|

市場調查報告書

商品編碼

1913318

工業網路安全市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)Industrial Cybersecurity Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

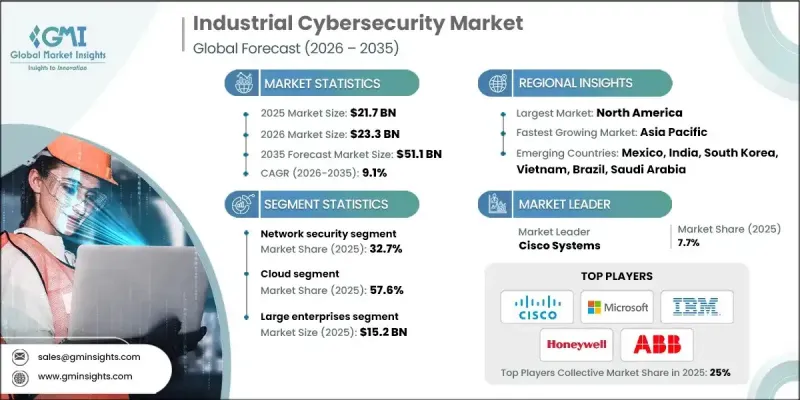

全球工業網路安全市場預計到 2025 年將達到 217 億美元,到 2035 年將達到 511 億美元,年複合成長率為 9.1%。

網路安全成長的驅動力在於針對營運系統的網路事件日益頻繁、複雜化程度不斷提高,且潛在影響也越來越大。隨著工業營運的互聯互通程度日益加深,保護關鍵基礎設施已成為至關重要的策略要務。許多工業環境中仍存在顯著的安全漏洞,導致監管機構的審查力度加大,企業面臨越來越大的壓力,必須加強網路防禦以避免大規模的經濟和營運中斷。人工智慧 (AI) 和機器學習的應用正在重塑網路安全範式,實現快速威脅偵測、預測分析和持續監控。這些技術提高了複雜工作流程的可見性,並提升了回應的準確性。政府的強制性規定和合規要求正在加速關鍵工業運作中網路安全的普及,使網路安全成為基礎設施現代化和長期風險管理策略的核心組成部分。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 217億美元 |

| 預測金額 | 511億美元 |

| 複合年成長率 | 9.1% |

到2025年,網路安全領域將佔據32.7%的市場。強勁的需求源自於保護互聯系統間即時資料交換通訊通道日益成長的需求。由於業務連續性高度依賴可靠的網路,因此保護資料流對於維護安全性、生產力和系統穩定性至關重要。

預計到 2025 年,雲端部署部分將佔 57.6% 的市場佔有率,從 2026 年到 2035 年的複合年成長率將達到 10.2%。基於雲端的網路安全解決方案對擁有分散式營運的組織尤其具有吸引力,因為它們可以在多個設施中提供集中式保護,而無需大量的初始投資。

預計到 2025 年,美國工業網路安全市場規模將達到 71 億美元。早期採用互聯技術以及對工業系統安全的大力投資鞏固了其市場領先地位,使其成為工業網路安全支出最高的地區。

目錄

第1章調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 關鍵基礎設施遭受網路攻擊的頻率增加

- 工業IoT(IIoT) 和智慧製造的日益普及

- 工業控制系統(ICS)日益數位化

- 嚴格的政府法規和合規要求

- 產業潛在風險與挑戰

- 工業網路安全專業人員短缺

- 中小企業網路安全意識不足

- 市場機遇

- 對人工智慧驅動的威脅偵測解決方案的需求日益成長

- 拓展新興經濟體的工業網路安全

- 工業領域對資安管理服務的需求不斷成長

- 對即時威脅情報和監控解決方案的需求

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- NIST網路安全框架(CSF)2.0

- NERC CIP

- ISA/IEC 62443

- NIST SP 800-82

- 歐洲

- NIS2 指令

- IEC 62443

- DORA

- 網路安全基礎

- 亞太地區

- 中國網路安全法(CSL)

- 經濟產業省網路安全管理指南

- 新加坡網路安全法

- SOCI法案

- 拉丁美洲

- ANEEL網路安全標準

- ANATEL 安全條例

- 智利網路安全基本法

- 中東和非洲

- 基本網路安全措施 (ECC)

- 2012年第5號聯邦法規(阿拉伯聯合大公國)

- 網路犯罪法(沙烏地阿拉伯)

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 成本細分分析

- 案例研究

- IT 和 OT 攻擊統計數據

- 針對IT的網路攻擊

- 針對營運技術 (OT) 的網路攻擊

- IT-OT融合與混合攻擊

- 來自先進產業和新興產業的威脅

- IT/OT攻擊的影響分析

- 技能和人才趨勢

- 勞動供需

- 工業網路安全技能缺口

- 培訓和認證項目

- 政府和產業為技能發展所採取的舉措

- 未來前景與機遇

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 企業擴張計畫和資金籌措

第5章 按組件分類的市場估算與預測,2022-2035年

- 解決方案

- 硬體

- 軟體

- 服務

- 託管服務

- 專業服務

第6章 2022-2035年按產品分類的市場估算與預測

- SCADA

- 身分和存取管理 (IAM)

- 統一威脅管理 (UTM)

- 預防資料外泄(DLP)

- IDS/IPS

- SIEM

- DDoS

- 其他

7. 2022-2035年各車型市場估計與預測

- 雲

- 本地部署

- 混合

第8章 依公司規模分類的市場估計與預測,2022-2035年

- 小型企業

- 主要企業

第9章 證券市場估價與預測,2022-2035年

- 網路安全

- 端點安全

- 應用程式安全

- 雲端安全

- 無線安全

- 其他

第10章 2022-2035年各產業市場估計與預測

- 車

- 電子設備

- 食品/飲料

- 能源與電力

- 石油和天然氣

- 化學

- 資訊科技/通訊

- 航太與國防

- 其他

第11章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 比荷盧經濟聯盟

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ANZ

- 新加坡

- 馬來西亞

- 印尼

- 越南

- 泰國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- 世界公司

- Siemens

- Honeywell

- Palo Alto Networks

- Cisco Systems

- Microsoft

- IBM

- Fortinet

- Schneider Electric

- Rockwell Automation

- Claroty

- Nozomi Networks

- Dragos

- Tenable

- ABB

- Thales

- 本地公司

- Armis

- Darktrace

- TXOne Networks

- Waterfall Security

- Radiflow

- Industrial Defender

- Trend Micro

- ABS Group

- Check Point

- Forescout

- 新興企業

- Fox-IT

- ONEKEY

- ACURITY

- Keeper Security

- Underwriters Laboratories

The Global Industrial Cybersecurity Market was valued at USD 21.7 billion in 2025 and is estimated to grow at a CAGR of 9.1% to reach USD 51.1 billion by 2035.

Growth is driven by the rising frequency, sophistication, and potential impact of cyber incidents targeting operational systems. As industrial operations become increasingly interconnected, protecting critical infrastructure has become a top strategic priority. Many industrial environments still face significant security gaps, which has intensified regulatory oversight and increased pressure on organizations to strengthen cyber defenses to avoid large-scale economic and operational disruption. The adoption of artificial intelligence and machine learning is reshaping cybersecurity frameworks by enabling faster threat detection, predictive analysis, and continuous monitoring. These technologies improve visibility across complex workflows and enhance response accuracy. Government mandates and compliance requirements are accelerating cybersecurity implementation across critical industrial operations, making cybersecurity a core element of infrastructure modernization and long-term risk management strategies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $21.7 Billion |

| Forecast Value | $51.1 Billion |

| CAGR | 9.1% |

The network security segment held a 32.7% share in 2025. Strong demand is driven by the need to secure communication channels that support real-time data exchange across interconnected systems. As operational continuity depends heavily on reliable networks, protecting data flows has become essential for maintaining safety, productivity, and system stability.

The cloud deployment segment accounted for 57.6% share in 2025 and is expected to grow at a CAGR of 10.2% from 2026 to 2035. Cloud-based cybersecurity solutions enable centralized protection across multiple facilities without requiring extensive upfront investment, making them especially attractive for organizations with distributed operations.

U.S. Industrial Cybersecurity Market reached USD 7.1 billion in 2025. Market leadership is supported by early adoption of connected technologies and strong investment in securing industrial systems, resulting in the highest regional spending on industrial cybersecurity.

Key companies operating in the Global Industrial Cybersecurity Market include Schneider Electric, IBM, Cisco Systems, Honeywell, Palo Alto Networks, ABB, Rockwell Automation, Thales, Microsoft, and Claroty. Companies in the Global Industrial Cybersecurity Market strengthen their competitive position through continuous innovation and integrated security offerings. Firms invest heavily in AI-driven threat detection, real-time monitoring, and predictive analytics to enhance protection capabilities. Strategic partnerships and ecosystem collaborations help expand solution compatibility across industrial platforms. Companies focus on scalable cloud-based architectures to support distributed operations efficiently. Expanding service portfolios to include consulting, risk assessment, and managed security services improves customer retention. Compliance-focused solutions aligned with regulatory requirements further strengthen trust.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Product

- 2.2.4 Deployment Model

- 2.2.5 Enterprise Size

- 2.2.6 Security

- 2.2.7 Industry

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising frequency of cyberattacks on critical infrastructure

- 3.2.1.2 Increasing adoption of industrial IoT (IIoT) and smart manufacturing

- 3.2.1.3 Growing digitalization of industrial control systems (ICS)

- 3.2.1.4 Strict government regulations and compliance mandates

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of skilled industrial cybersecurity professionals

- 3.2.2.2 Limited cybersecurity awareness among SMEs

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for AI-driven threat detection solutions

- 3.2.3.2 Expansion of industrial cybersecurity in emerging economies

- 3.2.3.3 Rising need for managed security services in industries

- 3.2.3.4 Demand for real-time threat intelligence and monitoring solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 NIST Cybersecurity Framework (CSF) 2.0

- 3.4.1.2 NERC CIP

- 3.4.1.3 ISA/IEC 62443

- 3.4.1.4 NIST SP 800-82

- 3.4.2 Europe

- 3.4.2.1 NIS2 Directive

- 3.4.2.2 IEC 62443

- 3.4.2.3 DORA

- 3.4.2.4 Cyber Essentials

- 3.4.3 Asia Pacific

- 3.4.3.1 China's Cybersecurity Law (CSL)

- 3.4.3.2 METI Cybersecurity Management Guidelines

- 3.4.3.3 Singapore Cybersecurity Act

- 3.4.3.4 SOCI Act

- 3.4.4 Latin America

- 3.4.4.1 ANEEL Cybersecurity Norms

- 3.4.4.2 ANATEL Security Regulations

- 3.4.4.3 Chile Framework Law on Cybersecurity

- 3.4.5 Middle East & Africa

- 3.4.5.1 Essential Cybersecurity Controls (ECC)

- 3.4.5.2 Federal Decree-Law No. 5/2012 (UAE)

- 3.4.5.3 Cybercrime Law (Saudi Arabia)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Case studies

- 3.11 IT and OT attacks statistics

- 3.11.1 IT-focused cyberattacks

- 3.11.2 OT-focused cyberattacks

- 3.11.3 IT-OT convergence & hybrid attacks

- 3.11.4 Advanced & emerging industrial threats

- 3.11.5 Impact analysis of IT & OT attacks

- 3.12 Skills & talent landscape

- 3.12.1 Workforce availability and demand

- 3.12.2 Skill gaps in industrial cybersecurity

- 3.12.3 Training and certification programs

- 3.12.4 Government and industry initiatives for skill development

- 3.13 Future outlook & opportunities

- 3.14 Sustainability and Environmental Aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly initiatives

- 3.14.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Solution

- 5.2.1 Hardware

- 5.2.2 Software

- 5.3 Services

- 5.3.1 Managed services

- 5.3.2 Professional services

Chapter 6 Market Estimates & Forecast, By Product, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 SCADA

- 6.3 Identity and Access Management (IAM)

- 6.4 Unified Threat Management (UTM)

- 6.5 Data Loss Prevention (DLP)

- 6.6 IDS/IPS

- 6.7 SIEM

- 6.8 DDoS

- 6.9 Others

Chapter 7 Market Estimates & Forecast, By Deployment Model, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Cloud

- 7.3 On-premises

- 7.4 Hybrid

Chapter 8 Market Estimates & Forecast, By Enterprise Size, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 SMEs

- 8.3 Large enterprises

Chapter 9 Market Estimates & Forecast, By Security, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 Network security

- 9.3 Endpoint security

- 9.4 Application security

- 9.5 Cloud security

- 9.6 Wireless security

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By Industry, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 Automotive

- 10.3 Electronics

- 10.4 Food & beverages

- 10.5 Energy & power

- 10.6 Oil & gas

- 10.7 Chemical

- 10.8 IT & Telecommunications

- 10.9 Aerospace & Defense

- 10.10 Others

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.3.8 Benelux

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Singapore

- 11.4.7 Malaysia

- 11.4.8 Indonesia

- 11.4.9 Vietnam

- 11.4.10 Thailand

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Colombia

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global companies

- 12.1.1 Siemens

- 12.1.2 Honeywell

- 12.1.3 Palo Alto Networks

- 12.1.4 Cisco Systems

- 12.1.5 Microsoft

- 12.1.6 IBM

- 12.1.7 Fortinet

- 12.1.8 Schneider Electric

- 12.1.9 Rockwell Automation

- 12.1.10 Claroty

- 12.1.11 Nozomi Networks

- 12.1.12 Dragos

- 12.1.13 Tenable

- 12.1.14 ABB

- 12.1.15 Thales

- 12.2 Regional companies

- 12.2.1 Armis

- 12.2.2 Darktrace

- 12.2.3 TXOne Networks

- 12.2.4 Waterfall Security

- 12.2.5 Radiflow

- 12.2.6 Industrial Defender

- 12.2.7 Trend Micro

- 12.2.8 ABS Group

- 12.2.9 Check Point

- 12.2.10 Forescout

- 12.3 Emerging companies

- 12.3.1 Fox-IT

- 12.3.2 ONEKEY

- 12.3.3 ACURITY

- 12.3.4 Keeper Security

- 12.3.5 Underwriters Laboratories

工業網路安全市場:依安全類型、交付方式、部署方式和產業分類-2026-2032年全球市場預測

工業網路安全市場:依安全類型、交付方式、部署方式和產業分類-2026-2032年全球市場預測 2026年全球機器人網路安全市場報告

2026年全球機器人網路安全市場報告 OT 安全解決方案 - 全球市場佔有率和排名、總收入和需求預測(2026-2032 年)2026年全球工業網路安全市場報告2026年工業自動化全球網路安全市場報告

OT 安全解決方案 - 全球市場佔有率和排名、總收入和需求預測(2026-2032 年)2026年全球工業網路安全市場報告2026年工業自動化全球網路安全市場報告 工業網路安全市場規模、佔有率、趨勢和預測:按組件、安全類型、行業和地區分類,2026-2034 年

工業網路安全市場規模、佔有率、趨勢和預測:按組件、安全類型、行業和地區分類,2026-2034 年 工業網路安全市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶及解決方案分類

工業網路安全市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶及解決方案分類 全球工業網路安全市場規模、佔有率、趨勢和成長分析報告(2026-2034)OT保全服務市場按組件類型、安全類型、組織規模、垂直行業和部署模式分類 - 全球預測 2026-2032 年日本工業網路安全市場報告:按組件、安全類型、產業和地區分類(2026-2034年)

全球工業網路安全市場規模、佔有率、趨勢和成長分析報告(2026-2034)OT保全服務市場按組件類型、安全類型、組織規模、垂直行業和部署模式分類 - 全球預測 2026-2032 年日本工業網路安全市場報告:按組件、安全類型、產業和地區分類(2026-2034年)