|

市場調查報告書

商品編碼

1892908

稀有糖市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Rare Sugar Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

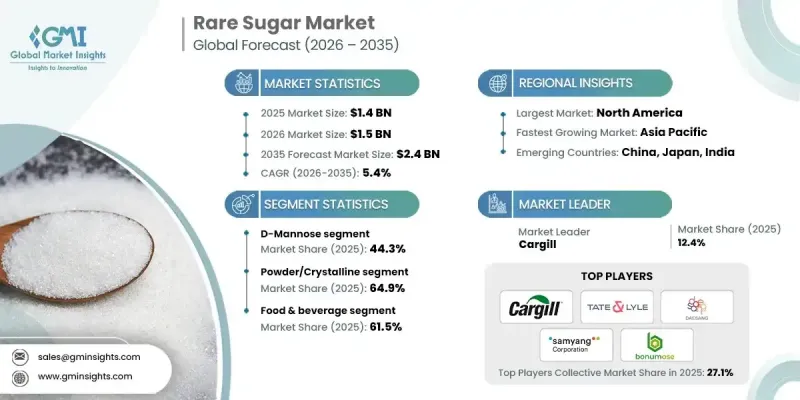

2025 年全球稀有糖市場價值為 14 億美元,預計到 2035 年將以 5.4% 的複合年成長率成長至 24 億美元。

低熱量、低升糖指數和清潔標籤的糖替代品(包括阿洛酮糖、塔格糖、D-甘露糖和阿洛糖)日益普及,推動了市場成長。人們對稀有糖代謝健康益處的認知不斷提高,加上監管框架的完善和供應鏈基礎設施的健全,正推動食品和飲料產品中稀有糖的應用。亞太地區成長最快,其中中國、日本和印度引領成長,這得益於可支配收入的增加、城市化進程的加快以及對健康食品需求的不斷成長。拉丁美洲和中東及非洲的新興市場,特別是巴西和沙烏地阿拉伯,也展現出良好的成長前景。整體而言,稀有糖正逐漸成為主流配料,各大品牌正在調整產品配方,以滿足消費者對更健康、清潔標籤替代品的需求,同時保持產品的口感和功能性。

| 市場範圍 | |

|---|---|

| 起始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 14億美元 |

| 預測值 | 24億美元 |

| 複合年成長率 | 5.4% |

食品飲料產業佔據了 61.5% 的市場佔有率,預計到 2035 年將以 4.8% 的複合年成長率成長。對低熱量和低升糖指數甜味劑的需求正在推動烘焙、糖果、飲料和乳製品行業的採用,這些甜味劑在不影響口味、質地或性能的前提下替代了傳統的糖。

2025年,粉末/結晶稀有糖市佔率為64.9%,預計從2025年到2034年將以4.4%的複合年成長率成長。與液體或糖漿形式的替代品相比,粉末和結晶形式具有更高的穩定性和更長的保存期限,使其成為大多數食品和飲料應用的理想選擇。

預計到2025年,北美稀有糖市場規模將達到4.617億美元。該地區的成長得益於消費者對低熱量、低升糖指數食品、清潔標籤產品的強勁需求,以及健康意識的提高、糖尿病盛行率的上升和功能性食品飲料的普及。此外,阿洛酮糖和塔格糖等稀有糖獲得監管部門批准,也進一步推動了美國市場的擴張。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 全球對更健康、低熱量甜味劑取代傳統糖的需求不斷成長

- 糖尿病和肥胖症盛行率的上升推動了功能性糖的創新

- 產業陷阱與挑戰

- 生產成本高昂,且大規模生產能力有限。

- 新興稀有糖的監管不確定性和全球批准差異

- 市場機遇

- 全球消費市場中清潔標籤和天然成分趨勢的不斷擴大

- 酵素法和微生物法生產技術的進步提高了糖合成的成本效益

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依稀有糖類型

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依稀有糖類型分類,2022-2035年

- D-甘露糖

- 阿洛酮糖

- 塔格糖

- 阿洛斯

第6章:市場估算與預測:依產品類型分類,2022-2035年

- 粉末/晶體

- 液體/糖漿

- 其他產品類型

第7章:市場估計與預測:依應用領域分類,2022-2035年

- 餐飲

- 製藥

- 化妝品

- 營養保健品

- 其他應用

第8章:市場估算與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- Anderson Global Group, LLC

- Ardilla Technologies

- Bonumose

- Cargill

- Daesang Corporation

- Matsutani Chemical Industry Co., Ltd

- Roquette Freres

- Samyang Corporation

- SAVANNA Ingredients GmbH

- Shandong Bailong Chuangyuan Bio-tech Co., Ltd

- Shandong Fuyang Bio-tech Co., Ltd

- Tate & Lyle PLC

The Global Rare Sugar Market was valued at USD 1.4 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 2.4 billion by 2035.

The market growth is fueled by the rising popularity of low-calorie, low-glycemic, and clean-label sugar alternatives, including allulose, tagatose, D-mannose, and allose. Increasing awareness of the metabolic health benefits of rare sugars, coupled with strengthened regulatory frameworks and robust supply chain infrastructures, is driving adoption in food and beverage products. The APAC region is witnessing the fastest growth, with China, Japan, and India leading due to rising disposable incomes, urbanization, and the growing demand for healthy foods. Emerging markets in Latin America and the Middle East & Africa, particularly Brazil and Saudi Arabia, are also showing promising growth prospects. Overall, rare sugars are becoming mainstream ingredients, with brands reformulating products to meet consumer demand for healthier, clean-label alternatives while maintaining taste and functionality.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.4 Billion |

| CAGR | 5.4% |

The food & beverage segment held a share of 61.5% share and is projected to grow at a CAGR of 4.8% through 2035. Demand for low-calorie and low-glycemic sweeteners is driving adoption across bakery, confectionery, beverage, and dairy products, replacing conventional sugars without compromising taste, texture, or performance.

The powder/crystalline rare sugars segment held 64.9% share in 2025 and is expected to grow at a CAGR of 4.4% from 2025 to 2034. Powder and crystalline forms offer greater stability and longer shelf-life compared to liquid or syrup alternatives, making them ideal for most food and beverage applications.

North America Rare Sugar Market generated USD 461.7 million in 2025. Growth in the region is supported by strong demand for low-calorie and low-glycemic foods, clean-label products, rising health awareness, increasing diabetes prevalence, and the popularity of functional foods and beverages. Regulatory approvals for rare sugars such as allulose and tagatose are further boosting market expansion in the U.S.

Key players operating in the Global Rare Sugar Market include Cargill, Daesang Corporation, Matsutani Chemical Industry Co., Ltd., Roquette Freres, Anderson Global Group, LLC, Ardilla Technologies, Bonumose, Samyang Corporation, SAVANNA Ingredients GmbH, Shandong Bailong Chuangyuan Bio-tech Co., Ltd., Shandong Fuyang Bio-tech Co., Ltd., and Tate & Lyle PLC. Companies in the Global Rare Sugar Market are strengthening their market position by investing heavily in research and development to innovate new sugar alternatives with better taste, stability, and functional benefits. Strategic partnerships with food and beverage manufacturers help expand distribution and accelerate adoption. Firms are also focusing on scaling production capabilities, securing reliable raw material sources, and obtaining regulatory approvals in multiple regions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Rare sugar type

- 2.2.3 Product type

- 2.2.4 Application

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global demand for healthier low-calorie sweeteners replacing conventional sugars

- 3.2.1.2 Increasing prevalence of diabetes and obesity driving functional sugar innovation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs and limited large-scale manufacturing capabilities

- 3.2.2.2 Regulatory uncertainties and varying global approvals for emerging rare sugars

- 3.2.3 Market opportunities

- 3.2.3.1 Expanding clean-label and natural ingredient trends across global consumer markets

- 3.2.3.2 Advances in enzymatic and microbial production improving cost-efficient sugar synthesis

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By rare sugar type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Rare Sugar Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 D-Mannose

- 5.3 Allulose

- 5.4 Tagatose

- 5.5 Allose

Chapter 6 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Powder/Crystalline

- 6.3 Liquid/Syrup

- 6.4 Other Product Types

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food and beverage

- 7.3 Pharmaceuticals

- 7.4 Cosmetics

- 7.5 Nutraceuticals

- 7.6 Other applications

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Anderson Global Group, LLC

- 9.2 Ardilla Technologies

- 9.3 Bonumose

- 9.4 Cargill

- 9.5 Daesang Corporation

- 9.6 Matsutani Chemical Industry Co., Ltd

- 9.7 Roquette Freres

- 9.8 Samyang Corporation

- 9.9 SAVANNA Ingredients GmbH

- 9.10 Shandong Bailong Chuangyuan Bio-tech Co., Ltd

- 9.11 Shandong Fuyang Bio-tech Co., Ltd

- 9.12 Tate & Lyle PLC