|

市場調查報告書

商品編碼

1913332

無線充電市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)Wireless Charging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

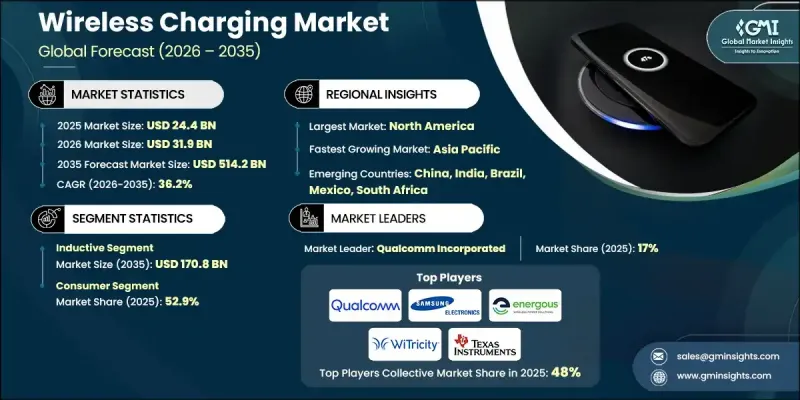

全球無線充電市場預計到 2025 年將達到 244 億美元,到 2035 年將達到 5,142 億美元,年複合成長率為 36.2%。

市場成長的驅動力來自消費性電子產品的日益普及、技術的快速發展、電動車的快速普及以及政府鼓勵充電基礎設施建設的扶持政策。隨著電動車普及速度的加快,對便利、無線充電解決方案的需求持續成長。無線充電技術,例如無線充電板和動態路邊充電系統,無需實體連接器,簡化了充電過程。諸如諧振和射頻技術等能夠提高速度、效率和柔軟性的技術創新,正在提升智慧型手機、筆記型電腦、穿戴式裝置和其他電子設備無線充電的實用性。這些進步正在突破傳統技術的限制,拓展應用領域,並加速其在消費性電子和汽車產業的商業化進程。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 244億美元 |

| 預測金額 | 5142億美元 |

| 複合年成長率 | 36.2% |

預計到 2025 年,諧振無線充電市場規模將達到 82 億美元,從 2025 年到 2034 年的複合年成長率將達到 38.8%。諧振技術無需精確對準即可實現中等距離的功率傳輸,使其適用於消費性電子產品和汽車應用,包括基於停車場的和動態電動車充電系統。

截至2025年,消費者市場將佔據52.9%的市場。智慧型手機、耳機、穿戴式裝置和行動裝置無線充電技術的快速普及,得益於多線圈解決方案、高效充電器以及與家庭、辦公室和公共場所的無縫整合。 Qi2等舉措和消費者意識的不斷提高,進一步推動了無線充電技術的普及,同時,各公司也不斷推出創新產品,例如嵌入式家具和美觀的整合式充電系統。

預計到2025年,北美無線充電市佔率將達到34%。該地區的成長得益於家用電器和電動車的廣泛應用,而這又得益於高效感應技術的進步和用戶體驗的提升。作為創新中心,美國擁有許多致力於開發尖端無線充電系統的大型科技公司和研究中心,同時,良好的法規環境和不斷完善的電動車基礎設施也進一步推動了市場的擴張。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 家用電子電器的普及率不斷提高

- 無線充電技術的進步

- 電動車(EV)的成長

- 政府措施和法規

- 產業潛在風險與挑戰

- 無線充電系統成本高昂

- 充電範圍限制

- 市場機遇

- 遠端動態充電技術的創新

- 商業設施中託管無線充電服務的機遇

- 促進要素

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

- 地緣政治和貿易趨勢

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 主要企業的競爭標竿分析

- 財務績效比較

- 收入

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線的廣度

- 科技

- 創新

- 區域比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導企業

- 受讓人

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年主要發展動態

- 併購

- 合作夥伴關係和合資企業

- 技術進步

- 擴張與投資策略

- 數位轉型計劃

- 新興/Start-Ups競賽的趨勢

第5章 按技術分類的市場估算與預測,2022-2035年

- 指導方法

- RF

- 諧振

- 其他

第6章 按應用領域分類的市場估算與預測,2022-2035年

- 車

- 消費者使用

- 工業的

- 衛生保健

- 航太/國防

- 其他

第7章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第8章 公司簡介

- 主要企業

- Qualcomm Incorporated

- Samsung Electronics, Co., Ltd.

- Texas Instruments, Inc.

- Infineon Technologies

- 按地區分類的主要企業

- 北美洲

- Energizer Holdings Inc.

- Powermat Technologies

- Evatran LLC(Plugless Power)

- 歐洲

- Wiferion GmbH

- Renesas Electronics

- Leggett &Platt, Inc

- 亞太地區

- MediaTek, Inc.

- Murata Manufacturing Co. Ltd.

- Semtech Corporation

- 北美洲

- 小眾玩家/顛覆者

- Convenient Power Ltd.

- Mojo Mobility, Inc.

- OSSIA

- Powercast Corporation

- WiBotic

- WiTricity Corporation

The Global Wireless Charging Market was valued at USD 24.4 billion in 2025 and is estimated to grow at a CAGR of 36.2% to reach USD 514.2 billion by 2035.

Market expansion is fueled by rising adoption of consumer electronics, rapid technological advancements, increasing deployment in electric vehicles, and supportive government policies promoting charging infrastructure development. As EV adoption accelerates, the demand for convenient, cable-free charging solutions continues to rise. Wireless charging technologies, such as pads and dynamic in-road systems, simplify the process by eliminating the need for physical connectors. Innovations enhancing speed, efficiency, and flexibility-including resonant and radio frequency-based solutions-are making wireless charging increasingly practical for smartphones, laptops, wearables, and other electronics. These advancements address previous limitations, expand application opportunities, and accelerate commercialization across consumer and automotive sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $24.4 Billion |

| Forecast Value | $514.2 Billion |

| CAGR | 36.2% |

The resonant wireless charging segment accounted for USD 8.2 billion in 2025 and is expected to grow at a CAGR of 38.8% during 2025-2034. Resonant technology allows mid-range power transfer without precise alignment, making it suitable for both consumer electronics and automotive applications, including parking-based and dynamic EV charging systems.

The consumer segment held a 52.9% share in 2025. Rapid adoption of wireless charging across smartphones, earbuds, wearables, and portable devices is being driven by multi-coil solutions, high-efficiency chargers, and seamless integration into homes, offices, and public spaces. Standardization initiatives such as Qi2 and increasing consumer awareness are further enhancing adoption, while companies continue to offer innovative products like furniture-embedded and aesthetically integrated charging systems.

North America Wireless Charging Market held a 34% share in 2025. Growth in the region is supported by strong adoption in consumer electronics and electric vehicles, driven by advancements in high-efficiency inductive technologies and improved user experience. The U.S., as a hub of innovation, hosts key technology firms and research centers developing cutting-edge wireless charging systems, while favorable regulations and growing EV infrastructure further support market expansion.

Key companies operating in the Global Wireless Charging Market include Samsung Electronics Co., Ltd., Qualcomm Incorporated, Infineon Technologies, Powermat Technologies, Mojo Mobility, Inc., Wiferion GmbH, Evatran LLC (Plugless Power), Powercast Corporation, Energizer Holdings Inc., WiTricity Corporation, WiBotic, Murata Manufacturing Co. Ltd., Convenient Power Ltd., Renesas Electronics, OSSIA, Texas Instruments, Inc., MediaTek, Inc., and Leggett & Platt, Inc. Companies in the Global Wireless Charging Market are employing several strategies to strengthen their presence and expand market share. Investments in research and development are enhancing charging efficiency, reducing power loss, and enabling faster wireless energy transfer. Firms are forming partnerships with automotive manufacturers, consumer electronics brands, and infrastructure providers to integrate wireless charging solutions across devices and EVs. Market players are also expanding regional production and distribution networks to reach emerging economies. Additionally, companies focus on standardization compliance, user-friendly designs, and multifunctional products to improve adoption.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Technology trends

- 2.2.2 Application trends

- 2.2.3 Regional trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased adoption in consumer electronics

- 3.2.1.2 Advancements in wireless charging technology

- 3.2.1.3 Growth of electric vehicles (EVs)

- 3.2.1.4 Government initiatives and regulations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Higher cost of wireless charging systems

- 3.2.2.2 Limited charging range

- 3.2.3 Market opportunities

- 3.2.3.1 Innovation in long-range and dynamic charging technologies

- 3.2.3.2 Opportunities for managed wireless charging services in commercial spaces

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter's analysis

- 3.5 PESTEL analysis

- 3.6 Technology and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Emerging business models

- 3.8 Compliance requirements

- 3.9 Patent and IP analysis

- 3.10 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Technology, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Inductive

- 5.3 RF

- 5.4 Resonant

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Automotive

- 6.3 Consumer

- 6.4 Industrial

- 6.5 Healthcare

- 6.6 Aerospace & Defense

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Global Key Players

- 8.1.1 Qualcomm Incorporated

- 8.1.2 Samsung Electronics, Co., Ltd.

- 8.1.3 Texas Instruments, Inc.

- 8.1.4 Infineon Technologies

- 8.2 Regional Key Players

- 8.2.1 North America

- 8.2.1.1 Energizer Holdings Inc.

- 8.2.1.2 Powermat Technologies

- 8.2.1.3 Evatran LLC (Plugless Power)

- 8.2.2 Europe

- 8.2.2.1 Wiferion GmbH

- 8.2.2.2 Renesas Electronics

- 8.2.2.3 Leggett & Platt, Inc

- 8.2.3 APAC

- 8.2.3.1 MediaTek, Inc.

- 8.2.3.2 Murata Manufacturing Co. Ltd.

- 8.2.3.3 Semtech Corporation

- 8.2.1 North America

- 8.3 Niche Players / Disruptors

- 8.3.1 Convenient Power Ltd.

- 8.3.2 Mojo Mobility, Inc.

- 8.3.3 OSSIA

- 8.3.4 Powercast Corporation

- 8.3.5 WiBotic

- 8.3.6 WiTricity Corporation

家用電子電器無線充電市場:依產品、組件、技術、銷售管道和應用分類-2026-2032年全球市場預測無線充電市場:按組件、技術類型、應用和最終用戶分類-2026-2032年全球市場預測

家用電子電器無線充電市場:依產品、組件、技術、銷售管道和應用分類-2026-2032年全球市場預測無線充電市場:按組件、技術類型、應用和最終用戶分類-2026-2032年全球市場預測 2026年全球無線充電市場報告

2026年全球無線充電市場報告 無線充電市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、設備、最終用戶、安裝類型及解決方案分類

無線充電市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、設備、最終用戶、安裝類型及解決方案分類 全球無線充電市場規模、佔有率、趨勢和成長分析報告(2026-2034年)家用電子電器充電器市場按產品類型、連接器類型、分銷管道、應用和最終用戶分類-2026年至2032年全球預測

全球無線充電市場規模、佔有率、趨勢和成長分析報告(2026-2034年)家用電子電器充電器市場按產品類型、連接器類型、分銷管道、應用和最終用戶分類-2026年至2032年全球預測 日本無線充電市場報告(按技術、傳輸範圍、應用和地區分類,2026-2034 年)

日本無線充電市場報告(按技術、傳輸範圍、應用和地區分類,2026-2034 年) 無線充電市場按組件、技術、應用和地區分類

無線充電市場按組件、技術、應用和地區分類 消費性電子充電線市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)無線充電模組市場:2025-2030 年預測

消費性電子充電線市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)無線充電模組市場:2025-2030 年預測