|

市場調查報告書

商品編碼

1913430

智慧卡市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)Smart Card Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球智慧卡市場預計到 2025 年將達到 652 億美元,到 2035 年將達到 1,228 億美元,年複合成長率為 6.3%。

智慧卡徹底改變了支付方式,取代了傳統的磁條卡和接觸式卡,實現了非接觸式交易。除了付款之外,智慧卡還透過儲存預先註冊的使用者資料進行身份驗證,從而革新了安全應用,幫助機構檢驗對建築物、電腦系統和其他安全區域的存取權限。智慧卡的應用已擴展到醫療保健、政府和交通運輸等領域,提供諸如醫療記錄追蹤、電子旅行登記和安全識別等功能。在美國,預計到2023年,非接觸式交易量將超過170億筆,隨著消費者越來越傾向於使用數位支付方式而非現金,這一數字也將繼續成長。在那些安全存取和無縫數位互動至關重要的行業,智慧卡技術的應用至關重要。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 652億美元 |

| 預測金額 | 1228億美元 |

| 複合年成長率 | 6.3% |

預計到2025年,智慧卡市佔率將達到66.5%。智慧卡已成為數位存取的基礎,並在銀行、金融、政府和安全等領域中廣泛應用。主要分銷合作夥伴透過提供多功能智慧卡,正推動著市場成長。

受全球智慧型手機用戶數量不斷成長的推動,預計到2025年,電信業的市場規模將達到282億美元。到2025年底,全球將有超過60億人上網,顯示該產業的影響力巨大。

預計2025年,美國智慧卡市場規模將達到121億美元。美國在智慧卡應用方面處於全球領先地位,聯邦政府機構正利用這項技術進行身份驗證、安全身份核查和非接觸式應用。政府專案採用智慧卡體現了美國對安全和數位轉型的重視。

目錄

第1章調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 對非接觸式支付解決方案的需求不斷成長

- 政府數位化舉措與電子管治項目

- 在新興市場拓展銀行服務

- 在交通運輸和旅遊領域不斷拓展應用

- 產業潛在風險與挑戰

- 來自行動支付和數位錢包解決方案的競爭日益加劇

- 卡片使用壽命短,更換成本高

- 市場機遇

- 開發永續且環保的卡片材料

- 升級忠誠度計畫和多用途卡

- 電信和SIM卡應用領域的成長

- 智慧城市與城市基礎建設發展

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 美國資訊處理標準(FIPS)

- 加拿大個人資訊保護與電子文件法

- 歐洲

- 一般資料保護規則(GDPR)

- 德國電子身分證(eID)法規

- 法國Carte Vital健康保險智慧卡標準

- 英國生物識別居住許可(BRP)

- 亞太地區

- 中國居民身分證(電子身分證)法

- 關於日本個人號碼卡系統的相關規定

- 印度的 Aadhaar 驗證和 eKYC 法規

- 拉丁美洲

- 巴西PIX即時支付系統的安全要求

- 墨西哥CURP電子識別標準

- 中東和非洲

- 阿拉伯聯合大公國(阿拉伯聯合大公國)ID卡系統條例

- 沙烏地阿拉伯國民身分證(Abshah)智慧卡框架

- 南非智慧ID卡法案(1997 年)

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 成本細分分析

- 永續性和環境影響

- 環境影響評估

- 社會影響力和社區服務

- 公司管治與企業社會責任

- 永續金融與投資趨勢

- 產業採用模式

- 銀行業及金融服務業的採用

- 政府和公共部門採用

- 交通運輸和出行領域的趨勢

- 醫療領域採用的促進因素

- 通訊業使用模式

- 未來前景與機遇

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 企業擴張計畫和資金籌措

第5章 依產品類型分類的市場估算與預測,2022-2035年

- 智慧卡

- 介面

- 詢問

- 非接觸式

- 相容NFC

- 基於RFID的

- 雙介面

- 尖端

- 記憶卡

- 微處理器卡

- 介面

- 智慧卡讀卡器

- 介面

- 聯繫類型

- 非接觸式

- 雙介面

- 成分

- 硬體

- 軟體

- 服務

- 介面

第6章 依功能分類的市場估計與預測,2022-2035年

- 交易

- 溝通

- 安全和存取控制

- 其他

第7章 按應用領域分類的市場估算與預測,2022-2035年

- BFSI

- 溝通

- 政府和醫療領域

- 零售與電子商務

- 運輸

- 媒體與娛樂

- 教育和學術機構

- 其他

第8章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 比荷盧經濟聯盟

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ANZ

- 新加坡

- 馬來西亞

- 印尼

- 越南

- 泰國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- 世界公司

- Thales

- IDEMIA

- Giesecke+Devrient

- NXP Semiconductors

- Infineon

- STMicroelectronics

- CPI Card

- HID Global

- Watchdata

- Eastcompeace

- Samsung Electronics

- Valid

- Ingenico

- Hengbao

- 本地公司

- Linxens

- Paragon ID

- Perfect Plastic Printing

- Identiv

- VeriFone

- SecureID

- CardLogix

- Bartronics

- 新興企業

- Kona I

- BrilliantTS

- Goldpac

- Wuhan Tianyu Information Industry

- Feitian

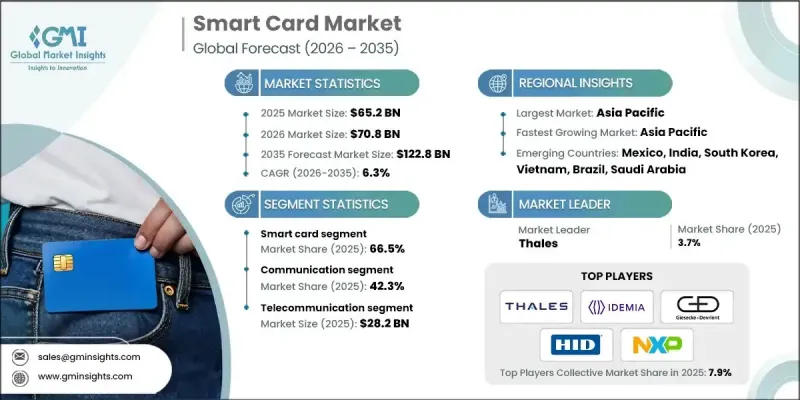

The Global Smart Card Market was valued at USD 65.2 billion in 2025 and is estimated to grow at a CAGR of 6.3% to reach USD 122.8 billion by 2035.

Smart cards have revolutionized payment methods, enabling users to conduct transactions through contactless interfaces instead of traditional magnetic stripe or contract cards. Beyond payments, smart cards have transformed security applications by storing preloaded user data for authentication purposes, helping organizations validate access to buildings, computer systems, and other secured areas. Their use has expanded across healthcare, government, and transportation sectors, providing functionalities such as medical record tracking, electronic passenger lists, and secure identification. In the U.S., contactless transactions have exceeded 17 billion by 2023 and continue to grow as consumers increasingly prefer digital payment methods over cash. The adoption of smart card technology has become critical in sectors where secure access and seamless digital interaction are essential.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $65.2 Billion |

| Forecast Value | $122.8 Billion |

| CAGR | 6.3% |

The smart cards segment held a 66.5% share in 2025. They have become a cornerstone of digital access, with widespread adoption in banking, finance, government, and security applications. Key distribution partners have accelerated growth by offering smart cards for multiple purposes.

The telecommunication segment was valued at USD 28.2 billion in 2025, supported by the rise in smartphone users globally. By late 2025, over 6 billion people were using the internet, indicating the sector's strong influence.

U.S. Smart Card Market reached USD 12.1 billion in 2025. The country leads in smart card adoption, with federal agencies utilizing the technology for credentialing, secure identification, and contactless applications. Smart card implementation in government programs demonstrates the nation's commitment to security and digital transformation.

Prominent companies operating in the Global Smart Card Market include Thales, IDEMIA, Giesecke & Devrient, HID Global, NXP Semiconductors, CPI Card, Infineon Technologies, Eastcompeace, Hengbao, and Watchdata Technologies. To strengthen their presence, companies in the Smart Card Market are focusing on product innovation by developing advanced, multi-functional cards with enhanced security features and contactless capabilities. Strategic collaborations with payment networks, telecommunications providers, and government agencies are being leveraged to expand reach and increase adoption. Firms are also investing in R&D to integrate emerging technologies such as AI and biometrics into smart cards, improving functionality and user experience.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Offering

- 2.2.3 Functionality

- 2.2.4 Application

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for contactless payment solutions

- 3.2.1.2 Government digitalization initiatives and e-governance programs

- 3.2.1.3 Expansion of banking services in emerging markets

- 3.2.1.4 Growing transportation and mobility applications

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Growing competition from mobile payment and digital wallet solutions

- 3.2.2.2 Short card lifecycle and replacement costs

- 3.2.3 Market opportunities

- 3.2.3.1 Development of sustainable and eco-friendly card materials

- 3.2.3.2 Enhanced loyalty programs and multi-application cards

- 3.2.3.3 Growth in telecom and sim card applications

- 3.2.3.4 Smart cities and urban infrastructure development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. Federal Information Processing Standards (FIPS)

- 3.4.1.2 Canadian Personal Information Protection and Electronic Documents Act

- 3.4.2 Europe

- 3.4.2.1 EU General Data Protection Regulation (GDPR)

- 3.4.2.2 German electronic identity card (eID) regulations

- 3.4.2.3 French carte vitale health insurance smart card standards

- 3.4.2.4 UK biometric residence permit (BRP)

- 3.4.3 Asia Pacific

- 3.4.3.1 China's Resident Identity Card (eID card) law

- 3.4.3.2 Japan My Number card system regulations

- 3.4.3.3 Indian Aadhaar authentication and eKYC regulations

- 3.4.4 Latin America

- 3.4.4.1 Brazil PIX instant payment system security requirements

- 3.4.4.2 Mexican CURP electronic identity card standards

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE Emirates ID card system regulations

- 3.4.5.2 Saudi Arabian national ID (Absher) smart card framework

- 3.4.5.3 South African smart ID card act 1997

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Sustainability and environmental impact

- 3.10.1 Environmental impact assessment

- 3.10.2 Social impact & community benefits

- 3.10.3 Governance & corporate responsibility

- 3.10.4 Sustainable finance & investment trends

- 3.11 Industry adoption patterns

- 3.11.1 Banking and financial services sector adoption

- 3.11.2 Government and public sector implementation

- 3.11.3 Transportation and mobility sector trends

- 3.11.4 Healthcare sector adoption drivers

- 3.11.5 Telecommunications industry usage patterns

- 3.12 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Offering, 2022 - 2035 ($Bn, units)

- 5.1 Key trends

- 5.2 Smart Card

- 5.2.1 Interface

- 5.2.1.1 Contact

- 5.2.1.2 Contactless

- 5.2.1.2.1 NFC-enabled

- 5.2.1.2.2 RFID-based

- 5.2.1.3 Dual Interface

- 5.2.2 Chip

- 5.2.3 Memory cards

- 5.2.4 Microprocessor cards

- 5.2.1 Interface

- 5.3 Smart Card Readers

- 5.3.1 Interface

- 5.3.1.1 Contact-based

- 5.3.1.2 Contactless

- 5.3.1.3 Dual Interface

- 5.3.2 Component

- 5.3.2.1 Hardware

- 5.3.2.2 Software

- 5.3.2.3 Services

- 5.3.1 Interface

Chapter 6 Market Estimates & Forecast, By Functionality, 2022 - 2035 ($Bn, units)

- 6.1 Key trends

- 6.2 Transaction

- 6.3 Communication

- 6.4 Security & Access Control

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, units)

- 7.1 Key trends

- 7.2 BFSI

- 7.3 Telecommunication

- 7.4 Government & healthcare

- 7.5 Retail & ecommerce

- 7.6 Transportation

- 7.7 Media & entertainment

- 7.8 Education & academic institutions

- 7.9 Others

Chapter 8 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 US

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.3.8 Benelux

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 ANZ

- 8.4.6 Singapore

- 8.4.7 Malaysia

- 8.4.8 Indonesia

- 8.4.9 Vietnam

- 8.4.10 Thailand

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Colombia

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global companies

- 9.1.1 Thales

- 9.1.2 IDEMIA

- 9.1.3 Giesecke+Devrient

- 9.1.4 NXP Semiconductors

- 9.1.5 Infineon

- 9.1.6 STMicroelectronics

- 9.1.7 CPI Card

- 9.1.8 HID Global

- 9.1.9 Watchdata

- 9.1.10 Eastcompeace

- 9.1.11 Samsung Electronics

- 9.1.12 Valid

- 9.1.13 Ingenico

- 9.1.14 Hengbao

- 9.2 Regional companies

- 9.2.1 Linxens

- 9.2.2 Paragon ID

- 9.2.3 Perfect Plastic Printing

- 9.2.4 Identiv

- 9.2.5 VeriFone

- 9.2.6 SecureID

- 9.2.7 CardLogix

- 9.2.8 Bartronics

- 9.3 Emerging companies

- 9.3.1 Kona I

- 9.3.2 BrilliantTS

- 9.3.3 Goldpac

- 9.3.4 Wuhan Tianyu Information Industry

- 9.3.5 Feitian

政府智慧卡市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、形狀、材質、最終用戶和功能分類晶片級安全增強市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、製程、最終用戶、解決方案分類智慧卡市場分析及預測(至2035年):類型、產品、服務、技術、組件、應用、材質類型、部署類型與最終用戶

政府智慧卡市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、形狀、材質、最終用戶和功能分類晶片級安全增強市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、製程、最終用戶、解決方案分類智慧卡市場分析及預測(至2035年):類型、產品、服務、技術、組件、應用、材質類型、部署類型與最終用戶 2026年全球雙介面積體電路卡市場報告

2026年全球雙介面積體電路卡市場報告 智慧卡MCU市場-全球產業規模、佔有率、趨勢、機會及預測(依產品、功能、終端用戶產業、地區及競爭格局分類),2021-2031年

智慧卡MCU市場-全球產業規模、佔有率、趨勢、機會及預測(依產品、功能、終端用戶產業、地區及競爭格局分類),2021-2031年 人工智慧智慧型裝置市場:2026-2032年全球預測(按產品類型、最終用戶、部署類型、公司規模和通路分類)數位電視智慧型裝置市場按面板技術、螢幕大小、解析度、作業系統和銷售管道-全球預測(2026-2032 年)

人工智慧智慧型裝置市場:2026-2032年全球預測(按產品類型、最終用戶、部署類型、公司規模和通路分類)數位電視智慧型裝置市場按面板技術、螢幕大小、解析度、作業系統和銷售管道-全球預測(2026-2032 年) 智慧卡市場規模、佔有率和成長分析(按類型、組件、功能、應用和地區分類)—2026-2033年產業預測

智慧卡市場規模、佔有率和成長分析(按類型、組件、功能、應用和地區分類)—2026-2033年產業預測 政府證件和國民身分證市場的量子技術準備交通智慧卡市場-全球產業規模、佔有率、趨勢、機會和預測,按卡片類型、最終用戶、地區和競爭格局分類,2020-2030年預測

政府證件和國民身分證市場的量子技術準備交通智慧卡市場-全球產業規模、佔有率、趨勢、機會和預測,按卡片類型、最終用戶、地區和競爭格局分類,2020-2030年預測