|

市場調查報告書

商品編碼

1913450

自主農業機械市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)Autonomous Farm Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

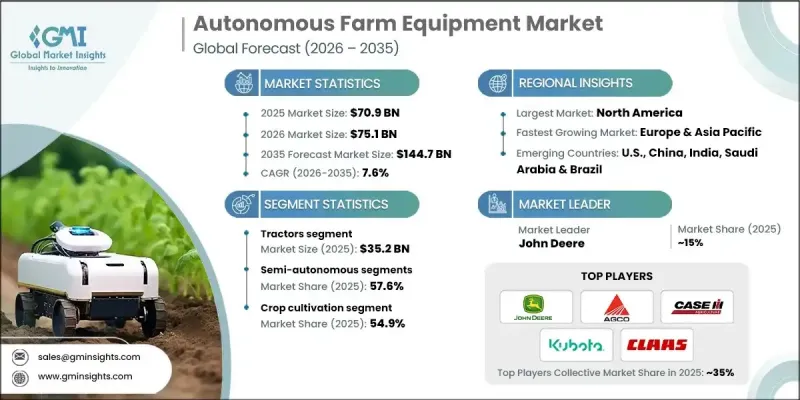

全球自主農業機械市場預計到 2025 年將達到 709 億美元,到 2035 年將達到 1,447 億美元,年複合成長率為 7.6%。

該行業的成長主要得益於精密農業技術的日益普及。這些技術使農民能夠最佳化投入使用、最大限度地減少資源浪費並提高作物產量。曳引機、收割機和無人機等自主機械使農民能夠在最佳時機施用投入物,從而提高盈利並減少對環境的影響。人工智慧、物聯網、機器人和機器視覺的融合正在革新農業,使作物監測、土壤評估和自動化收割等高級任務成為可能,並最大限度地減少人為干預。包括5G和雲端平台在內的先進通訊網路實現了即時監控和遠端控制,進一步提高了效率並促進了技術的普及應用。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 709億美元 |

| 預測金額 | 1447億美元 |

| 複合年成長率 | 7.6% |

預計到2025年,曳引機市場規模將達到352億美元,2026年至2035年的複合年成長率將達到7.4%。曳引機在關鍵農業作業中至關重要,隨著人工智慧、GPS導航和物聯網連接的整合,它們正朝著高效的半自動或全自動機械發展。勞動力短缺和營運成本上升正在推動市場需求,這些曳引機在提高作業精度和生產效率的同時,減少了對人工的依賴。

半自動設備市佔率佔比達57.6%,預計2026年至2035年將以7.1%的複合年成長率成長。這類設備兼顧自動化和人工監管,使農民能夠在保持作業柔軟性的同時,獲得諸如自動轉向和精準控制等功能。這種混合模式解決了投資成本和技術複雜性的擔憂,既能促進自動化系統的順利應用,又能提高重複性工作的效率。

美國自主農業設備市場預計到2025年將達到185億美元,2026年至2035年的複合年成長率將達到8.5%。規模較大的農場和技術先進的農業部門正在推動自主解決方案的普及。成熟製造商和新興企業對人工智慧、機器人和物聯網的大量投資正在加速這一進程。政府對智慧農業技術和永續實踐的激勵措施也進一步推動了市場擴張。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 產業影響因素

- 促進要素

- 擴大精密農業的引進

- 技術進步

- 政府政策與補貼

- 勞動短缺和成本上升

- 產業潛在風險與挑戰

- 高昂的初始投資和成本壁壘

- 連接性和基礎設施限制

- 促進要素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 監管環境

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 2022-2035年按產品分類的市場估算與預測

- 聯結機

- 收割機

- 播種機

- 噴霧器

- 無人駕駛飛行器(UAV)

- 其他(耕耘機、灌溉設備)

第6章 按技術分類的市場估計與預測,2022-2035年

- 導引與導航系統

- 感測器技術

- 人工智慧(AI)和機器學習

- 機器人與自動化

- 連接和通訊系統

第7章 2022-2035年各細分市場的估計與預測

- 完全自主

- 半自主

第8章 按產量分類的市場估計與預測,2022-2035年

- 不到30馬力

- 31-100馬力

- 超過100馬力

第9章 按應用領域分類的市場估算與預測,2022-2035年

- 作物種植

- 園藝和幼苗

- 酪農和畜牧業管理

- 林業和木材管理

第10章 按分銷管道分類的市場估算與預測,2022-2035年

- 直銷

- 間接銷售

第11章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 印尼

- 馬來西亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第12章:公司簡介

- AGCO Corporation

- Agrobot

- Autonomous Solutions Inc.

- Case IH

- Claas

- Dot Technology Corp

- DroneDeploy

- Fendt

- Harvest Automation

- John Deere

- Kinze Manufacturing

- Kubota Corporation

- New Holland Agriculture

- Precision Planting

- Raven Industries

The Global Autonomous Farm Equipment Market was valued at USD 70.9 billion in 2025 and is estimated to grow at a CAGR of 7.6% to reach USD 144.7 billion by 2035.

Growth in this sector is fueled by the increasing adoption of precision farming techniques. These methods allow farmers to optimize input use, minimize resource wastage, and maximize crop output. Autonomous machines such as tractors, harvesters, and drones enable farmers to apply inputs at the most effective times, improving profitability while reducing environmental impact. The convergence of AI, IoT, robotics, and machine vision is revolutionizing agriculture, enabling sophisticated operations like crop monitoring, soil assessment, and automated harvesting with minimal human intervention. Advanced communication networks, including 5G and cloud platforms, allow real-time monitoring and remote operation, further enhancing efficiency and adoption.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $70.9 Billion |

| Forecast Value | $144.7 Billion |

| CAGR | 7.6% |

The tractors segment accounted for USD 35.2 billion in 2025 and is expected to grow at a CAGR of 7.4% from 2026 to 2035. They remain critical for essential farm operations, and the integration of AI, GPS navigation, and IoT connectivity has transformed them into highly efficient, semi- or fully-autonomous machines. Labor shortages and rising operational costs drive demand, as these tractors reduce reliance on manual work while boosting precision and productivity.

The semi-autonomous equipment segment held a 57.6% share and is projected to grow at a CAGR of 7.1% from 2026 to 2035. This equipment offers a balance between automation and human oversight, providing features like auto-steering and precision controls while allowing farmers to retain operational flexibility. This hybrid approach addresses concerns over investment costs and technical complexity, enabling smoother adoption of automated systems and improving efficiency for repetitive tasks.

U.S. Autonomous Farm Equipment Market was valued at USD 18.5 billion in 2025 and is forecasted to grow at a CAGR of 8.5% from 2026 to 2035. Large-scale farms and a technologically advanced agricultural sector drive the adoption of autonomous solutions. Substantial investments in AI, robotics, and IoT by both established manufacturers and startups accelerate deployment. Government incentives for smart farming technologies and sustainable practices further stimulate market expansion.

Key players in the Global Autonomous Farm Equipment Market include Case IH, John Deere, Kinze Manufacturing, Kubota Corporation, AGCO Corporation, Claas, Dot Technology Corp, DroneDeploy, Precision Planting, New Holland Agriculture, Fendt, Harvest Automation, Autonomous Solutions Inc., and Agrobot. Companies in the Autonomous Farm Equipment Market are focusing on multiple strategies to strengthen their foothold. They are investing heavily in research and development to enhance the capabilities of autonomous machines, including AI-driven navigation and advanced sensor integration. Strategic partnerships and collaborations with tech startups and agri-tech firms help expand product portfolios and enter new markets. Firms are also emphasizing after-sales services, training, and support programs to boost customer adoption.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Technology

- 2.2.4 Operation

- 2.2.5 Power output

- 2.2.6 Application

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of precision agriculture

- 3.2.1.2 Technological advancements

- 3.2.1.3 Government initiatives and subsidies

- 3.2.1.4 Labor shortages and rising costs

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment and cost barriers

- 3.2.2.2 Connectivity and infrastructure limitations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Tractor

- 5.3 Harvesters

- 5.4 Planters

- 5.5 Sprayers

- 5.6 UAVs

- 5.7 Others (cultivators, irrigation equipment)

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Guidance & navigation systems

- 6.3 Sensor technologies

- 6.4 Artificial intelligence & machine learning

- 6.5 Robotics & automation

- 6.6 Connectivity and communication systems

Chapter 7 Market Estimates & Forecast, By Operation, 2022 - 2035, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Fully autonomous

- 7.3 Semi-autonomous

Chapter 8 Market Estimates & Forecast, By Power Output, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Below 30 HP

- 8.3 31-100 HP

- 8.4 Above 100 HP

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Crop cultivation

- 9.3 Horticulture & nursery

- 9.4 Dairy & livestock management

- 9.5 Forestry & timber management

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Indonesia

- 11.4.7 Malaysia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 AGCO Corporation

- 12.2 Agrobot

- 12.3 Autonomous Solutions Inc.

- 12.4 Case IH

- 12.5 Claas

- 12.6 Dot Technology Corp

- 12.7 DroneDeploy

- 12.8 Fendt

- 12.9 Harvest Automation

- 12.10 John Deere

- 12.11 Kinze Manufacturing

- 12.12 Kubota Corporation

- 12.13 New Holland Agriculture

- 12.14 Precision Planting

- 12.15 Raven Industries

自主農業機械市場:按類型、組件、技術、推進系統、農場規模和運作方式分類-2026-2032年全球市場預測

自主農業機械市場:按類型、組件、技術、推進系統、農場規模和運作方式分類-2026-2032年全球市場預測 全球自主農業機械市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球自主農業機械市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球自主農業機械市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球自主農業機械市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球自主農業機械市場報告

2026年全球自主農業機械市場報告 全球自主農業機械市場預測至2032年:按類型、組件、自主程度、動力來源、技術、應用和地區分類的分析

全球自主農業機械市場預測至2032年:按類型、組件、自主程度、動力來源、技術、應用和地區分類的分析 全球自主農業機械市場

全球自主農業機械市場 自主農業設備市場,按類型、按應用、按電源、按技術、按最終用戶、按國家和地區 - 2025 年至 2032 年的全球行業分析、市場規模、市場佔有率和預測

自主農業設備市場,按類型、按應用、按電源、按技術、按最終用戶、按國家和地區 - 2025 年至 2032 年的全球行業分析、市場規模、市場佔有率和預測 自主農業設備市場規模、佔有率、成長分析,按產品、按技術、按自動化類型、按應用、按地區 - 行業預測,2024-2031 年

自主農業設備市場規模、佔有率、成長分析,按產品、按技術、按自動化類型、按應用、按地區 - 行業預測,2024-2031 年 自主農業機械市場:按產品(拖拉機、收割機、灌溉機、畜牧機械)、按技術(物聯網、GPS)、按自動化類型、按應用(農業、畜牧業)、按地區 - 2031 年世界預測年

自主農業機械市場:按產品(拖拉機、收割機、灌溉機、畜牧機械)、按技術(物聯網、GPS)、按自動化類型、按應用(農業、畜牧業)、按地區 - 2031 年世界預測年 自主農業機械市場:按產品、按自動化、按應用、按地區、細分市場預測,2024-2030 年

自主農業機械市場:按產品、按自動化、按應用、按地區、細分市場預測,2024-2030 年