|

市場調查報告書

商品編碼

1892858

動物飼料益生菌市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Animal Feed Probiotics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

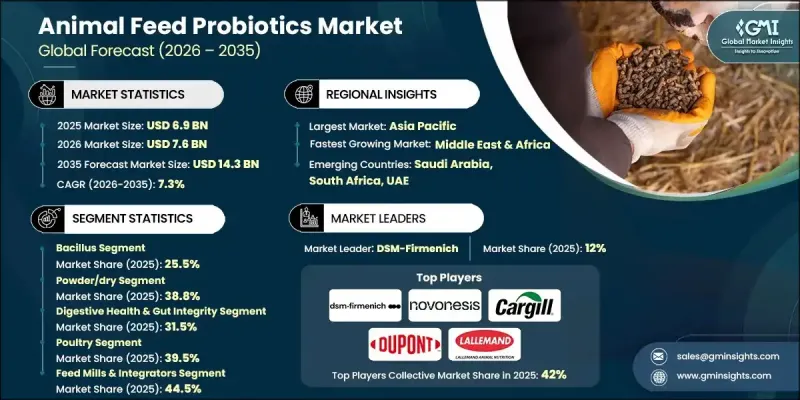

2025年全球動物飼料益生菌市場價值為69億美元,預計到2035年將以7.3%的複合年成長率成長至143億美元。

監管政策的轉變限制了動物營養中抗生素的使用,鼓勵生產者採用替代的健康管理方法,從而推動了益生菌市場的成長。飼料生產商越來越依賴以營養為基礎的解決方案,以維持腸道平衡並提升動物的整體生產性能。益生菌已成為這一轉變中不可或缺的一部分,它們作為一種專注於微生物組的成分,能夠在不依賴具有重要藥用價值的化合物的情況下改善動物健康狀況。由於全球飼料生產規模龐大,即使是適度的採用也能產生顯著的影響。在各種生產系統中觀察到的持續性能提升,包括更高的生長效率、更低的疾病壓力和更高的產品質量,進一步增強了市場對益生菌的接受度。這些益處使益生菌成為預防性動物健康策略的一部分,而非被動治療模式。永續性的考量也進一步增強了市場需求,因為益生菌有助於提高營養物質的利用率,並有助於降低對環境的影響,從而幫助生產者履行氣候承諾並滿足不斷變化的採購標準。

| 市場範圍 | |

|---|---|

| 起始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 69億美元 |

| 預測值 | 143億美元 |

| 複合年成長率 | 7.3% |

2025年,芽孢桿菌益生菌市佔率達到25.5%,預計到2035年將以6.6%的複合年成長率成長。它們在高溫加工和嚴苛的儲存條件下仍能保持穩定,因此在商業飼料生產中廣泛應用。這些特性使其成為在生產壓力下維持消化平衡和酶活性的可靠解決方案。

2025年,粉末和乾粉製劑市佔率為38.8%,預計從2026年到2035年將以6.2%的複合年成長率成長。其易於操作、混合均勻、保存期限長、成本效益高等優點,持續推動大規模飼料生產企業的採用。

預計2025年,北美動物飼料益生菌市佔率將達到29%。先進的生產系統、嚴格的監管以及無抗生素飼餵方案的廣泛應用,將持續推動市場擴張。該地區在精準營養和永續發展方面的領先地位,也促進了益生菌研發和應用領域的持續創新。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 科學支援的性能提升

- 管理和貿易要求

- 精準農業與穩定性技術

- 產業陷阱與挑戰

- 菌株變異性和劑量

- 監理複雜性

- 市場機遇

- 甲烷和營養管理

- 水產養殖與寵物營養。

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品類型

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依產品類型分類,2022-2035年

- 芽孢桿菌

- 乳酸桿菌

- 釀酒酵母(酵母型)

- 雙歧桿菌

- 腸球菌

- 後生元

- 鏈球菌

- 其他

第6章:市場估算與預測:依產品類型分類,2022-2035年

- 粉末/乾粉

- 微膠囊化

- 液體/可溶性

- 顆粒

- 其他

第7章:市場估計與預測:依功能分類,2022-2035年

- 消化系統健康與腸道完整性

- 免疫支持與調節

- 促進生長和飼料效率

- 病原體控制與競爭性排斥

- 壓力管理

- 其他

第8章:市場估算與預測:依畜牧業分類,2022-2035年

- 家禽

- 肉雞

- 層

- 育種者

- 其他

- 豬

- 仔豬(斷奶前和斷奶後)

- 種植者

- 終結者

- 其他

- 牛(反芻動物)

- 乳牛

- 肉牛

- 水產養殖

- 鮭魚

- 鱒魚

- 蝦

- 鯉魚

- 其他

- 寵物食品

- 狗

- 貓

- 馬科動物

- 其他

第9章:市場估算與預測:依配銷通路分類,2022-2035年

- 飼料廠和一體化企業

- 獸藥經銷商

- 直接銷售(生產商對農場)

- 線上/電子商務

- 其他

第10章:市場估計與預測:依最終用途分類,2022-2035年

- 商業/工業農場

- 小規模/後院作業

- 其他

第11章:市場估計與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第12章:公司簡介

- DSM-Firmenich

- Chr. Hansen (Novonesis)

- Cargill Animal Nutrition

- DuPont Nutrition & Biosciences (IFF)

- Lallemand Animal Nutrition

- Alltech

- Kemin Industries

- Evonik Industries

- Novus International

- Lesaffre Group

- Angel Yeast

- Biomin

- Nutreco

- MicroSynbiotiX

The Global Animal Feed Probiotics Market was valued at USD 6.9 billion in 2025 and is estimated to grow at a CAGR of 7.3% to reach USD 14.3 billion by 2035.

Growth is supported by regulatory shifts that limit the use of antibiotics in animal nutrition, encouraging producers to adopt alternative health management approaches. Feed manufacturers increasingly rely on nutrition-based solutions that support gut balance and overall animal performance. Probiotics have become an integral part of this transition as microbiome-focused ingredients that enhance health outcomes without relying on medically important compounds. Even modest adoption levels have a significant impact due to the sheer scale of global feed production. Market acceptance is reinforced by consistent performance improvements observed across production systems, including better growth efficiency, reduced disease pressure, and improved output quality. These benefits align probiotics with preventive animal health strategies rather than reactive treatment models. Sustainability considerations further strengthen demand, as probiotics support improved nutrient utilization and contribute to lower environmental impact, helping producers meet climate commitments and evolving sourcing standards.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.9 Billion |

| Forecast Value | $14.3 Billion |

| CAGR | 7.3% |

The bacillus-based probiotics segment held a 25.5% share in 2025 and is expected to grow at a CAGR of 6.6% through 2035. Their stability under high processing temperatures and challenging storage conditions supports widespread use in commercial feed manufacturing. These characteristics make them a reliable solution for maintaining digestive balance and enzyme activity under production stress.

The powder and dry formulations segment held 38.8% share in 2025 and is forecast to grow at a CAGR of 6.2% from 2026 to 2035. Their ease of handling, uniform blending, long shelf life, and cost efficiency continue to drive adoption across large-scale feed operations.

North America Animal Feed Probiotics Market captured 29% share in 2025. Advanced production systems, strong regulatory oversight, and widespread adoption of antibiotic-free feeding programs continue to support market expansion. Regional leadership in precision nutrition and sustainability initiatives encourages ongoing innovation in probiotic development and delivery.

Key companies operating in the Global Animal Feed Probiotics Market include Chr. Hansen (Novonesis), DSM-Firmenich, Alltech, Cargill Animal Nutrition, Lallemand Animal Nutrition, Evonik Industries, Kemin Industries, DuPont Nutrition & Biosciences (IFF), Nutreco, Novus International, Lesaffre Group, Angel Yeast, Biomin, and MicroSynbiotiX. Companies in the Animal Feed Probiotics Market pursue focused strategies to strengthen their competitive position. Investment in research and strain development remains a priority to enhance efficacy and stability. Manufacturers expand product portfolios to address evolving regulatory and sustainability requirements. Strategic partnerships with feed producers support wider market penetration and application expertise. Firms emphasize quality assurance and traceability to build customer trust. Geographic expansion into high-growth regions improves scale and distribution reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Form

- 2.2.4 Function

- 2.2.5 Livestock

- 2.2.6 Distribution Channel

- 2.2.7 End Use

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Science-backed performance gains

- 3.2.1.2 Stewardship and trade requirements

- 3.2.1.3 Precision farming & stability tech

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Strain variability & dosing

- 3.2.2.2 Regulatory complexity

- 3.2.3 Market opportunities

- 3.2.3.1 Methane and nutrient management

- 3.2.3.2 Aquaculture and pet nutrition.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Bacillus

- 5.3 Lactobacilli

- 5.4 Saccharomyces (Yeast-Based)

- 5.5 Bifidobacterium

- 5.6 Enterococcus

- 5.7 Postbiotics

- 5.8 Streptococcus

- 5.9 Others

Chapter 6 Market Estimates and Forecast, By Form, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Powder/Dry

- 6.3 Microencapsulated

- 6.4 Liquid/Soluble

- 6.5 Granules

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Function, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Digestive health & gut integrity

- 7.3 Immune support & modulation

- 7.4 Growth promotion & feed efficiency

- 7.5 Pathogen control & competitive exclusion

- 7.6 Stress management

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Livestock, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Poultry

- 8.2.1 Broilers

- 8.2.2 Layers

- 8.2.3 Breeders

- 8.2.4 Others

- 8.3 Swine

- 8.3.1 Piglets (pre-weaning & post-weaning)

- 8.3.2 Growers

- 8.3.3 Finishers

- 8.3.4 Others

- 8.4 Cattle (ruminants)

- 8.4.1 Dairy cattle

- 8.4.2 Beef cattle

- 8.5 Aquaculture

- 8.5.1 Salmon

- 8.5.2 Trout

- 8.5.3 Shrimp

- 8.5.4 Carp

- 8.5.5 Others

- 8.6 Pet food

- 8.6.1 Dogs

- 8.6.2 Cats

- 8.7 Equine

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Feed mills & integrators

- 9.3 Veterinary distributors

- 9.4 Direct sales (manufacturer to farm)

- 9.5 Online/e-commerce

- 9.6 Others

Chapter 10 Market Estimates and Forecast, By End Use, 2022-2035 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 Commercial/industrial farms

- 10.3 Small-scale/backyard operations

- 10.4 Others

Chapter 11 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East and Africa

Chapter 12 Company Profiles

- 12.1 DSM-Firmenich

- 12.2 Chr. Hansen (Novonesis)

- 12.3 Cargill Animal Nutrition

- 12.4 DuPont Nutrition & Biosciences (IFF)

- 12.5 Lallemand Animal Nutrition

- 12.6 Alltech

- 12.7 Kemin Industries

- 12.8 Evonik Industries

- 12.9 Novus International

- 12.10 Lesaffre Group

- 12.11 Angel Yeast

- 12.12 Biomin

- 12.13 Nutreco

- 12.14 MicroSynbiotiX

2026-2034年全球動物飼料益生菌市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球動物飼料益生菌市場規模、佔有率、趨勢和成長分析報告 動物飼料益生菌市場-全球產業規模、佔有率、趨勢、機會和預測:按動物種類、原料、劑型、分銷管道、地區和競爭格局分類,2021-2031年

動物飼料益生菌市場-全球產業規模、佔有率、趨勢、機會和預測:按動物種類、原料、劑型、分銷管道、地區和競爭格局分類,2021-2031年 動物飼料益生菌市場規模、佔有率和成長分析(按動物種類、市場來源、劑型、通路、功能和地區分類)-2026-2033年產業預測

動物飼料益生菌市場規模、佔有率和成長分析(按動物種類、市場來源、劑型、通路、功能和地區分類)-2026-2033年產業預測 動物飼料益生菌市場規模、佔有率和成長分析(按形態、來源、動物種類和地區分類)—產業預測(2026-2033 年)

動物飼料益生菌市場規模、佔有率和成長分析(按形態、來源、動物種類和地區分類)—產業預測(2026-2033 年) 全球精準益生菌市場:預測至2032年-按產品類型、劑型、通路、應用、最終用戶和地區分類的分析

全球精準益生菌市場:預測至2032年-按產品類型、劑型、通路、應用、最終用戶和地區分類的分析 動物飼料益生菌市場:全球按產地、牲畜、形態、菌株、功能、分銷管道和地區分類 - 預測至 2030 年

動物飼料益生菌市場:全球按產地、牲畜、形態、菌株、功能、分銷管道和地區分類 - 預測至 2030 年 食品、飲料、營養補充品和飼料中的益生菌至 2030 年動物飼料中益生菌市場預測:按成分、形式、功能、牲畜、銷售管道和地區進行的全球分析

食品、飲料、營養補充品和飼料中的益生菌至 2030 年動物飼料中益生菌市場預測:按成分、形式、功能、牲畜、銷售管道和地區進行的全球分析