personnel while ensuring continuous monitoring.

North America Nuclear Robots Market held a 38.9% share in 2025. Growth in the region is driven by extensive nuclear infrastructure, large-scale decommissioning activities, and strong regulatory policies emphasizing safety and automation. Increasing adoption of AI-driven inspection, maintenance, and waste management robots, combined with government-funded R&D initiatives, is bolstering market expansion.

Leading players in the Global Nuclear Robots Market include Hitachi-GE Nuclear Energy, Ltd., KUKA AG, ABB Ltd., Honeybee Robotics, Ltd., Boston Dynamics, Inc., Inuktun Services Ltd., Babcock International Group plc, QinetiQ Group plc, Orano, Framatome, Westinghouse Electric Company LLC, Nuvia Group, Amentum Services, Inc., GE Inspection Robotics, Mitsubishi Heavy Industries, Ltd., Veolia Environnement S.A., Oceaneering International, Inc., Cybernetix (TechnipFMC), James Fisher & Sons plc, and Mirion Technologies, Inc. Companies in the Global Nuclear Robots Market are strengthening their positions through continuous R&D investments to develop autonomous, AI-enabled systems capable of operating in extreme radiation environments. They are forming strategic partnerships with nuclear operators and government agencies to expand adoption. Geographic expansion into regions with aging nuclear infrastructure and decommissioning requirements is another key strategy.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Robot type trends

- 2.2.3 Payload capacity trends

- 2.2.4 End-use industry trends

- 2.2.5 Regional trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased focus on accident prevention and emergency response preparedness

- 3.2.1.2 Increasing decommissioning of aging nuclear facilities

- 3.2.1.3 Labor shortages and skill gaps in nuclear operations

- 3.2.1.4 Government funding and public sector investment in nuclear safety infrastructure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital and lifecycle costs

- 3.2.2.2 Limited standardization and interoperability across nuclear sites

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of robotics-as-a-service models for decommissioning projects

- 3.2.3.2 Development of modular, reconfigurable robots for multi-site applicability

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Patent and IP analysis

- 3.11 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn & Units)

- 5.1 Key trends

- 5.2 Remote manipulators

- 5.3 Crawlers

- 5.4 Aerial drones

- 5.5 Underwater robots (ROVs)

- 5.6 Humanoid robots

Chapter 6 Market Estimates and Forecast, By Robot Type, 2022 - 2035 ($ Mn & Units)

- 6.1 Key trends

- 6.2 Inspection robots

- 6.3 Decontamination robots

- 6.4 Maintenance & repair robots

- 6.5 Waste handling robots

- 6.6 Emergency response robots

Chapter 7 Market Estimates and Forecast, By Payload Capacity, 2022 - 2035 ($ Mn & Units)

- 7.1 Key trends

- 7.2 Low payload robots

- 7.3 Medium payload robots

- 7.4 High payload robots

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2022 - 2035 ($ Mn & Units)

- 8.1 Key trends

- 8.2 Nuclear waste handling

- 8.3 Nuclear decommissioning

- 8.4 Radiation cleanup

- 8.5 Nuclear power plants

- 8.6 Research & exploration

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Orano

- 10.1.2 Mitsubishi Heavy Industries

- 10.1.3 Hitachi-GE Nuclear Energy

- 10.1.4 Westinghouse Electric Company

- 10.2 Regional Key Players

- 10.2.1 North America

- 10.2.1.1 Amentum Services

- 10.2.1.2 Mirion Technologies

- 10.2.1.3 GE Inspection Robotics

- 10.2.2 Europe

- 10.2.2.1 QinetiQ Group

- 10.2.2.2 Framatome

- 10.2.2.3 Babcock International Group

- 10.2.3 APAC

- 10.2.3.1 KUKA AG

- 10.2.3.2 ABB

- 10.2.3.3 Cybernetix (TechnipFMC)

- 10.2.1 North America

- 10.3 Niche Players / Disruptors

- 10.3.1 Boston Dynamics

- 10.3.2 James Fisher & Sons

- 10.3.3 Veolia Environnement

- 10.3.4 Nuvia Group

- 10.3.5 Oceaneering International

- 10.3.6 Honeybee Robotics

- 10.3.7 Inuktun Services

零售機器人市場:2026-2032年全球市場預測(按產品類型、組件、整合類型、應用、最終用戶和部署模式分類)

零售機器人市場:2026-2032年全球市場預測(按產品類型、組件、整合類型、應用、最終用戶和部署模式分類) 2026年全球機器人廚房市場報告商用機器人市場:按類型、應用、酬載能力和最終用戶產業分類-2026-2032年全球市場預測

2026年全球機器人廚房市場報告商用機器人市場:按類型、應用、酬載能力和最終用戶產業分類-2026-2032年全球市場預測 機器人廚房市場預測至2034年:全球分析(按組件、機器人類型、功能、部署模式、應用、最終用戶和地區分類)2026年全球零售機器人市場報告

機器人廚房市場預測至2034年:全球分析(按組件、機器人類型、功能、部署模式、應用、最終用戶和地區分類)2026年全球零售機器人市場報告 全球商用機器人市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球商用機器人市場報告智慧電話行銷機器人市場:依組織規模、部署類型、交付管道、應用和產業垂直領域分類,全球預測,2026-2032年

全球商用機器人市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球商用機器人市場報告智慧電話行銷機器人市場:依組織規模、部署類型、交付管道、應用和產業垂直領域分類,全球預測,2026-2032年 商用機器人市場規模、佔有率和成長分析(按類型、最終用戶、應用、技術和地區分類)-2026-2033年產業預測

商用機器人市場規模、佔有率和成長分析(按類型、最終用戶、應用、技術和地區分類)-2026-2033年產業預測 全球商業建築機器人市場

全球商業建築機器人市場