|

市場調查報告書

商品編碼

1913293

IT資產處置市場機會、成長要素、產業趨勢分析及預測(2026-2035年)IT Asset Disposition (ITAD) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球 IT 資產處置 (ITAD) 市場預計到 2025 年將達到 175 億美元,到 2035 年將達到 401 億美元,年複合成長率為 8.9%。

全球電子廢棄物數量的不斷成長推動了這個市場的擴張,電子垃圾問題已成為企業和政府面臨的緊迫挑戰。過去,廢棄的IT設備往往最終被掩埋,造成嚴重的環境問題。如今,電信、金融、製造、媒體和政府等行業的機構越來越傾向於回收、翻新和轉售廢棄的IT資產。這種轉變為ITAD(資訊科技資產處置)服務提供者創造了巨大的機遇,幫助他們幫助企業實現永續性和淨零排放目標。隨著企業社會責任(CSR)日益受到重視,企業也逐漸意識到負責任地管理廢棄電子產品的重要性。透過採用經認證的ITAD流程,企業可以確保資料安全擦除、減少環境影響、滿足不斷變化的監管要求,同時也能從回收的資產中獲得潛在收益。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 175億美元 |

| 預測金額 | 401億美元 |

| 複合年成長率 | 8.9% |

到2025年,電腦和筆記型電腦市場將佔29.6%的佔有率,創造52億美元的收入。這些設備的平均使用壽命為3至8年,因此對ITAD服務有持續的需求。雲端運算的普及和資料中心的擴張進一步增加了需要安全處置、回收或翻新的設備數量。這一趨勢為擁有區域或本地營運的ITAD服務供應商帶來了強勁的成長前景。

到2025年,大型企業將佔據66.9%的市場佔有率,這主要得益於其在多個地點管理的龐大IT設備數量。人工智慧、雲端運算和其他新興技術推動的頻繁硬體更新換代,每年都會產生大量廢棄資產。大型企業依賴經過認證的ITAD服務來遵守GDPR、HIPAA和ESG標準等法規,降低資料外洩風險,並履行環境義務。

預計2025年,美國IT資產處分(ITAD)市場規模將達53億美元。推動市場成長的主要因素包括:大型企業對IT的高需求、頻繁的技術升級以及嚴格的法規環境。在政府推行企業社會責任(CSR)和永續性政策的支持下,企業正積極採用經認證的ITAD服務,以確保資料安全擦除和環保回收。

目錄

第1章調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 電子廢棄物產生量呈上升趨勢

- 安全資料抹除的需求日益成長

- 雲端採用率不斷提高和資料中心整合

- 回收和翻新的IT資產的需求日益成長

- 產業潛在風險與挑戰

- 全球公司複雜的逆向物流

- 發展中地區回收基礎建設有限

- 市場機遇

- 對永續回收解決方案的需求日益成長

- 在新興市場拓展ITAD服務

- 資料中心退役創造新機遇

- 擴大與原始設備製造商和雲端服務供應商的合作關係

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 美國的資料保護與電子廢棄物法規

- 加拿大個人資訊保護與電子文件法

- 歐洲

- 一般資料保護規則(GDPR)

- 歐盟廢棄電子電氣設備指令(WEEE)

- ISO/IEC 27001 和 EN 標準

- 亞太地區

- 中國個人資訊保護法(PIPL)

- 日本個人資訊保護法(APPI)

- 印度的《資訊科技法》、《資料保護規則》和《電子廢棄物(管理)規則》

- 拉丁美洲

- 巴西通用資料保護法(LGPD)

- 墨西哥個人資訊保護法(LFPDPPP)

- 中東和非洲

- 阿拉伯聯合大公國個人資料保護法及危險廢棄物及電子廢棄物管理條例

- 南非的《個人資訊保護法》(POPIA) 和當地電子廢棄物標準

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 透過服務

- 成本細分分析

- 永續性和環境影響

- 環境影響評估

- 社會影響力和社區服務

- 公司管治與企業社會責任

- 永續金融與投資趨勢

- 碳足跡考量

- 案例研究

- 未來前景與機遇

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 企業擴張計畫和資金籌措

第5章 依資產類型分類的市場估算與預測,2022-2035年

- 電腦/筆記型電腦

- 智慧型手機和平板電腦

- 周邊設備

- 貯存

- 伺服器

- 其他

第6章 依公司規模分類的市場估計與預測,2022-2035年

- 小型企業

- 主要企業

第7章 按服務分類的市場估計與預測,2022-2035年

- 資料清除

- 逆向物流

- 再行銷

- 恢復價值

- 拆卸和拆除處理

- 回收利用

- 物流管理

- 其他

第8章 依實施類型分類的市場估算與預測,2022-2035年

- 現場 ITAD 服務

- 異地/設施內ITAD

第9章 2022-2035年各通路市場估算與預測

- 直接銷售(OEM 直接面向客戶)

- 第三方ITAD提供者

第10章 2022-2035年各產業市場估計與預測

- BFSI

- 資訊科技/通訊

- 政府

- 能源與公共產業

- 衛生保健

- 媒體與娛樂

- 其他

第11章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 比荷盧經濟聯盟

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ANZ

- 新加坡

- 馬來西亞

- 印尼

- 越南

- 泰國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- 世界公司

- Iron Mountain

- Sims Lifecycle

- Dell

- HP

- IBM

- SK Tes

- Park Place Technologies

- Ingram Micro

- ERI

- Arrow Electronics

- Apto Solutions

- CompuCom Systems

- LifeSpan

- Blancco Technology

- EPC Global Solutions

- 本地公司

- Quantum Lifecycle Partners

- Securis

- Sage Sustainable Electronics

- Wisetek

- Vyta

- GreenTek

- DMD Systems Recovery

- Excess Logic

- Technimove

- 新興企業

- ITAMG

- Hummingbird International

- CloudBlue

- DataServ

- Dynamic Lifecycle Innovations

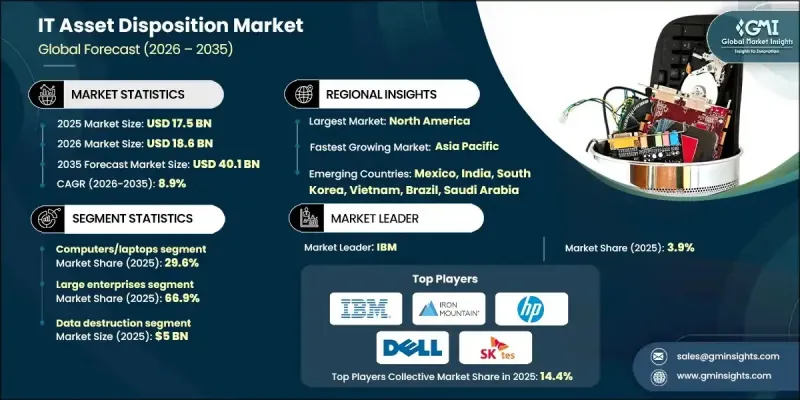

The Global IT Asset Disposition (ITAD) Market was valued at USD 17.5 billion in 2025 and is estimated to grow at a CAGR of 8.9% to reach USD 40.1 billion by 2035.

The expansion of this market is fueled by the rising volume of e-waste worldwide, which has become a pressing concern for businesses and governments alike. In the past, discarded IT equipment often ended up in landfills, creating significant environmental challenges. Today, organizations are increasingly turning to recycling, refurbishing, and reselling of retired IT assets across industries such as telecommunications, finance, manufacturing, media, and government. This shift has created a substantial opportunity for ITAD providers to support companies in achieving their sustainability and net-zero emission goals. Corporate social responsibility is emerging as a priority, with businesses recognizing the value of responsibly managing retired electronics. By adopting certified ITAD processes, companies can ensure secure data destruction, reduce environmental impact, and meet evolving regulatory requirements while generating potential revenue from recovered assets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $17.5 Billion |

| Forecast Value | $40.1 Billion |

| CAGR | 8.9% |

The computers and laptops segment held a 29.6% share in 2025, generating USD 5.2 billion. With an average lifespan of three to eight years, these assets create recurring demand for ITAD services. Growing cloud adoption and data center expansion further increase the volume of equipment requiring secure disposal, recycling, or refurbishment. This trend supports strong growth prospects for ITAD providers with local or regional operations.

The large enterprises segment held a 66.9% share in 2025, driven by the sheer volume of IT devices managed across multiple locations. Frequent hardware upgrades prompted by AI, cloud computing, and other emerging technologies result in significant volumes of retired assets annually. Large organizations rely on certified ITAD services to comply with regulations such as GDPR, HIPAA, and ESG standards, mitigate data breach risks, and meet environmental obligations.

U.S. IT Asset Disposition (ITAD) Market reached USD 5.3 billion in 2025. Growth is driven by the concentration of large companies with high IT demands, frequent technology upgrades, and a strong regulatory environment. Companies are adopting certified ITAD services for secure data destruction and environmentally responsible recycling, supported by government policies promoting corporate social responsibility and sustainability.

Leading players in the Global IT Asset Disposition (ITAD) Market include IBM, Dell, Iron Mountain, HP, SK Tes, Sims Lifecycle, LifeSpan, Park Place Technologies, Technimove, and Apto Solutions. Companies in the IT Asset Disposition (ITAD) Market strengthen their position through several strategic approaches. They invest in certified processes and secure data destruction services to build trust with large enterprises and comply with global regulations. Expanding geographic presence and establishing regional hubs ensure timely service delivery and support international clients. Firms also focus on technology-enabled tracking systems, reporting tools, and automated logistics to improve operational efficiency.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Asset

- 2.2.3 Enterprise Size

- 2.2.4 Services

- 2.2.5 Deployment

- 2.2.6 Channel

- 2.2.7 Industry Vertical

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising volume of e-waste generation

- 3.2.1.2 Increasing need for secure data destruction

- 3.2.1.3 Growth of cloud adoption and data center consolidation

- 3.2.1.4 Growing demand for value recovery & refurbished IT assets

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complex reverse logistics for global enterprises

- 3.2.2.2 Limited recycling infrastructure in developing regions

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for sustainable recycling solutions

- 3.2.3.2 Expansion of ITAD services in emerging markets

- 3.2.3.3 Rising opportunities in data center decommissioning

- 3.2.3.4 Increasing partnerships with OEMs & cloud providers

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. data protection and e-waste rules

- 3.4.1.2 Canadian Personal Information Protection and Electronic Documents Act

- 3.4.2 Europe

- 3.4.2.1 EU General Data Protection Regulation (GDPR)

- 3.4.2.2 EU Waste Electrical and Electronic Equipment (WEEE)

- 3.4.2.3 ISO/IEC 27001 and EN standards

- 3.4.3 Asia Pacific

- 3.4.3.1 China’s Personal Information Protection Law (PIPL)

- 3.4.3.2 Japan’s Act on the Protection of Personal Information (APPI)

- 3.4.3.3 India’s IT Act, data protection rules, and E-waste (Management) Rules

- 3.4.4 Latin America

- 3.4.4.1 Brazil’s General Data Protection Law (LGPD)

- 3.4.4.2 Mexico’s data protection law (LFPDPPP)

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE personal data protection law and hazardous/e-waste regulations

- 3.4.5.2 South Africa’s POPIA and local e-waste standards

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By service

- 3.9 Cost breakdown analysis

- 3.10 Sustainability and environmental impact

- 3.10.1 Environmental impact assessment

- 3.10.2 Social impact & community benefits

- 3.10.3 Governance & corporate responsibility

- 3.10.4 Sustainable finance & investment trends

- 3.10.5 Carbon footprint considerations

- 3.11 Case Studies

- 3.12 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Asset, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Computers/Laptops

- 5.3 Smartphones and Tablets

- 5.4 Peripherals

- 5.5 Storages

- 5.6 Servers

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Enterprise Size, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 SMEs

- 6.3 Large enterprises

Chapter 7 Market Estimates & Forecast, By Services, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Data Destruction

- 7.3 Reverse Logistics

- 7.4 Remarketing

- 7.5 Value Recovery

- 7.6 De-Manufacturing

- 7.7 Recycling

- 7.8 Logistics Management

- 7.9 Others

Chapter 8 Market Estimates & Forecast, By Deployment, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Onsite ITAD Services

- 8.3 Offsite / Facility-Based ITAD

Chapter 9 Market Estimates & Forecast, By Channel, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 Direct (OEM to Client)

- 9.3 Third-Party ITAD Providers

Chapter 10 Market Estimates & Forecast, By Industry Vertical, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 BFSI

- 10.3 IT & Telecom

- 10.4 Government

- 10.5 Energy and Utilities

- 10.6 Healthcare

- 10.7 Media and Entertainment

- 10.8 Others

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.3.8 Benelux

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Singapore

- 11.4.7 Malaysia

- 11.4.8 Indonesia

- 11.4.9 Vietnam

- 11.4.10 Thailand

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Colombia

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global companies

- 12.1.1 Iron Mountain

- 12.1.2 Sims Lifecycle

- 12.1.3 Dell

- 12.1.4 HP

- 12.1.5 IBM

- 12.1.6 SK Tes

- 12.1.7 Park Place Technologies

- 12.1.8 Ingram Micro

- 12.1.9 ERI

- 12.1.10 Arrow Electronics

- 12.1.11 Apto Solutions

- 12.1.12 CompuCom Systems

- 12.1.13 LifeSpan

- 12.1.14 Blancco Technology

- 12.1.15 EPC Global Solutions

- 12.2 Regional companies

- 12.2.1 Quantum Lifecycle Partners

- 12.2.2 Securis

- 12.2.3 Sage Sustainable Electronics

- 12.2.4 Wisetek

- 12.2.5 Vyta

- 12.2.6 GreenTek

- 12.2.7 DMD Systems Recovery

- 12.2.8 Excess Logic

- 12.2.9 Technimove

- 12.3 Emerging companies

- 12.3.1 ITAMG

- 12.3.2 Hummingbird International

- 12.3.3 CloudBlue

- 12.3.4 DataServ

- 12.3.5 Dynamic Lifecycle Innovations

IT資產處置市場:2026-2032年全球市場預測(按資產類型、服務類型、處置方法、處置地點、最終用戶產業、組織規模和採購管道分類)

IT資產處置市場:2026-2032年全球市場預測(按資產類型、服務類型、處置方法、處置地點、最終用戶產業、組織規模和採購管道分類) IT資產處置市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、流程、最終用戶及解決方案分類

IT資產處置市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、流程、最終用戶及解決方案分類 2026年全球企業IT資產處置市場報告IT資產處置(ITAD)全球市場報告(2026年)

2026年全球企業IT資產處置市場報告IT資產處置(ITAD)全球市場報告(2026年) 2026-2030年全球IT資產處分(ITAD)市場

2026-2030年全球IT資產處分(ITAD)市場 全球IT資產處置市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球IT資產處置市場規模、佔有率、趨勢和成長分析報告(2026-2034年) IT資產再利用市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、組織規模、垂直市場、地區及競爭格局分類,2021-2031年)IT資產處置市場-全球產業規模、佔有率、趨勢、機會、預測:按資產類型、最終用途、地區和競爭格局分類,2021-2031年IT資產遷移市場:2026-2032年全球預測(依資產類型、服務模式、公司規模及產業分類)

IT資產再利用市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、組織規模、垂直市場、地區及競爭格局分類,2021-2031年)IT資產處置市場-全球產業規模、佔有率、趨勢、機會、預測:按資產類型、最終用途、地區和競爭格局分類,2021-2031年IT資產遷移市場:2026-2032年全球預測(依資產類型、服務模式、公司規模及產業分類) 日本IT資產處置市場報告:依服務、資產類型、公司規模、產業及地區分類(2026-2034年)

日本IT資產處置市場報告:依服務、資產類型、公司規模、產業及地區分類(2026-2034年)