|

市場調查報告書

商品編碼

1913308

積層軟管市場機會、成長要素、產業趨勢分析及2026年至2035年預測Laminated Tubes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

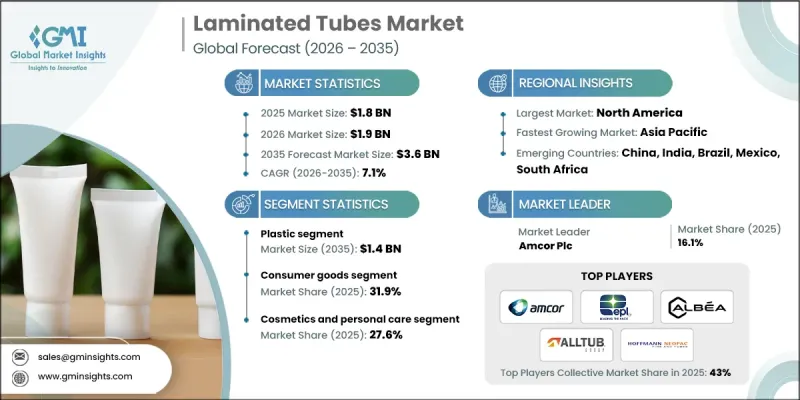

全球積層軟管市場預計到 2025 年將達到 18 億美元,到 2035 年將達到 36 億美元,年複合成長率為 7.1%。

市場成長得益於更嚴格的監管標準和消費者日益增強的環保意識。為了實現循環經濟目標,企業正擴大採用永續包裝手法,包括可回收和可生物分解材料。積層軟管旨在減少材料廢棄物並提高可回收性,幫助品牌在滿足不斷變化的消費者期望的同時,實現其永續性目標。此外,市場對安全、高阻隔阻隔性和合規包裝解決方案的需求不斷成長,尤其是在受監管目標產品方面,也推動了複合軟管的需求。積層軟管具有強大的防潮、防氧和防外部污染物性能,同時也能實現精準控制的分配。隨著業界越來越重視安全性、延長保存期限和合規性,對積層軟管包裝的需求持續成長。持續的材料創新和製造技術的改進進一步增強了複合軟管市場在多個終端應用領域的成長前景。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 18億美元 |

| 預測金額 | 36億美元 |

| 複合年成長率 | 7.1% |

預計到2035年,塑膠市場規模將達到14億美元。輕質、經濟、柔軟性和優異的阻隔性能等材料特性是推動強勁市場需求的主要因素。可再生聚合物和多層結構技術的不斷進步,也促進了塑膠的廣泛應用和更廣泛的認可。

預計到2025年,消費品產業將佔31.9%的市場佔有率。成長的驅動力在於市場對兼具耐用性、便利性和視覺吸引力的包裝解決方案的需求。對使用者體驗、貨架可見性和品牌差異化的日益重視,持續推動著管材結構、材料和印刷技術的創新。

到 2025 年,北美積層軟管市場將佔據 30% 的佔有率。該地區的需求得益於對優質和客製化包裝解決方案的積極採用、對永續性的重視,以及先進包裝製造商和全球品牌所有者的存在,這些因素共同推動了產品的持續發展。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 朝向永續和環保包裝的轉變

- 個人護理和化妝品行業的成長

- 管材印刷技術的進步

- 藥品包裝需求不斷成長

- 產業潛在風險與挑戰

- 複雜的回收過程

- 原物料價格波動

- 市場機遇

- 為個人護理和化妝品包裝增值

- 生態標章和品牌差異化

- 促進要素

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 新興經營模式

- 合規要求

- 永續性措施

- 永續材料評估

- 碳足跡分析

- 採取循環經濟模式

- 永續性認證和標準

- 永續性投資報酬率分析

- 專利和智慧財產權分析

- 地緣政治和貿易趨勢

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 主要企業的競爭標竿分析

- 財務績效比較

- 收入

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線的廣度

- 科技

- 創新

- 區域比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導企業

- 受讓人

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年主要發展動態

- 併購

- 合作夥伴關係和合資企業

- 技術進步

- 擴張與投資策略

- 數位轉型計劃

- 新興/Start-Ups競賽的趨勢

第5章 按材料分類的市場估算與預測,2022-2035年

- 塑膠

- 鋁

- 聚箔

第6章 依產能分類的市場估計與預測,2022-2035年

- 少於50毫升

- 50ml~100ml

- 100ml~150ml

- 150ml~200ml

- 超過200毫升

第7章 按應用領域分類的市場估算與預測,2022-2035年

- 化妝品和個人護理

- 護膚

- 護髮

- 口腔護理

- 藥膏和乳霜

- 調味品和醬料

- 食用糊

- 黏合劑和密封劑

- 其他

第8章 依最終用途產業分類的市場估算與預測,2022-2035年

- 消費品

- 製藥

- 食品/飲料

- 工業的

- 其他

第9章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 主要企業

- Amcor Plc

- Albea Group

- EPL Limited

- Hoffmann Neopac AG

- 按地區分類的主要企業

- 北美洲

- CCL Industries Inc.

- Plastube Inc.

- Perfect Containers Group

- 歐洲

- Alltub Group

- Pirlo GmbH &Co. KG

- Tubapack AS

- 亞太地區

- Kyodo Printing(Vietnam)Co., Ltd.

- Antilla Propack

- BRK Packwell Private Limited.

- 北美洲

- 小眾玩家/顛覆者

- Burhani Packaging

- CTLpack

- Huhtamaki Oyj

- Montebello Packaging

- Norway Pack

- Perfektup Ambalaj

- Prutha Packaging Pvt. Ltd.

- REGO

- Shreeji Enterprises

- STS Pack Holding

- Zeal Life Sciences Pvt. Ltd.

The Global Laminated Tubes Market was valued at USD 1.8 billion in 2025 and is estimated to grow at a CAGR of 7.1% to reach USD 3.6 billion by 2035.

Market growth is supported by stricter regulatory standards and rising consumer awareness related to environmental responsibility. Companies are increasingly adopting sustainable packaging approaches, including recyclable and biodegradable materials, to align with circular economy objectives. Laminated tubes are designed to reduce material waste and improve recyclability, helping brands meet sustainability goals while responding to evolving consumer expectations. Demand is also rising due to the need for secure, high-barrier, and compliant packaging solutions, particularly for regulated products. Laminated tubes offer strong resistance to moisture, oxygen, and external contaminants while enabling controlled and accurate dispensing. As industries place greater emphasis on safety, shelf-life extension, and regulatory compliance, laminated tube packaging continues to gain traction. Ongoing material innovation and improved manufacturing techniques further strengthen the market's growth outlook across multiple end-use sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.8 Billion |

| Forecast Value | $3.6 Billion |

| CAGR | 7.1% |

The plastic segment is expected to reach USD 1.4 billion by 2035. Strong demand is supported by the material's lightweight nature, cost efficiency, flexibility, and excellent barrier performance. Continuous advancements in recyclable polymers and multilayer structures are increasing acceptance and expanding application scope.

The consumer goods segment accounted for 31.9% share in 2025. Growth is driven by demand for packaging solutions that combine durability, convenience, and visual appeal. Increased focus on user experience, shelf visibility, and brand differentiation continues to encourage innovation in tube structure, materials, and printing technologies.

North America Laminated Tubes Market held a 30% share in 2025. Regional demand is supported by strong adoption of premium and customized packaging solutions, emphasis on sustainability, and the presence of advanced packaging manufacturers and global brand owners, which together promote continuous product development.

Key companies operating in the Global Laminated Tubes Market include Amcor Plc, CCL Industries Inc., Albea Group, EPL Limited, Alltub Group, Pirlo GmbH & Co. KG, Tubapack A.S., Plastube Inc., STS Pack Holding, CTLpack, BRK Packwell Private Limited, Antilla Propack, Burhani Packaging, Shreeji Enterprises, Prutha Packaging Pvt. Ltd., REGO, and Zeal Life Sciences Pvt. Ltd. Companies in the Global Laminated Tubes Market strengthen their market position through material innovation, sustainable product development, and expanded manufacturing capabilities. Firms focus on developing recyclable and lightweight tube structures that meet regulatory and environmental standards. Investment in advanced barrier technologies helps improve product protection and shelf life. Strategic partnerships with brand owners support customized packaging solutions and long-term contracts.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Material trends

- 2.2.2 Capacity trends

- 2.2.3 Application trends

- 2.2.4 End use industry trends

- 2.2.5 Regional trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Shift toward sustainable and eco-friendly packaging

- 3.2.1.2 Growth in personal care and cosmetics industry

- 3.2.1.3 Advancements in tube printing technology

- 3.2.1.4 Rising demand for pharmaceutical packaging

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complex recycling process

- 3.2.2.2 Fluctuating raw material prices

- 3.2.3 Market opportunities

- 3.2.3.1 Premiumization of personal care and cosmetics packaging

- 3.2.3.2 Eco-labeling and brand differentiation

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter's analysis

- 3.5 PESTEL analysis

- 3.6 Technology and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Emerging business models

- 3.8 Compliance requirements

- 3.9 Sustainability measures

- 3.9.1 Sustainable materials assessment

- 3.9.2 Carbon footprint analysis

- 3.9.3 Circular economy implementation

- 3.9.4 Sustainability certifications and standards

- 3.9.5 Sustainability ROI analysis

- 3.10 Patent and IP analysis

- 3.11 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material, 2022 - 2035 ($ Mn & Mn Units)

- 5.1 Key trends

- 5.2 Plastic

- 5.3 Aluminum

- 5.4 Polyfoil

Chapter 6 Market Estimates and Forecast, By Capacity, 2022 - 2035 ($ Mn & Mn Units)

- 6.1 Key trends

- 6.2 Less than 50ml

- 6.3 50ml to 100ml

- 6.4 100ml to 150ml

- 6.5 150ml to 200ml

- 6.6 Above 200ml

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn & Mn Units)

- 7.1 Key trends

- 7.2 Cosmetics and personal care

- 7.2.1 Skin care

- 7.2.2 Hair care

- 7.2.3 Oral care

- 7.3 Ointments and creams

- 7.4 Condiments and sauces

- 7.5 Edible pastes

- 7.6 Adhesives and sealants

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By End Use industry, 2022 - 2035 ($ Mn & Mn Units)

- 8.1 Key trends

- 8.2 Consumer goods

- 8.3 Pharmaceuticals

- 8.4 Food and beverages

- 8.5 Industrial

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn & Mn Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Amcor Plc

- 10.1.2 Albea Group

- 10.1.3 EPL Limited

- 10.1.4 Hoffmann Neopac AG

- 10.2 Regional Key Players

- 10.2.1 North America

- 10.2.1.1 CCL Industries Inc.

- 10.2.1.2 Plastube Inc.

- 10.2.1.3 Perfect Containers Group

- 10.2.2 Europe

- 10.2.2.1 Alltub Group

- 10.2.2.2 Pirlo GmbH & Co. KG

- 10.2.2.3 Tubapack A.S.

- 10.2.3 APAC

- 10.2.3.1 Kyodo Printing (Vietnam) Co., Ltd.

- 10.2.3.2 Antilla Propack

- 10.2.3.3 BRK Packwell Private Limited.

- 10.2.1 North America

- 10.3 Niche Players / Disruptors

- 10.3.1 Burhani Packaging

- 10.3.2 CTLpack

- 10.3.3 Huhtamaki Oyj

- 10.3.4 Montebello Packaging

- 10.3.5 Norway Pack

- 10.3.6 Perfektup Ambalaj

- 10.3.7 Prutha Packaging Pvt. Ltd.

- 10.3.8 REGO

- 10.3.9 Shreeji Enterprises

- 10.3.10 STS Pack Holding

- 10.3.11 Zeal Life Sciences Pvt. Ltd.

膠印層壓包裝市場機會、成長要素、產業趨勢分析及 2026-2035 年預測。

膠印層壓包裝市場機會、成長要素、產業趨勢分析及 2026-2035 年預測。 包裝複合材料市場規模、佔有率、成長和行業分析:按材料(聚乙烯、聚丙烯、聚酯、鋁箔、紙張、其他)、應用和地區分類(至2034年)

包裝複合材料市場規模、佔有率、成長和行業分析:按材料(聚乙烯、聚丙烯、聚酯、鋁箔、紙張、其他)、應用和地區分類(至2034年) 鋁阻隔積層軟管市場(按應用、層數、管徑、裝飾和封閉類型)—2025-2032 年全球預測

鋁阻隔積層軟管市場(按應用、層數、管徑、裝飾和封閉類型)—2025-2032 年全球預測 全球積層軟管市場

全球積層軟管市場 全球包裝層壓板市場:市場規模、佔有率和趨勢分析(按材料、厚度、最終用途和地區),按細分市場預測(2025-2030 年)

全球包裝層壓板市場:市場規模、佔有率和趨勢分析(按材料、厚度、最終用途和地區),按細分市場預測(2025-2030 年) 2032 年積層軟管市場預測:按類型、瓶蓋類型、材料、印刷技術、產能、最終用戶、地區進行的全球分析

2032 年積層軟管市場預測:按類型、瓶蓋類型、材料、印刷技術、產能、最終用戶、地區進行的全球分析 全球鋁阻隔層壓管市場規模研究,按應用、產能、材料和區域預測 2022-2032 年

全球鋁阻隔層壓管市場規模研究,按應用、產能、材料和區域預測 2022-2032 年