|

市場調查報告書

商品編碼

1913320

無人交通管理市場機會、成長要素、產業趨勢分析及2026年至2035年預測Unmanned Traffic Management Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

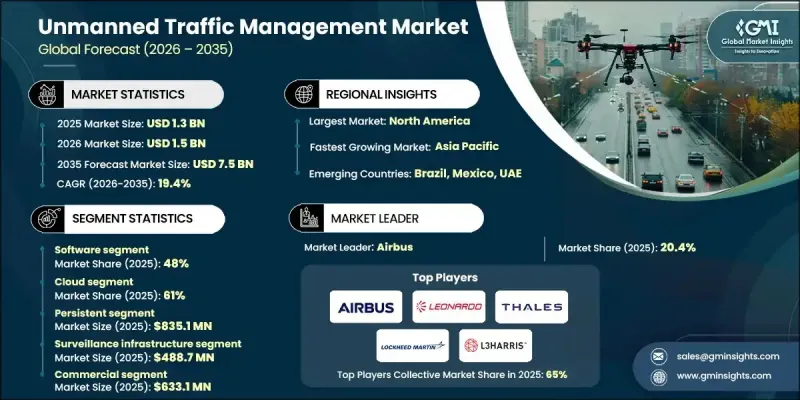

全球無人交通管理市場預計到 2025 年將達到 13 億美元,到 2035 年將達到 75 億美元,年複合成長率為 19.4%。

市場成長主要受商業和政府無人機營運的快速成長、對安全低空空域管理日益成長的需求以及無人機交通監管框架不斷演進的推動。隨著各組織和機構致力於將無人機(UAV)安全地融入共用空域,先進的無人機交通管理(UTM)解決方案對於及時、安全且可追蹤的無人機運作至關重要。此外,對提升無人機監控、飛行規劃和營運效率的技術投入不斷增加,也促進了市場擴張。各行業的相關人員都在優先考慮端到端、數據驅動的系統,這些系統能夠提供即時情境察覺、減少空域衝突,並支援擴充性的長期空中交通管理策略。這些進步已使UTM解決方案成為全球安全高效無人機運作的關鍵基礎技術。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 13億美元 |

| 預測金額 | 75億美元 |

| 複合年成長率 | 19.4% |

人工智慧和機器學習飛行路徑最佳化、物聯網即時追蹤、GPS和ADS-B監控、基於雲端的無人機交通管理平台以及自動化無人機協調系統等技術創新正在變革傳統的空域管理。這些工具能夠全面掌控無人機運行,從任務規劃和即時監控到碰撞偵測和合規性,無所不包。整合數位平台、自動化和分析技術的進步正在提高效率、降低風險並增強運行安全性,從而推動市場成長。

軟體領域佔了48%的市場佔有率,預計到2035年將以20.1%的複合年成長率成長。軟體的主導地位源自於其在無人機即時追蹤、空域監控、飛行路徑最佳化和綜合交通管理方面的核心作用。基於雲端的無人機交通管理(UTM)平台、人工智慧驅動的分析、物聯網監控和行動應用,能夠幫助營運商、監管機構和商業用戶有效地協調無人機運作、維護空域安全並最佳化效能。

預計到2025年,雲端解決方案將佔據61%的市場佔有率,並在2035年之前以18.8%的複合年成長率成長。擴充性、即時數據存取和低實施成本正在推動雲端解決方案的主流化應用,使營運商和監管機構能夠監控無人機交通、最佳化飛行路徑、檢測潛在衝突並管理跨多個區域的空域。其柔軟性和整合能力使雲端平台成為大規模無人機作業的理想選擇。

預計到2025年,美國無人機交通管理市場將佔據78%的佔有率,市場規模將達到3.671億美元。北美憑藉著成熟的無人機生態系統、先進的空域基礎設施以及對數位化空中交通管理技術的早期應用,在全球市場中佔據領先地位。該地區受益於雲端平台、人工智慧分析、物聯網追蹤和即時監控的廣泛應用。

全球無人機交通管理市場的主要企業包括 Leonardo、L3Harris、洛克希德·馬丁、空中巴士、Altitude Angel、PrecisionHawk、Frequentiss、泰雷茲和 Unifly。這些公司正透過大力投資軟體和雲端解決方案來增強其市場地位,這些解決方案能夠提升即時空域監控和自動衝突解決能力。他們正與無人機運營商、監管機構和技術提供商建立戰略夥伴關係,以建立端到端的無人機管理整合平台。人工智慧、機器學習和物聯網系統的持續研發正在幫助企業改善飛行路徑最佳化、情境察覺和預測分析。此外,多家公司正在拓展其全球業務,以服務高成長地區,並提升擴充性、合規性和客戶參與。專注於柔軟性、互通性和數據驅動型解決方案將使企業能夠建立長期競爭優勢並佔據更大的市場佔有率。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 商業無人機運作的快速擴張

- 監管要求和安全標準

- 技術進步

- 拓展城市空中運輸(UAM)和超視距飛行(BVLOS)

- 產業潛在風險與挑戰

- 分裂世界中的監管

- 前期成本高

- 市場機遇

- 與智慧城市和物聯網網路整合

- 拓展新興市場

- 政府和國防部門引入無人機

- 進階分析和人工智慧驅動的最佳化

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 美國航空管理局(FAA)遠端識別法規

- 美國國家空域系統(NAS)指南

- 歐洲

- 德國聯邦交通運輸數位化部 (BMVI) 和德國聯邦航空局 (DFS) 的規定

- 法國民航總局 (DGAC) 和國家稅務局 (ANAF) 指南

- 英國民航局(CAA)和無人機系統(UAS)條例

- 義大利ENAC指南

- 亞太地區

- 中國民用航空局(CAAC)和無人機系統(UAS)規章

- 日本民航局無人機指南

- 韓國國土交通部(MOLIT)與無人機法規

- 印度民航局無人機法規與唯一識別碼系統

- 拉丁美洲

- 巴西ANAC和DECEA指南

- 墨西哥民航局無人機法規

- 中東和非洲

- 阿拉伯聯合大公國民航總局無人機法規

- 沙烏地阿拉伯民航局無人機指南

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 成本細分分析

- 專利分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

- 使用案例場景

- UTM系統結構和空域模型

- 集中式與分散式UTM架構

- 戰術性和戰略衝突消除

- 與載人空中交通管理系統整合

- 互通性和標準化框架

- UTM經營模式和獲利模式

- 相關人員生態系統和管治模型

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 企業擴張計畫和資金籌措

第5章 按組件分類的市場估算與預測,2022-2035年

- 軟體

- 硬體

- 服務

第6章 按類型分類的市場估算與預測,2022-2035年

- 執著的

- 不永續性

7. 2022-2035年各車型市場估計與預測

- 本地部署

- 雲

第8章 按應用領域分類的市場估算與預測,2022-2035年

- 監控基礎設施

- 通訊基礎設施

- 導航支援基礎設施

- 其他

9. 依最終用途分類的市場估計與預測,2022-2035 年

- 商業的

- 政府

- 私人的

第10章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 比利時

- 荷蘭

- 瑞典

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 新加坡

- 韓國

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第11章:公司簡介

- Global Player

- Airbus

- Altitude Angel

- Frequentis

- Honeywell International

- L3 Harris

- Leonardo

- Lockheed Martin

- PrecisionHawk

- Thales

- Unifly

- Regional Player

- AirMap

- Airspace Link

- ANRA Technologies

- Dedrone

- DroneDeploy

- Flytrex

- Kittyhawk

- SkyGrid

- Terra Drone

- uAvionix

- 新興企業

- Airborne Robotics

- Drone Harmony

- Simulyze

- UAV Navigation

Volocopter UT

The Global Unmanned Traffic Management Market was valued at USD 1.3 billion in 2025 and is estimated to grow at a CAGR of 19.4% to reach USD 7.5 billion by 2035.

Market growth is fueled by a rapid increase in commercial and governmental drone operations, heightened demand for safe low-altitude airspace management, and evolving regulatory frameworks governing drone traffic. As organizations and authorities focus on integrating unmanned aerial vehicles (UAVs) into shared airspace safely, advanced UTM solutions are becoming essential to enable timely, secure, and traceable drone operations. The market's expansion is also supported by rising investments in technology that enhance drone monitoring, flight planning, and operational efficiency. Stakeholders across industries are prioritizing end-to-end, data-driven systems that provide real-time situational awareness, reduce airspace conflicts, and support scalable, long-term air traffic management strategies. These developments position UTM solutions as critical enablers of safe and efficient UAV operations worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.3 Billion |

| Forecast Value | $7.5 Billion |

| CAGR | 19.4% |

Technological innovations, including AI- and ML-driven flight path optimization, IoT-enabled real-time tracking, GPS and ADS-B monitoring, cloud-based UTM platforms, and automated drone coordination systems, are transforming traditional airspace management. These tools provide full visibility and control over UAV operations, from mission planning and real-time monitoring to conflict detection and regulatory compliance. The market continues to evolve as integrated digital platforms, automation, and analytics improve efficiency, reduce risks, and enhance operational safety.

The software segment held 48% share and is projected to grow at a CAGR of 20.1% through 2035. Software dominates due to its pivotal role in real-time drone tracking, airspace monitoring, flight path optimization, and comprehensive traffic management. Cloud-based UTM platforms, AI-powered analytics, IoT monitoring, and mobile-enabled applications help operators, regulators, and commercial users coordinate UAV operations efficiently, maintain airspace safety, and optimize performance.

The cloud segment accounted for 61% share in 2025 and is expected to grow at a CAGR of 18.8% through 2035. Cloud solutions dominate because of their scalability, real-time data access, and lower deployment costs. They enable operators and regulators to monitor drone traffic, optimize flight paths, detect potential conflicts, and manage airspace across multiple regions. Their flexibility and integration capabilities make cloud platforms ideal for large-scale UAV operations.

U.S. Unmanned Traffic Management Market held 78% share, generating USD 367.1 million in 2025. North America leads the global market due to its mature drone ecosystem, advanced airspace infrastructure, and early adoption of digital air traffic management technologies. The region benefits from widespread deployment of cloud-based platforms, AI-powered analytics, IoT-enabled tracking, and real-time monitoring.

Key players in the Global Unmanned Traffic Management Market include Leonardo, L3Harris, Lockheed Martin, Airbus, Altitude Angel, PrecisionHawk, Frequentis, Thales, and Unifly. Companies in the Global Unmanned Traffic Management Market are strengthening their presence by investing heavily in software and cloud-based solutions that enhance real-time airspace monitoring and automated conflict resolution. They are forming strategic partnerships with drone operators, regulators, and technology providers to create integrated platforms for end-to-end UAV management. Continuous R&D in AI, machine learning, and IoT-enabled systems is helping firms improve flight path optimization, situational awareness, and predictive analytics. Several companies are also expanding globally to serve high-growth regions, enhancing scalability, regulatory compliance, and customer engagement. Focusing on flexible, interoperable, and data-driven solutions enables firms to build long-term competitive advantages and capture larger market share.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Type

- 2.2.4 Deployment Model

- 2.2.5 Application

- 2.2.6 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid Growth of Commercial Drone Operations

- 3.2.1.2 Regulatory Mandates & Safety Requirements

- 3.2.1.3 Technological Advancements

- 3.2.1.4 Urban Air Mobility & BVLOS Expansion

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Fragmented Global Regulations

- 3.2.2.2 High Initial Costs

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with Smart Cities & IoT Networks

- 3.2.3.2 Expansion into Emerging Markets

- 3.2.3.3 Government and Defense UAV Adoption

- 3.2.3.4 Advanced Analytics and AI-Driven Optimization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. FAA Remote ID Rules

- 3.4.1.2 U.S. National Airspace System (NAS) Guidelines

- 3.4.2 Europe

- 3.4.2.1 Germany BMVI & DFS Regulations

- 3.4.2.2 France DGAC & ANAF Guidelines

- 3.4.2.3 United Kingdom CAA & UAS Regulations

- 3.4.2.4 Italy ENAC Guidelines

- 3.4.3 Asia Pacific

- 3.4.3.1 China CAAC & UAS Regulations

- 3.4.3.2 Japan JCAB Drone Guidelines

- 3.4.3.3 South Korea MOLIT & Drone Regulations

- 3.4.3.4 India DGCA Drone Rules & UIN System

- 3.4.4 Latin America

- 3.4.4.1 Brazil ANAC & DECEA Guidelines

- 3.4.4.2 Mexico DGAC UAV Regulations

- 3.4.5 Middle East and Africa

- 3.4.5.1 UAE GCAA Drone Regulations

- 3.4.5.2 Saudi Arabia GACA Drone Guidelines

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and Environmental Aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Use case scenarios

- 3.13 UTM system architecture & airspace models

- 3.13.1 Centralized vs federated UTM architectures

- 3.13.2 Tactical vs strategic deconfliction

- 3.13.3 Integration with manned ATM systems

- 3.14 Interoperability & standards framework

- 3.15 UTM business & monetization models

- 3.16 Stakeholder ecosystem & governance model

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($ Bn)

- 5.1 Key trends

- 5.2 Software

- 5.3 Hardware

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By Type, 2022 - 2035 ($ Bn)

- 6.1 Key trends

- 6.2 Persistent

- 6.3 Non-persistent

Chapter 7 Market Estimates & Forecast, By Deployment Model, 2022 - 2035 ($ Bn)

- 7.1 Key trends

- 7.2 On premises

- 7.3 Cloud

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($ Bn)

- 8.1 Key trends

- 8.2 Surveillance infrastructure

- 8.3 Communication infrastructure

- 8.4 Navigation infrastructure

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($ Bn)

- 9.1 Key trends

- 9.2 Commercial

- 9.3 Government

- 9.4 Private

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($ Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Singapore

- 10.4.6 South Korea

- 10.4.7 Vietnam

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Global Player

- 11.1.1 Airbus

- 11.1.2 Altitude Angel

- 11.1.3 Frequentis

- 11.1.4 Honeywell International

- 11.1.5. L3 Harris

- 11.1.6 Leonardo

- 11.1.7 Lockheed Martin

- 11.1.8 PrecisionHawk

- 11.1.9 Thales

- 11.1.10 Unifly

- 11.2 Regional Player

- 11.2.1 AirMap

- 11.2.2 Airspace Link

- 11.2.3 ANRA Technologies

- 11.2.4 Dedrone

- 11.2.5 DroneDeploy

- 11.2.6 Flytrex

- 11.2.7 Kittyhawk

- 11.2.8 SkyGrid

- 11.2.9 Terra Drone

- 11.2.10 uAvionix

- 11.3 Emerging Players

- 11.3.1 Airborne Robotics

- 11.3.2 Drone Harmony

- 11.3.3 Simulyze

- 11.3.4 UAV Navigation

Volocopter UT