|

市場調查報告書

商品編碼

1913292

安全存取服務邊緣 (SASE) 市場機會、成長促進因素、產業趨勢分析與預測 (2026-2035)Secure Access Service Edge Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

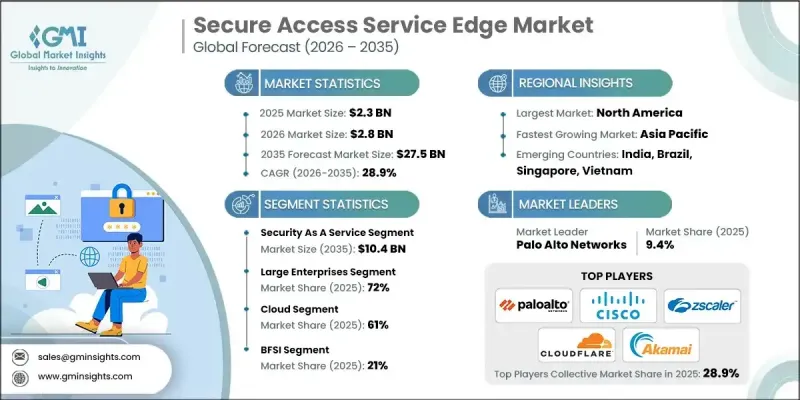

全球安全存取服務邊緣市場預計到 2025 年將達到 23 億美元,到 2035 年將達到 275 億美元,年複合成長率為 28.9%。

各行各業的組織都在加速向雲端交付應用程式轉型,重新定義企業網路和安全的設計方式。隨著對雲端託管軟體的依賴日益增強,企業正在摒棄傳統的基於邊界的防禦策略,轉而採用以雲端為中心的SASE架構,以提供統一的連接和安全性。企業越來越需要為使用者和設備提供一致的保護和最佳化的效能,無論其身處何地。這種需求正在推動集中管理、策略驅動的SASE平台的普及,這些平台在支援安全全球存取的同時,也能維持營運的柔軟性。分散式辦公、雲端遷移以及對可擴展基礎架構的需求正在重塑企業安全策略。為了支持不斷發展的業務運營和實現長期的數位轉型目標,各組織正在優先考慮簡化管理、加強基於身分的控制以及採用統一的網路和安全模型。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 23億美元 |

| 預測金額 | 275億美元 |

| 複合年成長率 | 28.9% |

分散的安全工具的廣泛使用增加了營運複雜性和成本,促使企業將網路和安全整合到一個統一的平台上。採用統一的SASE解決方案可以幫助企業實現IT環境現代化,減少供應商分散,並簡化管理。隨著零信任原則的興起,SASE框架內的統一身分和存取控制有助於限制未經授權的存取活動,並降低基於憑證的風險。

預計到2025年,安全即服務(Security as a Service)將佔據52%的市場佔有率,到2035年市場規模將達到104億美元。企業越來越依賴雲端原生保全服務來取代傳統模式,在強化防護的同時,也支援混合雲和雲端優先的營運模式。這些服務內建的高階分析和自動化功能提高了威脅偵測和回應的效率。

預計到2025年,大型企業將佔據72%的市場佔有率,到2035年將成長至183億美元。這些企業採用SASE是為了應對複雜的全球營運、嚴格的安全要求以及超過兩年的漫長引進週期。高可用性、擴充性、可自訂策略和強大的服務保障仍然是推動其採用的關鍵因素。

預計到2025年,美國安全存取服務邊緣市場規模將達到7.534億美元。美國企業正根據國家零信任計劃,快速對其安全框架進行現代化改造,以支援遠距辦公、雲端擴展和日益成長的網路風險。市場對能夠提升分散式團隊效能、可擴展性和使用者體驗的雲端原生平台的需求持續成長。

目錄

第1章調查方法

第2章執行摘要

第3章業界考察

- 產業生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 雲端運算和SaaS的快速普及

- 擴大遠距和混合辦公模式

- 網路安全威脅日益加劇,攻擊手段也日益複雜。

- 降低安全複雜性和供應商分散性的必要性

- 加速零信任安全框架

- 產業潛在風險與挑戰

- 與傳統基礎設施整合的挑戰

- 對資料隱私和供應商鎖定問題的擔憂

- 市場機遇

- 拓展至中小企業及中階市場領域

- 對人工智慧驅動的威脅偵測的需求日益成長

- 邊緣運算應用的日益普及

- 多重雲端和混合雲端現代化舉措

- 成長潛力分析

- 監管環境

- 北美洲

- 美國- 加州消費者隱私法案

- 加拿大—個人資訊保護與電子文件法

- 歐洲

- 英國- 資料保護法

- 德國——聯邦資料保護法

- 法國——數位共和國法案

- 義大利—個人資料保護法

- 西班牙—資料保護與數位權利組織法

- 亞太地區

- 中國 - 個人資訊保護法

- 日本—個人資訊保護法

- 印度—數位個人資料保護法

- 拉丁美洲

- 巴西——通用資料保護法

- 墨西哥—關於保護私人實體所持有個人資料的聯邦法律

- 阿根廷—個人資料保護法

- 中東和非洲

- 阿拉伯聯合大公國—個人資料保護法

- 南非—個人資訊保護法

- 沙烏地阿拉伯—個人資料保護法

- 北美洲

- 波特分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 成本細分分析

- 開發成本結構

- 研發成本分析

- 行銷和銷售費用

- 專利分析

- 案例研究

- 永續性和環境方面

- 永續努力

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 未來市場展望與機遇

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 企業擴張計畫和資金籌措

第5章 市場估算與預測:依產品類型分類(2021-2034 年)

- 網路即服務

- 安全即服務

第6章 市場估算與預測:依部署模式分類(2021-2034 年)

- 雲

- 本地部署

第7章 市場估計與預測:依公司規模分類(2021-2034 年)

- 主要企業

- 小型企業

第8章 依最終用途分類的市場估算與預測(2022-2035 年)

- BFSI

- 資訊科技/通訊

- 零售

- 衛生保健

- 政府

- 製造業

- 能源與公共產業

- 教育

- 其他

第9章 各地區市場估算與預測(2022-2035 年)

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 葡萄牙

- 克羅埃西亞

- 比荷盧經濟聯盟

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 新加坡

- 泰國

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

第10章:公司簡介

- 全球公司

- Cisco

- Palo Alto Networks

- Fortinet

- Zscaler

- Cloudflare

- Akamai

- Broadcom VMware

- Juniper Networks

- Aruba Networks HPE

- Verizon

- AT&T Cybersecurity

- Check Point Software Technologies

- IBM Security

- McAfee Enterprise Trellix

- BT Group British Telecom

- 本地公司

- SonicWall

- Forcepoint

- Barracuda Networks

- WatchGuard Technologies

- Sophos

- Sangfor Technologies

- Cyberoam

- SecPod

- T-Systems

- 新創公司/顛覆者

- Netskope

- Cato Networks

- Versa Networks

- Aryaka

- Perimeter 81

- Tailscale

- Axis Security

The Global Secure Access Service Edge Market was valued at USD 2.3 billion in 2025 and is estimated to grow at a CAGR of 28.9% to reach USD 27.5 billion by 2035.

Organizations across industries are accelerating the shift toward cloud-delivered applications, which is redefining how enterprise networks and security are designed. As reliance on cloud-hosted software grows, companies are moving away from legacy perimeter-based defenses and adopting cloud-centric SASE architectures that deliver unified connectivity and security. Enterprises increasingly require consistent protection and optimized performance for users and devices regardless of location. This demand is driving adoption of centrally managed, policy-driven SASE platforms that support secure global access while maintaining operational flexibility. Distributed workforces, cloud migration, and the need for scalable infrastructure are reshaping enterprise security strategies. Organizations are prioritizing simplified management, stronger identity-based controls, and integrated networking and security models to support evolving business operations and long-term digital transformation goals.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.3 Billion |

| Forecast Value | $27.5 Billion |

| CAGR | 28.9% |

The growing use of fragmented security tools has increased operational complexity and cost, prompting organizations to consolidate networking and security into integrated platforms. Unified SASE deployments allow enterprises to modernize IT environments, reduce vendor sprawl, and streamline management. As zero-trust principles gain traction, integrated identity verification and access control within SASE frameworks help limit unauthorized movement and reduce credential-based risks.

The security delivered as a service accounted for 52% share in 2025 and is forecast to reach USD 10.4 billion by 2035. Enterprises are increasingly relying on cloud-native security services to replace traditional models, improving protection while supporting hybrid and cloud-first operations. Advanced analytics and automation embedded within these services enhance threat detection and response efficiency.

The large enterprises represented held 72% share in 2025 and is projected to generate USD 18.3 billion by 2035. These organizations adopt SASE to address complex global operations, strict security requirements, and long deployment cycles that often extend beyond two years. High availability, scalability, customizable policies, and strong service guarantees remain key adoption drivers.

United States Secure Access Service Edge Market reached USD 753.4 million in 2025. U.S.-based organizations are rapidly modernizing security frameworks to support remote work, cloud expansion, and rising cyber risks, while aligning with national zero-trust initiatives. Demand continues to rise for cloud-native platforms that improve performance, scalability, and user experience for distributed teams.

Leading companies operating in the Global Secure Access Service Edge Market include Cisco, Zscaler, Fortinet, Palo Alto Networks, Akamai, Broadcom, Netskope, Cloudflare, and Forcepoint. Companies in the Global Secure Access Service Edge Market strengthen their market position by expanding cloud-native portfolios and emphasizing integrated security and networking capabilities. Providers focus on platform consolidation to reduce complexity for enterprise customers while improving visibility and control. Continuous investment in automation, analytics, and intelligent threat mitigation enhances operational efficiency and security outcomes. Strategic partnerships and ecosystem development enable broader service integration and faster deployment. Vendors also prioritize scalability, uptime assurance, and flexible pricing models to attract large enterprises and mid-sized organizations alike.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Offering

- 2.2.3 Deployment model

- 2.2.4 Organization size

- 2.2.5 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook & strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Rapid cloud and SaaS adoption

- 3.2.1.3 Expansion of remote and hybrid workforces

- 3.2.1.4 Rising cybersecurity threats and attack sophistication

- 3.2.1.5 Need to reduce security complexity and vendor sprawl

- 3.2.1.6 Acceleration of zero-trust security frameworks

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Integration challenges with legacy infrastructure

- 3.2.2.2 Concerns over data privacy and vendor lock-in

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into SMB and mid-market segments

- 3.2.3.2 Growing demand for AI-driven threat detection

- 3.2.3.3 Increasing adoption of edge computing applications

- 3.2.3.4 Multi-cloud and hybrid-cloud modernization initiatives

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. - California Consumer Privacy Act

- 3.4.1.2 Canada - Personal Information Protection and Electronic Documents Act

- 3.4.2 Europe

- 3.4.2.1 UK - Data Protection Act

- 3.4.2.2 Germany - Federal Data Protection Act

- 3.4.2.3 France - Digital Republic Act

- 3.4.2.4 Italy - Personal Data Protection Code

- 3.4.2.5 Spain - Organic Law on Data Protection and Digital Rights

- 3.4.3 Asia Pacific

- 3.4.3.1 China - Personal Information Protection Law

- 3.4.3.2 Japan - Act on the Protection of Personal Information

- 3.4.3.3 India - Digital Personal Data Protection Act

- 3.4.4 Latin America

- 3.4.4.1 Brazil - General Data Protection Law

- 3.4.4.2 Mexico - Federal Law on Protection of Personal Data Held by Private Parties

- 3.4.4.3 Argentina - Personal Data Protection Law

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE - Personal Data Protection Law

- 3.4.5.2 South Africa - Protection of Personal Information Act

- 3.4.5.3 Saudi Arabia - Personal Data Protection Law

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.8.1 Development cost structure

- 3.8.2 R&D cost analysis

- 3.8.3 Marketing & sales costs

- 3.9 Patent analysis

- 3.10 Case study

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.12 Future market outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Offering, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Network as a Service

- 5.3 Security as a Service

Chapter 6 Market Estimates & Forecast, By Deployment model, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Cloud

- 6.3 On-premises

Chapter 7 Market Estimates & Forecast, By Organization size, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Large Enterprises

- 7.3 SMEs

Chapter 8 Market Estimates & Forecast, By End Use, 2022-2035 (USD Mn)

- 8.1 Key trends

- 8.2 BFSI

- 8.3 IT & Telecom

- 8.4 Retail

- 8.5 Healthcare

- 8.6 Government

- 8.7 Manufacturing

- 8.8 Energy & utilities

- 8.9 Education

- 8.10 Others

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.3.8 Portugal

- 9.3.9 Croatia

- 9.3.10 Benelux

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Singapore

- 9.4.7 Thailand

- 9.4.8 Indonesia

- 9.4.9 Vietnam

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Colombia

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Turkey

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Cisco

- 10.1.2 Palo Alto Networks

- 10.1.3 Fortinet

- 10.1.4 Zscaler

- 10.1.5 Cloudflare

- 10.1.6 Akamai

- 10.1.7 Broadcom VMware

- 10.1.8 Juniper Networks

- 10.1.9 Aruba Networks HPE

- 10.1.10 Verizon

- 10.1.11 AT&T Cybersecurity

- 10.1.12 Check Point Software Technologies

- 10.1.13 IBM Security

- 10.1.14 McAfee Enterprise Trellix

- 10.1.15 BT Group British Telecom

- 10.2 Regional Players

- 10.2.1 SonicWall

- 10.2.2 Forcepoint

- 10.2.3 Barracuda Networks

- 10.2.4 WatchGuard Technologies

- 10.2.5 Sophos

- 10.2.6 Sangfor Technologies

- 10.2.7 Cyberoam

- 10.2.8 SecPod

- 10.2.9 T-Systems

- 10.3 Emerging / Disruptor Players

- 10.3.1 Netskope

- 10.3.2 Cato Networks

- 10.3.3 Versa Networks

- 10.3.4 Aryaka

- 10.3.5 Perimeter 81

- 10.3.6 Tailscale

- 10.3.7 Axis Security

安全存取服務邊緣市場-2026-2032年全球市場預測

安全存取服務邊緣市場-2026-2032年全球市場預測 SASE市場預測——按組件、部署模式、架構類型、應用、最終用戶和地區分類的全球分析——2034年

SASE市場預測——按組件、部署模式、架構類型、應用、最終用戶和地區分類的全球分析——2034年 SD-WAN 與 SASE:全球市場預測(2025-2030 年)

SD-WAN 與 SASE:全球市場預測(2025-2030 年) 安全存取服務邊緣 (SASE) 市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶和解決方案分類

安全存取服務邊緣 (SASE) 市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶和解決方案分類 2026 年全球服務邊際市場報告

2026 年全球服務邊際市場報告 安全存取服務邊緣 (SASE) 市場:按解決方案和區域分類

安全存取服務邊緣 (SASE) 市場:按解決方案和區域分類 安全存取服務邊際市場 - 全球產業規模、佔有率、趨勢、機會、預測:按組件、最終用途、組織規模、地區和競爭對手分類,2021-2031 年

安全存取服務邊際市場 - 全球產業規模、佔有率、趨勢、機會、預測:按組件、最終用途、組織規模、地區和競爭對手分類,2021-2031 年 2026-2030年全球安全存取服務邊緣市場

2026-2030年全球安全存取服務邊緣市場 安全存取服務邊緣 (SASE) 市場規模、佔有率和成長分析(按產品、服務標準、組織規模、最終用戶和地區分類)—2026-2033 年行業預測安全存取服務邊緣 (SASE) 市場按產品、性別、組織規模、部署模式和最終用戶行業分類 - 2025-2030 年全球預測

安全存取服務邊緣 (SASE) 市場規模、佔有率和成長分析(按產品、服務標準、組織規模、最終用戶和地區分類)—2026-2033 年行業預測安全存取服務邊緣 (SASE) 市場按產品、性別、組織規模、部署模式和最終用戶行業分類 - 2025-2030 年全球預測