|

市場調查報告書

商品編碼

1913480

醫用吸痰設備市場機會、成長要素、產業趨勢分析及2026年至2035年預測Medical Suction Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

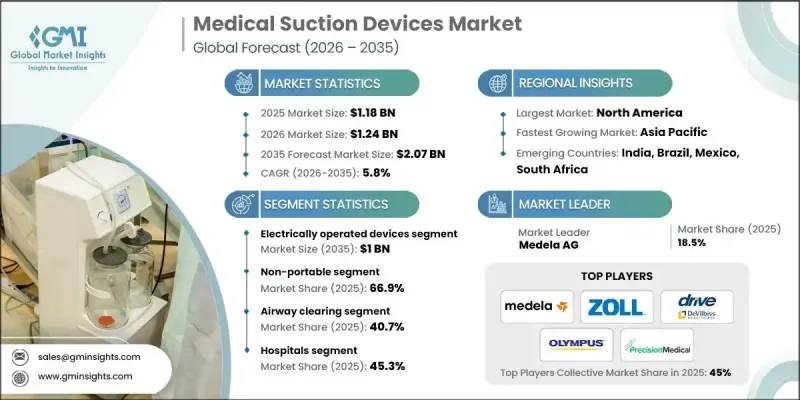

全球醫用吸痰設備市場預計到 2025 年將達到 11.8 億美元,預計到 2035 年將達到 20.7 億美元,年複合成長率為 5.8%。

這一上升趨勢得益於長期呼吸系統疾病負擔的加重、依賴吸痰技術的醫療程序的擴展以及居家醫療解決方案日益普及。隨著呼吸系統疾病的日益普遍,有效的呼吸道清除對於減少併發症和促進患者康復至關重要。醫用吸痰系統也被廣泛應用於各種臨床環境中,透過清除體液和分泌物,在醫療過程中保持視野清晰和環境清潔。全球外科手術和診斷程序的不斷增加進一步強化了對這些設備的需求。此外,微創醫療技術的興起也推動了對精準可控的體液管理的需求,進而促進了能夠確保準確性、安全性和穩定臨床效果的先進吸痰解決方案的應用。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 11.8億美元 |

| 預測金額 | 20.7億美元 |

| 複合年成長率 | 5.8% |

預計到2025年,電動醫用吸痰設備市場規模將達5.736億美元。這些設備因其性能可靠、吸力控制可調以及能夠支援連續運行而備受青睞。其設計兼具功能一致性、便攜性和自動化安全功能,因此在醫療保健領域中廣泛應用。

預計到2025年,非攜帶式吸痰系統市佔率將達到66.9%。這些固定式設備主要用於醫院和高級醫療機構,滿足其高容量、不間斷吸痰的需求。其堅固耐用的設計可為關鍵醫療程序和長期患者管理提供可靠且持續的性能。

預計到 2025 年,美國醫用吸痰設備市場規模將達到 4.433 億美元。慢性呼吸系統疾病發生率的上升持續推動急診、急性照護和長期照護機構對呼吸道管理解決方案的需求。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 產業影響因素

- 促進要素

- 慢性呼吸系統疾病呈上升趨勢

- 需要吸痰設備的手術數量增加

- 人們越來越偏好居家醫療

- 提高新興經濟體對攜帶式醫用吸痰設備的認知

- 產業潛在風險與挑戰

- 熟練專業人員短缺

- 吸痰裝置的報銷限額

- 市場機遇

- 持續的技術改進

- 擴大公共醫療基礎設施

- 促進要素

- 成長潛力分析

- 監管環境

- 技術進步

- 當前技術趨勢

- 新興技術

- 供應鏈分析

- 2024年定價分析

- 未來市場趨勢

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 合作夥伴關係和合資企業

- 新產品發布

- 擴張計劃

第5章 按類型分類的市場估算與預測,2022-2035年

- 電子設備

- 手動裝置

- 文丘里管

第6章 市場估算與預測:2022-2035年手機性別分佈

- 不便攜帶式

- 可攜式的

第7章 按應用領域分類的市場估算與預測,2022-2035年

- 氣道管理

- 外科

- 胃

- 其他

第8章 依最終用途分類的市場估算與預測,2022-2035年

- 醫院

- 診所

- 其他

第9章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第10章:公司簡介

- Allied Healthcare Products, Inc.

- Precision Medical, Inc.

- Drive Medical

- Integra Biosciences AG

- Medicop, Inc.

- ATMOS MedizinTechnik GmbH &Co. KG

- ZOLL Medical Corporation

- Welch Vacuum

- Laerdal Medical

- Amsino International, Inc.

- Olympus Corporation

- Medtronic

The Global Medical Suction Devices Market was valued at USD 1.18 billion in 2025 and is estimated to grow at a CAGR of 5.8% to reach USD 2.07 billion by 2035.

The upward trend is supported by the rising burden of long-term respiratory conditions, the expanding volume of medical interventions that rely on suction technology, and the growing acceptance of home-based healthcare solutions. As respiratory disorders become more common, effective airway clearance has become essential to reduce complications and support patient recovery. Medical suction systems are also widely relied upon to maintain visibility and cleanliness during medical procedures by removing fluids and secretions across diverse clinical settings. The increasing global volume of surgical and diagnostic procedures continues to reinforce demand for these devices. In addition, the shift toward less invasive medical techniques has increased the need for precise and controlled fluid management, driving the adoption of advanced suction solutions that support accuracy, safety, and consistent clinical outcomes.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.18 Billion |

| Forecast Value | $2.07 Billion |

| CAGR | 5.8% |

The electrically powered medical suction devices segment generated USD 573.6 million in 2025. These devices are favored for their dependable performance, adjustable suction control, and ability to support continuous operation. Their design enables consistent functionality, portability options, and automated safety features, making them widely used across healthcare environments.

The non-portable suction systems segment accounted for 66.9% share in 2025. These stationary units are primarily used in hospitals and advanced care facilities where high-capacity and uninterrupted suction is required. Their robust design supports critical medical procedures and long-term patient management by delivering reliable and sustained performance.

U.S. Medical Suction Devices Market recorded USD 443.3 million in 2025. The rising incidence of chronic respiratory conditions continues to drive demand for airway management solutions across emergency, acute, and extended care settings.

Key companies operating in the Global Medical Suction Devices Market include Medtronic, Laerdal Medical, Allied Healthcare Products, Inc., Olympus Corporation, Drive DeVilbiss Healthcare, ATMOS MedizinTechnik GmbH & Co. KG, ZOLL Medical Corporation, Precision Medical, Inc., Amsino International, Inc., Integra Biosciences AG, Medicop, Inc., and Welch Vacuum. Companies in the Global Medical Suction Devices Market are strengthening their market position through innovation, product diversification, and strategic expansion. Many manufacturers are investing in advanced device designs that improve reliability, ease of use, and patient safety. Emphasis is being placed on developing compact, energy-efficient, and user-friendly systems suited for both clinical and home-care environments. Firms are also expanding their geographic footprint through partnerships and distribution agreements to improve market access.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Portability trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of chronic respiratory disorders

- 3.2.1.2 Rising number of procedures that require suction devices.

- 3.2.1.3 Increasing preference for home healthcare

- 3.2.1.4 Increase in awareness regarding portable medical suction devices in emerging economies.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Dearth of skilled professionals

- 3.2.2.2 Limited reimbursement for suction devices

- 3.2.3 Market opportunities

- 3.2.3.1 Ongoing technology improvements

- 3.2.3.2 Expansion of public healthcare infrastructure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Pricing analysis, 2024

- 3.8 Future market trends

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Electrically operated devices

- 5.3 Manually operated devices

- 5.4 Venturi

Chapter 6 Market Estimates and Forecast, By Portability, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Non portable

- 6.3 Portable

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Airway clearing

- 7.3 Surgical

- 7.4 Gastric

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 clinics

- 8.4 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Allied Healthcare Products, Inc.

- 10.2 Precision Medical, Inc.

- 10.3 Drive Medical

- 10.4 Integra Biosciences AG

- 10.5 Medicop, Inc.

- 10.6 ATMOS MedizinTechnik GmbH & Co. KG

- 10.7 ZOLL Medical Corporation

- 10.8 Welch Vacuum

- 10.9 Laerdal Medical

- 10.10 Amsino International, Inc.

- 10.11 Olympus Corporation

- 10.12 Medtronic

醫用吸痰設備市場:依產品、真空系統、應用、最終用戶和銷售管道分類-2026-2032年全球市場預測外科吸引裝置市場:2026-2032年全球市場預測(按產品類型、最終用戶、分銷管道、應用和技術分類)足部吸痰裝置市場:按操作方式、便攜性、患者類型、銷售管道、應用和最終用戶分類——2026-2032年全球市場預測

醫用吸痰設備市場:依產品、真空系統、應用、最終用戶和銷售管道分類-2026-2032年全球市場預測外科吸引裝置市場:2026-2032年全球市場預測(按產品類型、最終用戶、分銷管道、應用和技術分類)足部吸痰裝置市場:按操作方式、便攜性、患者類型、銷售管道、應用和最終用戶分類——2026-2032年全球市場預測 2026年全球吸力及真空設備市場報告2026年全球醫用吸痰設備市場報告

2026年全球吸力及真空設備市場報告2026年全球醫用吸痰設備市場報告 外科吸引設備市場分析及預測(至2035年):類型、產品、技術、應用、最終用戶、材料類型、設備、製程、功能、安裝類型

外科吸引設備市場分析及預測(至2035年):類型、產品、技術、應用、最終用戶、材料類型、設備、製程、功能、安裝類型 醫用抽吸裝置市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年預測

醫用抽吸裝置市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年預測 外科吸引設備市場-全球產業規模、佔有率、趨勢、機會及預測:類型、可用性、應用、最終用戶、地區及競爭格局,2021-2031年

外科吸引設備市場-全球產業規模、佔有率、趨勢、機會及預測:類型、可用性、應用、最終用戶、地區及競爭格局,2021-2031年 醫用吸痰設備市場規模、佔有率及成長分析(按產品類型、應用、最終用戶、技術及地區分類)-2026-2033年產業預測吸塵器設備市場按類型、技術、應用、最終用戶和分銷管道分類,全球預測(2026-2032年)

醫用吸痰設備市場規模、佔有率及成長分析(按產品類型、應用、最終用戶、技術及地區分類)-2026-2033年產業預測吸塵器設備市場按類型、技術、應用、最終用戶和分銷管道分類,全球預測(2026-2032年)