|

市場調查報告書

商品編碼

1892907

低溫設備市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Cryogenic Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

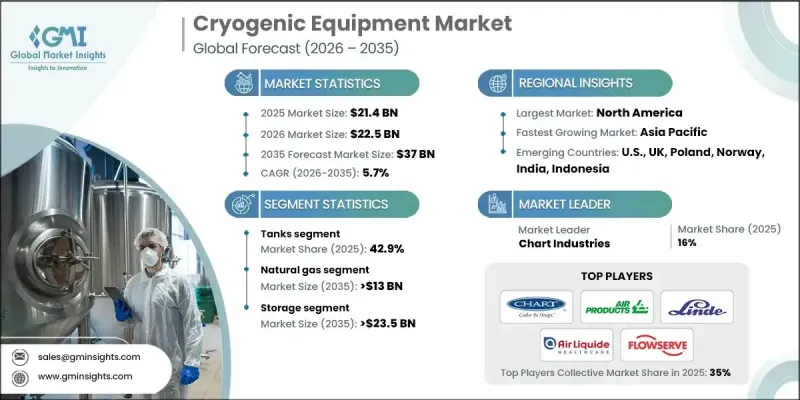

2025年全球低溫設備市場價值為214億美元,預計2035年將以5.7%的複合年成長率成長至370億美元。

市場成長主要得益於先進液化系統在天然氣儲存領域的日益普及,以及最佳化低溫運行的自動化閥門組件的持續整合。液化天然氣加註用低溫泵的廣泛應用,以及海事領域減排措施的推進,正在重塑設計重點。低溫設備涵蓋用於在極低溫下生產、處理、儲存和運輸物料的專用設備和系統,這些設備對於液化氮氣、氧氣、氫氣、氦氣和天然氣等氣體至關重要。真空絕緣管道、模組化低溫儲罐和撬裝式系統日益普及的提高了效率和靈活性,而物聯網感測器和預測性維護工具則提升了運作可靠性。工業和石化應用中低溫汽化器、壓縮機和靈活容量解決方案的日益普及,正在重新定義安裝規範,並為超低溫運行領域的創新創造機會。

| 市場範圍 | |

|---|---|

| 起始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 214億美元 |

| 預測值 | 370億美元 |

| 複合年成長率 | 5.7% |

預計到2035年,閥門市場規模將達到40億美元,主要得益於市場對不銹鋼和鎳合金的偏好以及對嚴格性能標準的堅持。專注於零排放運作的先進閥門設計符合永續發展目標,能夠更安全、更有效率地處理低溫流體。

預計到2035年,氧氣市場將以5.5%的複合年成長率成長。氧氣汽化器和大容量儲氧系統的日益普及正在推動包括航太燃料供應在內的工業流程。低溫氧氣泵的整合進一步促進了對精確可靠的低溫管理有更高要求的特定應用領域的發展。

美國低溫設備市場佔85.7%的市場佔有率,預計2025年市場規模將達42億美元。低溫儲槽的廣泛應用,以及削峰設施的配套設施,有助於應對季節性電力需求。物聯網賦能的低溫泵和預測性維護解決方案的日益普及,正在推動工廠的智慧化和自動化營運,從而提升整個產業的效率和安全性。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 原物料供應及採購分析

- 製造能力評估

- 供應鏈韌性與風險因素

- 配電網路分析

- 監管環境

- 產業影響因素

- 成長促進因素

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL 分析

- 低溫設備成本結構分析

- 新興機會與趨勢

- 數位化和物聯網整合

- 投資分析及未來展望

第4章:競爭格局

- 介紹

- 按地區分類的公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 戰略儀錶板

- Key partnerships & collaborations

- Major M&A activities

- Product innovations & launches

- Market expansion strategies

- 策略舉措

- 競爭性標竿分析

- 創新與技術格局

第5章:市場規模及預測:依產品分類,2022-2035年

- 坦克

- 閥門

- 霧化器

- 水泵浦

- 管道

- 其他

第6章:市場規模及預測:依低溫液體類型分類,2022-2035年

- 氮

- 氧

- 天然氣

- 氬氣

- 其他低溫液體

第7章:市場規模及預測:依應用領域分類,2022-2035年

- 貯存

- 分配

第8章:市場規模及預測:依最終用途分類,2022-2035年

- 石油天然氣產業

- 力量

- 餐飲

- 化學

- 橡膠和塑膠

- 冶金

- 衛生保健

- 船運

- 農業、林業和漁業

- 其他行業

第9章:市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 義大利

- 西班牙

- 法國

- 波蘭

- 挪威

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 印尼

- 泰國

- 馬來西亞

- 菲律賓

- 韓國

- 澳洲

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 科威特

- 阿曼

- 土耳其

- 卡達

- 埃及

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

- 秘魯

第10章:公司簡介

- Abhijit Enterprises

- Air Liquide

- Air Products and Chemicals

- AIR WATER

- Auguste Cryogenics

- BRUGG Pipes

- Chart Industries

- Cryogas Equipment

- Cryogenic OGS

- CRYOSPAIN

- Cryostar

- Cryoworld

- Demaco

- Emerson Electric

- Flowserve Corporation

- Hypro

- INOXCVA

- IWI Cryogenic Vaporization Systems (India) Pvt. Ltd.

- Kelvin International

- Linde

- Shell-n-Tube

- SLB

- Vacuum Barrier

The Global Cryogenic Equipment Market was valued at USD 21.4 billion in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 37 billion by 2035.

Market growth is driven by the increasing adoption of advanced liquefaction systems for natural gas storage and the rising integration of automated valve assemblies that optimize low-temperature operations. The growing deployment of cryogenic pumps for LNG bunkering, coupled with emission reduction initiatives across the marine sector, is shaping design priorities. Cryogenic equipment encompasses specialized devices and systems for producing, handling, storing, and transporting materials at extremely low temperatures, essential for liquefying gases such as nitrogen, oxygen, hydrogen, helium, and natural gas. Rising adoption of vacuum-insulated piping, modular cryogenic tanks, and skid-mounted systems is enhancing efficiency and flexibility, while IoT-enabled sensors and predictive maintenance tools are improving operational reliability. Increasing utilization of cryogenic vaporizers, compressors, and flexible capacity solutions in industrial and petrochemical applications is redefining installation practices and creating opportunities for innovation in ultra-low temperature operations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $21.4 Billion |

| Forecast Value | $37 Billion |

| CAGR | 5.7% |

The valves segment is expected to reach USD 4 billion by 2035, driven by a preference for stainless steel and nickel alloys and adherence to stringent performance standards. Advanced valve designs focused on zero-emission operations are aligning with sustainability objectives, enabling safer and more efficient handling of cryogenic fluids.

The oxygen segment is projected to grow at a CAGR of 5.5% by 2035. Rising adoption of oxygen vaporizers and high-capacity storage systems is supporting industrial processes, including aerospace fueling applications. Integration of oxygen cryogenic pumps is further driving niche applications that demand precise and reliable low-temperature management.

U.S. Cryogenic Equipment Market held 85.7% share, generating USD 4.2 billion in 2025. Strong adoption of cryogenic tanks, coupled with peak shaving facilities, supports seasonal power demand management. Increasing deployment of IoT-enabled cryogenic pumps and predictive maintenance solutions is enabling smart and automated plant operations, improving efficiency and safety across the industry.

Major players active in the Global Cryogenic Equipment Market include Emerson Electric, Air Liquide, Chart Industries, Flowserve Corporation, Linde, Cryostar, Air Products and Chemicals, Kelvin International, IWI Cryogenic Vaporization Systems (India) Pvt. Ltd., Cryogas Equipment, CRYOSPAIN, BRUGG Pipes, Abhijit Enterprises, Cryoworld, Shell-n-Tube, Demaco, AIR WATER, Auguste Cryogenics, SLB, Cryogenic OGS, and Vacuum Barrier. Companies in the Cryogenic Equipment Market are focusing on multiple strategies to enhance their market presence and strengthen their competitive position. Key approaches include investing in R&D to develop next-generation, energy-efficient, and modular cryogenic solutions. Firms are pursuing strategic partnerships, joint ventures, and acquisitions to expand geographic reach and technological capabilities. Product differentiation through advanced materials, automated valve assemblies, and IoT-enabled monitoring systems is being emphasized to meet industry-specific requirements.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Market estimates & forecast parameters

- 1.3 Forecast

- 1.3.1 Key trends for market estimates

- 1.3.2 Quantified market impact analysis

- 1.3.2.1 Mathematical impact of growth parameters on forecast

- 1.3.3 Scenario analysis framework

- 1.4 Primary research and validation

- 1.4.1 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.2 Sources, by region

- 1.6 Research trail & scoring components

- 1.6.1 Research trail components

- 1.6.2 Scoring components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

- 1.8 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Product trends

- 2.4 Cryogen type trends

- 2.5 Application trends

- 2.6 End use trends

- 2.7 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of cryogenic equipment

- 3.8 Emerging opportunities & trends

- 3.9 Digitalization and IoT integration

- 3.10 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.3.1 Key partnerships & collaborations

- 4.3.2 Major M&A activities

- 4.3.3 Product innovations & launches

- 4.3.4 Market expansion strategies

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Product, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Tanks

- 5.3 Valves

- 5.4 Vaporizers

- 5.5 Pumps

- 5.6 Pipe

- 5.7 Others

Chapter 6 Market Size and Forecast, By Cryogen Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Nitrogen

- 6.3 Oxygen

- 6.4 Natural gas

- 6.5 Argon

- 6.6 Other cryogens

Chapter 7 Market Size and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Storage

- 7.3 Distribution

Chapter 8 Market Size and Forecast, By End Use, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 O&G industry

- 8.3 Power

- 8.4 Food & beverage

- 8.5 Chemical

- 8.6 Rubber & plastics

- 8.7 Metallurgy

- 8.8 Healthcare

- 8.9 Shipping

- 8.10 Agriculture, forestry & fishing

- 8.11 Other industries

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 Italy

- 9.3.4 Spain

- 9.3.5 France

- 9.3.6 Poland

- 9.3.7 Norway

- 9.3.8 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Indonesia

- 9.4.5 Thailand

- 9.4.6 Malaysia

- 9.4.7 Philippines

- 9.4.8 South Korea

- 9.4.9 Australia

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 Kuwait

- 9.5.4 Oman

- 9.5.5 Turkey

- 9.5.6 Qatar

- 9.5.7 Egypt

- 9.5.8 South Africa

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Argentina

- 9.6.3 Peru

Chapter 10 Company Profiles

- 10.1 Abhijit Enterprises

- 10.2 Air Liquide

- 10.3 Air Products and Chemicals

- 10.4 AIR WATER

- 10.5 Auguste Cryogenics

- 10.6 BRUGG Pipes

- 10.7 Chart Industries

- 10.8 Cryogas Equipment

- 10.9 Cryogenic OGS

- 10.10 CRYOSPAIN

- 10.11 Cryostar

- 10.12 Cryoworld

- 10.13 Demaco

- 10.14 Emerson Electric

- 10.15 Flowserve Corporation

- 10.16 Hypro

- 10.17 INOXCVA

- 10.18 IWI Cryogenic Vaporization Systems (India) Pvt. Ltd.

- 10.19 Kelvin International

- 10.20 Linde

- 10.21 Shell-n-Tube

- 10.22 SLB

- 10.23 Vacuum Barrier

低溫設備市場規模、佔有率、趨勢和預測:按設備、低溫介質、應用、最終用戶產業和地區分類,2026-2034年

低溫設備市場規模、佔有率、趨勢和預測:按設備、低溫介質、應用、最終用戶產業和地區分類,2026-2034年 低溫設備市場:2026-2032年全球市場預測(依產品類型、冷卻劑類型、應用、終端用戶產業及通路分類)低溫產品市場:依低溫設備、低溫氣體、應用及最終用戶分類-2026-2032年全球市場預測

低溫設備市場:2026-2032年全球市場預測(依產品類型、冷卻劑類型、應用、終端用戶產業及通路分類)低溫產品市場:依低溫設備、低溫氣體、應用及最終用戶分類-2026-2032年全球市場預測 2026年全球低溫設備市場報告

2026年全球低溫設備市場報告 全球低溫設備市場:按設備、低溫介質、終端用戶產業、系統類型、應用和地區分類-預測(至2030年)

全球低溫設備市場:按設備、低溫介質、終端用戶產業、系統類型、應用和地區分類-預測(至2030年) 全球低溫設備市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析、未來預測(2026-2034)

全球低溫設備市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析、未來預測(2026-2034) 低溫電子市場預測至2032年:按組件、溫度範圍、材料類型、應用、最終用戶和地區分類的全球分析

低溫電子市場預測至2032年:按組件、溫度範圍、材料類型、應用、最終用戶和地區分類的全球分析 低溫設備市場規模、佔有率和趨勢分析報告:按產品、低溫介質、應用、最終用途、地區和細分市場預測(2026-2033 年)

低溫設備市場規模、佔有率和趨勢分析報告:按產品、低溫介質、應用、最終用途、地區和細分市場預測(2026-2033 年) 低溫設備市場規模、佔有率和成長分析(按產品、低溫劑、系統類型、應用、最終用途和地區分類)-2026-2033年產業預測

低溫設備市場規模、佔有率和成長分析(按產品、低溫劑、系統類型、應用、最終用途和地區分類)-2026-2033年產業預測 低溫設備市場-全球產業規模、佔有率、趨勢、機會和預測,依產品類型、低溫物質類型、最終用戶、地區和競爭格局分類,2020-2030 年預測

低溫設備市場-全球產業規模、佔有率、趨勢、機會和預測,依產品類型、低溫物質類型、最終用戶、地區和競爭格局分類,2020-2030 年預測