|

市場調查報告書

商品編碼

1913283

壓電微型幫浦市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)Piezoelectric Micro Pump Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

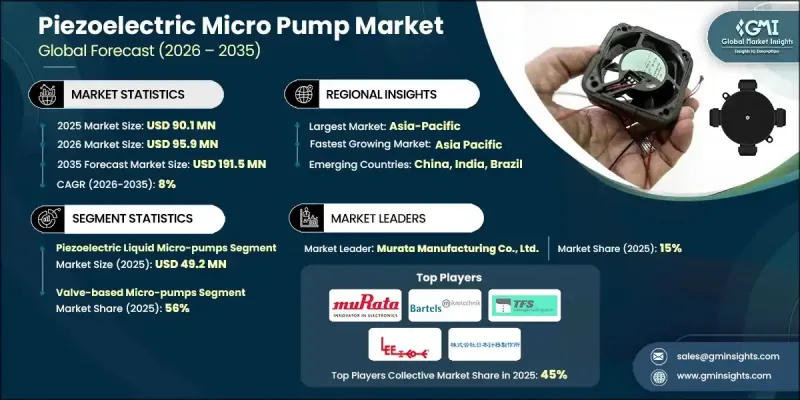

全球壓電微型幫浦市場預計到 2025 年將達到 9,010 萬美元,到 2035 年將達到 1.915 億美元,年複合成長率為 8%。

隨著越來越多的行業尋求緊湊、高精度且節能的流體和氣體處理解決方案,該市場正穩步發展。壓電微泵利用壓電致動器運行,正在革新對精度、空間利用率和低功耗要求極高的應用領域的流體控制。其運作安靜、發熱量低,且無需複雜的機械組裝即可提供穩定的流速,這些優勢推動了各行各業的強勁需求。隨著製造商不斷追求更小巧、更智慧的系統設計,對可靠、長壽命且運行穩定的微流體組件的需求日益成長。加速的技術創新使這些泵浦成為優先考慮便攜性、精度和運作效率的先進系統結構的重要組成部分。致動器材料和泵浦結構的持續改進進一步提升了性能、耐用性和整合柔軟性,從而支撐了市場的持續成長。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 9010萬美元 |

| 預測金額 | 1.915億美元 |

| 複合年成長率 | 8% |

壓電微泵技術的應用範圍正從傳統領域擴展到需要極高精度劑量控制和流體傳輸的領域。緊湊型分析系統、溫度控管。

預計2025年,壓電液體微型幫浦市場規模將達4,920萬美元。這類泵浦因其能夠在保持緊湊面積的同時精確輸送液體而得到廣泛應用。其致動器驅動設計最大限度地減少了運動部件,提高了可靠性,使其能夠應用於需要精確穩定流體輸送的精密系統中。

到2025年,閥式微型幫浦將佔56.4%的市場。其高普及率歸功於其增強的流量調節能力,例如透過整合閥門機構實現方向控制和降低迴流風險。這種設計優勢使其適用於需要高精度操作控制和重複性的應用。

預計到 2025 年,美國壓電微型幫浦市場將佔據 75% 的市場佔有率,達到 2,030 萬美元。該地區受益於微流體技術的早期應用、對研發的大力投入以及完善的商業化途徑,尤其是在技術先進的行業。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 產業影響因素

- 促進要素

- 對小型化醫療設備的需求日益成長

- 微流體和實驗室自動化領域的進展

- 整合到家用電子電器和冷卻系統中

- 產業潛在風險與挑戰

- 製造流程複雜且成本高

- 惡劣環境下的可靠性挑戰

- 機會

- 照護現場的擴展

- 穿戴式裝置和物聯網裝置中的應用

- 促進要素

- 成長潛力分析

- 關鍵市場趨勢與顛覆性因素

- 未來市場趨勢

- 風險及緩解分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按模型

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 按車型分類的市場估計與預測,2022-2035年

- 壓電液體微型泵

- 壓電空氣/氣體微型泵

6. 按設計類型分類的市場估算與預測,2022-2035 年

- 無閥微型泵

- 閥式微型泵

7. 2022-2035年按最終用途產業分類的市場估算與預測

- 醫學與生命科學

- 家用電子電器

- 工業應用

- 汽車/運輸設備

- 家用電器

- 其他(航太與國防、農業)

第8章 按分銷管道分類的市場估算與預測,2022-2035年

- 直銷

- 間接銷售

第9章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 土耳其

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Murata Manufacturing Co., Ltd.

- Bartels Mikrotechnik GmbH

- Takasago Electric, Inc

- The Lee Company

- Nippon Keiki Works, Ltd.

- NITTO KOHKI CO., LTD.

- MicroJet Technology Co., Ltd.

- Audiowell Electronics(Guangdong)Co., Ltd.

- HeYi Precision Pump

- Maxclever Electric Co., Ltd.

- Dolomite Microfluidics

- Koge Micro Tech Co., Ltd.

- Debiotech SA

- PiezoData Inc.

- HOERBIGER Motion Control GmbH

The Global Piezoelectric Micro Pump Market was valued at USD 90.1 million in 2025 and is estimated to grow at a CAGR of 8% to reach USD 191.5 million by 2035.

The market is steadily gaining momentum as industries increasingly seek compact, highly accurate, and energy-efficient solutions for fluid and gas handling. Piezoelectric micro pumps, which operate using piezoelectric actuators, are reshaping fluid control in applications where precision, space efficiency, and low power usage are critical. Their quiet performance, minimal heat generation, and ability to deliver stable flow rates without complex mechanical assemblies make them particularly attractive across a wide range of sectors. Demand is rising as manufacturers focus on smaller, smarter system designs that require reliable microfluidic components capable of consistent operation over long lifecycles. As innovation accelerates, these pumps are becoming integral to advanced system architectures that emphasize portability, accuracy, and operational efficiency. Continuous advancements in actuator materials and pump structures are further enhancing performance, durability, and integration flexibility, supporting sustained market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $90.1 Million |

| Forecast Value | $191.5 Million |

| CAGR | 8% |

The use of piezoelectric micro pump technology is expanding beyond traditional applications into areas that require extremely controlled dosing and fluid transfer. Growing emphasis on compact analytical systems, thermal management solutions for electronics, and next-generation wearable platforms is contributing to broader adoption. Industries that rely on repeatable and contamination-free fluid handling are increasingly integrating these pumps into their designs, supported by ongoing improvements in manufacturing precision and system compatibility.

In 2025, the piezoelectric liquid micro pumps segment generated USD 49.2 million. These pumps are widely adopted due to their ability to deliver accurate liquid volumes while maintaining a compact footprint. Their actuator-driven design minimizes moving components, which enhances reliability and supports use in highly sensitive systems that require precise and consistent fluid delivery.

The valve-based micro pumps represented 56.4% share in 2025. Their strong adoption is linked to their enhanced flow regulation capabilities, as integrated valve mechanisms allow controlled directionality and reduce the risk of reverse flow. This design advantage makes them suitable for applications that demand higher levels of operational control and repeatability.

U.S Piezoelectric Micro Pump Market held 75% share, generating USD 20.3 million in 2025. The region benefits from early adoption of microfluidic technologies, strong investment in research and development, and established commercialization pathways, particularly across technologically advanced industries.

Key companies operating in the Global Piezoelectric Micro Pump Market include Murata Manufacturing Co., Ltd., Bartels Mikrotechnik GmbH, Dolomite Microfluidics, Takasago Electric, Inc., The Lee Company, NITTO KOHKI CO., LTD., Nippon Keiki Works, Ltd., Audiowell Electronics (Guangdong) Co., Ltd., MicroJet Technology Co., Ltd., HOERBIGER Motion Control GmbH, Debiotech SA, Koge Micro Tech Co., Ltd., Maxclever Electric Co., Ltd., HeYi Precision Pump, and PiezoData Inc. Companies in the Global Piezoelectric Micro Pump Market are strengthening their competitive position by prioritizing product miniaturization, performance optimization, and long-term reliability. Many players are investing in advanced piezoelectric materials and refined actuator designs to improve flow accuracy and energy efficiency. Strategic collaborations with system integrators and OEMs help accelerate adoption across specialized applications.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 By regional

- 2.2.2 By machine type

- 2.2.3 By design type

- 2.2.4 By end use industry

- 2.2.5 By distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Demand for Miniaturized Medical Devices

- 3.2.1.2 Advancements in Microfluidics and Lab Automation

- 3.2.1.3 Integration in Consumer Electronics and Cooling Systems

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High Manufacturing Complexity and Cost

- 3.2.2.2 Reliability Issues in Harsh Environments

- 3.2.3 Opportunities

- 3.2.3.1 Expansion in Point-of-Care Diagnostics

- 3.2.3.2 Adoption in Wearable and IoT Devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Major market trends and disruptions

- 3.5 Future market trends

- 3.6 Risk and mitigation Analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By Machine type

- 3.9 Regulatory landscape

- 3.9.1 North America

- 3.9.2 Europe

- 3.9.3 Asia-Pacific

- 3.9.4 Middle East and Africa

- 3.9.5 Latin America

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Machine Type, 2022-2035 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Piezoelectric liquid micro-pumps

- 5.3 Piezoelectric air/gas micro-pumps

Chapter 6 Market Estimates & Forecast, By Design Type, 2022-2035 (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Valveless micro-pumps

- 6.3 Valve-based micro-pumps

Chapter 7 Market Estimates & Forecast, By End Use Industry, 2022-2035 (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Medical & life sciences

- 7.3 Consumer electronics

- 7.4 Industrial applications

- 7.5 Automotive & transportation

- 7.6 Household appliances

- 7.7 Others (aerospace & defense, agriculture)

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Turkey

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Murata Manufacturing Co., Ltd.

- 10.2 Bartels Mikrotechnik GmbH

- 10.3 Takasago Electric, Inc

- 10.4 The Lee Company

- 10.5 Nippon Keiki Works, Ltd.

- 10.6 NITTO KOHKI CO., LTD.

- 10.7 MicroJet Technology Co., Ltd.

- 10.8 Audiowell Electronics (Guangdong) Co., Ltd.

- 10.9 HeYi Precision Pump

- 10.10 Maxclever Electric Co., Ltd.

- 10.11 Dolomite Microfluidics

- 10.12 Koge Micro Tech Co., Ltd.

- 10.13 Debiotech SA

- 10.14 PiezoData Inc.

- 10.15 HOERBIGER Motion Control GmbH

先進壓電裝置市場分析及預測(至2035年):按類型、產品類型、技術、應用、材料類型、最終用戶、功能、安裝類型、裝置、解決方案分類

先進壓電裝置市場分析及預測(至2035年):按類型、產品類型、技術、應用、材料類型、最終用戶、功能、安裝類型、裝置、解決方案分類 全球壓電材料市場規模、佔有率、趨勢和成長分析報告(2026-2034年)壓電陶瓷市場-2026-2031年預測

全球壓電材料市場規模、佔有率、趨勢和成長分析報告(2026-2034年)壓電陶瓷市場-2026-2031年預測 壓電材料市場規模、佔有率及成長分析(依產品、材料、元件、工作模式、應用及地區分類)-2026-2033年產業預測

壓電材料市場規模、佔有率及成長分析(依產品、材料、元件、工作模式、應用及地區分類)-2026-2033年產業預測 KNN無鉛壓電陶瓷:全球市佔率及排名、總收入及需求預測(2025-2031年)壓電微型幫浦:全球市場佔有率和排名、總收入和需求預測(2025-2031年)壓電陶瓷技術:全球市佔率及排名、總收入及需求預測(2025-2031年)

KNN無鉛壓電陶瓷:全球市佔率及排名、總收入及需求預測(2025-2031年)壓電微型幫浦:全球市場佔有率和排名、總收入和需求預測(2025-2031年)壓電陶瓷技術:全球市佔率及排名、總收入及需求預測(2025-2031年) 壓電材料的全球市場 (~2035年):材料·用途·終端用戶·各地區壓電材料市場分析及至2034年的預測:依類型、產品、應用、材料類型、技術、組件、設備、最終用戶及功能全球壓電材料市場:2025 年至 2030 年預測

壓電材料的全球市場 (~2035年):材料·用途·終端用戶·各地區壓電材料市場分析及至2034年的預測:依類型、產品、應用、材料類型、技術、組件、設備、最終用戶及功能全球壓電材料市場:2025 年至 2030 年預測