|

市場調查報告書

商品編碼

1913367

感染控制用品市場:市場機會、成長促進因素、產業趨勢分析及預測(2026-2035 年)Infection Control Supplies Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

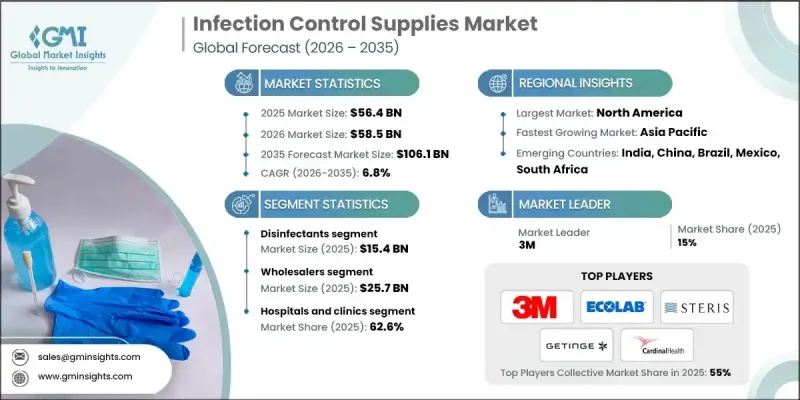

全球感染控制用品市場預計到 2025 年將達到 564 億美元,到 2035 年將達到 1,061 億美元,年複合成長率為 6.8%。

市場成長得益於醫療環境中感染疾病率的上升、對預防通訊協定的日益重視以及防護和消毒技術的不斷創新。全球醫療系統日益重視降低感染風險,以改善患者預後並降低治療成本。長期健康問題的日益增多增加了患者與醫療機構的接觸,提高了感染風險,並進一步強化了對強力的感染預防措施的需求。免疫功能低下的患者需要加強保護,這進一步推動了對先進感染控制解決方案的需求。全球重症監護和外科手術能力的提升也促進了現代消毒和滅菌技術的廣泛應用。隨著醫療機構更加重視安全、效率和合規性,感染控制用品已成為臨床運作的重要組成部分,從而支持了醫院、診所和門診機構市場的持續成長。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 564億美元 |

| 市場規模預測 | 1061億美元 |

| 複合年成長率 | 6.8% |

預計到2025年,消毒劑品類將創造154億美元的收入,佔市場佔有率的27.2%。由於人們對衛生標準的認知不斷提高以及合規要求日益嚴格,醫療機構對消毒劑的需求仍然強勁。法律規範和以衛生為中心的政策也進一步推動了醫療機構對消毒劑的採用。

2025年,批發分銷管道的價值將達到257億美元。這些仲介業者在確保獲得必要的感染控制產品方面發揮著至關重要的作用。它們的規模、定價柔軟性和物流能力使它們成為需要確保穩定供應的大規模醫療機構的首選採購管道。

預計到2024年,北美感染控制用品市佔率將達到42.5%。該地區的領先地位得益於其完善的醫療基礎設施、高度的感染預防意識以及嚴格的監管執行。醫療程序的不斷增加和機構合規要求的嚴格性也持續支撐全部區域穩定的需求。

目錄

第1章:分析方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 產業影響因素

- 促進要素

- 醫療相關感染(HAI)激增

- 人口老化趨勢日益加劇

- 慢性病發生率呈上升趨勢

- 提高公共衛生意識

- 產業潛在風險與挑戰

- 缺乏感染控制和預防意識

- 缺乏衛生知識

- 市場機遇

- 擴建門診及門診治療設施

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 技術進步

- 當前技術趨勢

- 新興技術

- 價格分析(2024)

- 未來市場趨勢

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 企業矩陣分析

- 主要企業的競爭分析

- 競爭定位矩陣

- 主要趨勢

- 企業合併(M&A)

- 合夥/合資企業

- 新產品發布

- 擴張計劃

第5章 按產品分類的市場估算與預測(2022-2035 年)

- 消毒劑

- 產品類型

- 乾洗手劑

- 表面消毒劑

- 皮膚消毒劑

- 器械消毒劑

- 劑型

- 消毒紙巾

- 液體消毒劑

- 消毒噴霧

- 美國環保署分類

- 低效率消毒劑

- 中級消毒劑

- 高效消毒劑

- 產品類型

- 清潔配件

- 清潔和消毒設備

- 超音波清洗器

- 清洗消毒機

- 紫外線消毒器

- 清洗消毒機

- 一次性安全產品

- 外科用覆蓋巾及罩衣

- 口罩

- 風鏡

- 手套

- 蓋子和封口

- 其他一次性安全產品

- 其他產品

第6章 按分銷管道分類的市場估算與預測(2022-2035 年)

- 批發商

- 零售商

- 藥局

- 電子商務

- 其他分銷管道

7. 依最終用途分類的市場估計與預測(2022-2035 年)

- 醫院和診所

- 醫療設備製造商

- 製藥公司

- 研究所

- 其他最終用途

第8章 各地區市場估算與預測(2021-2034 年)

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- 3M

- Advanced Sterilization Products(ASP)

- Belimed Deutschland GmbH(Metal Zug Group)

- Cardinal Health

- Cantel Medical

- Dentsply Sirona

- Ecolab

- Envista Holdings Corporation

- Getinge

- Henry Schein

- Kimberly-Clark Corporation

- Matachana Group

- Reckitt

- Steelco

- Steris

The Global Infection Control Supplies Market was valued at USD 56.4 billion in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 106.1 billion by 2035.

Market growth is supported by the rising incidence of infectious conditions within healthcare environments, increased emphasis on prevention protocols, and continuous innovation in protective and disinfection technologies. Healthcare systems worldwide are placing greater priority on minimizing infection risks to improve patient outcomes and reduce treatment costs. The growing burden of long-term health conditions has intensified interactions with healthcare facilities, increasing exposure risks and reinforcing the need for robust infection prevention measures. Patients with compromised immunity require heightened protection, further driving demand for advanced infection control solutions. Expansion of critical care and surgical capacity globally has also contributed to higher utilization of modern disinfection and sterilization technologies. As healthcare providers focus on safety, efficiency, and regulatory compliance, infection control supplies have become a fundamental component of clinical operations, supporting sustained market expansion across hospitals, clinics, and outpatient care settings.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $56.4 Billion |

| Forecast Value | $106.1 Billion |

| CAGR | 6.8% |

The disinfectants category generated USD 15.4 billion during 2025 and accounted for a 27.2% share. Strong demand continues across healthcare environments due to heightened awareness of sanitation standards and strict compliance requirements. Regulatory oversight and hygiene-focused policies continue to reinforce adoption across medical facilities.

The wholesalers distribution channel reached USD 25.7 billion in 2025. These intermediaries play a critical role in ensuring reliable access to essential infection control products. Their scale, pricing flexibility, and logistical capabilities make them a preferred sourcing option for large healthcare organizations that require consistent supply availability.

North America Infection Control Supplies Market represented 42.5% share in 2024. Regional dominance is supported by a well-developed healthcare infrastructure, high awareness of infection prevention, and strict regulatory enforcement. Rising procedural volumes and strong institutional compliance requirements continue to support stable demand across the region.

Key companies active in the Global Infection Control Supplies Market include Ecolab, 3M, Steris, Getinge, Cardinal Health, Kimberly-Clark Corporation, Henry Schein, Reckitt, Advanced Sterilization Products, Belimed Deutschland GmbH, Steelco, Cantel Medical, Matachana Group, Dentsply Sirona, and Envista Holdings Corporation. Companies operating in the Global Infection Control Supplies Market are strengthening their market position through innovation, portfolio expansion, and strategic partnerships. Manufacturers are investing in advanced product development to improve effectiveness, safety, and ease of use. Expansion of automated and digital-enabled solutions is enhancing efficiency and compliance for healthcare providers. Strategic collaborations with hospitals and distributors help secure long-term supply contracts.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Distribution channel trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in healthcare-associated infections (HAIs)

- 3.2.1.2 Rising geriatric population base

- 3.2.1.3 Growing prevalence of chronic diseases

- 3.2.1.4 Increasing public health awareness

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of awareness regarding infection control and prevention

- 3.2.2.2 Insufficient knowledge related to hygienic conditions

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of outpatient and ambulatory care facilities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis, 2024

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Disinfectants

- 5.2.1 Product type

- 5.2.1.1 Hand disinfectants

- 5.2.1.2 Surface disinfectants

- 5.2.1.3 Skin disinfectants

- 5.2.1.4 Instrument disinfectants

- 5.2.2 Formulation

- 5.2.2.1 Disinfectant wipes

- 5.2.2.2 Liquid disinfectants

- 5.2.2.3 Disinfectant sprays

- 5.2.3 EPA classification

- 5.2.3.1 Low-level disinfectants

- 5.2.3.2 Intermediate-level disinfectants

- 5.2.3.3 High-level disinfectants

- 5.2.1 Product type

- 5.3 Cleaning accessories

- 5.4 Cleaning and disinfection equipment

- 5.4.1 Ultrasonic cleaners

- 5.4.2 Flusher disinfectors

- 5.4.3 UV-ray disinfectors

- 5.4.4 Washer disinfectors

- 5.5 Disposable safety products

- 5.5.1 Surgical drapes and gowns

- 5.5.2 Face masks

- 5.5.3 Goggles

- 5.5.4 Gloves

- 5.5.5 Covers and closures

- 5.5.6 Others disposable safety products

- 5.6 Other products

Chapter 6 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Wholesalers

- 6.3 Retailers

- 6.4 Pharmacies

- 6.5 E-commerce

- 6.6 Other distribution channels

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals and clinics

- 7.3 Medical device companies

- 7.4 Pharmaceutical companies

- 7.5 Research laboratories

- 7.6 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 3M

- 9.2 Advanced Sterilization Products (ASP)

- 9.3 Belimed Deutschland GmbH (Metal Zug Group)

- 9.4 Cardinal Health

- 9.5 Cantel Medical

- 9.6 Dentsply Sirona

- 9.7 Ecolab

- 9.8 Envista Holdings Corporation

- 9.9 Getinge

- 9.10 Henry Schein

- 9.11 Kimberly-Clark Corporation

- 9.12 Matachana Group

- 9.13 Reckitt

- 9.14 Steelco

- 9.15 Steris

感染控制用品市場:依類型、通路、最終用戶、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

感染控制用品市場:依類型、通路、最終用戶、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測 感染控制市場報告:按類型、最終用戶和地區分類(2026-2034 年)

感染控制市場報告:按類型、最終用戶和地區分類(2026-2034 年) 感染控制服飾市場-全球產業規模、佔有率、趨勢、機會與預測:按產品、最終用途、地區和競爭格局分類,2021-2031年

感染控制服飾市場-全球產業規模、佔有率、趨勢、機會與預測:按產品、最終用途、地區和競爭格局分類,2021-2031年 感染控制市場:全球市場依產品類型、技術、應用、通路和最終用戶分類的預測-2026-2032年

感染控制市場:全球市場依產品類型、技術、應用、通路和最終用戶分類的預測-2026-2032年 全球感染控制市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球感染控制市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球感染控制用品市場報告日本感染控制市場報告(按類型(設備消毒器、滅菌設備、服務、耗材)、最終用途(醫院、醫療器材公司、臨床實驗室、製藥公司及其他)和地區分類,2026-2034年)

2026年全球感染控制用品市場報告日本感染控制市場報告(按類型(設備消毒器、滅菌設備、服務、耗材)、最終用途(醫院、醫療器材公司、臨床實驗室、製藥公司及其他)和地區分類,2026-2034年) 感染控制市場規模、佔有率和成長分析(按產品、應用、通路、最終用戶和地區分類)-2026-2033年產業預測

感染控制市場規模、佔有率和成長分析(按產品、應用、通路、最終用戶和地區分類)-2026-2033年產業預測 全球感染控制市場按產品/服務、最終用戶和地區分類-預測至2030年2025年感染控制全球市場報告

全球感染控制市場按產品/服務、最終用戶和地區分類-預測至2030年2025年感染控制全球市場報告