|

市場調查報告書

商品編碼

1892833

輕型卡車轉向系統市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Light Duty Truck Steering System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

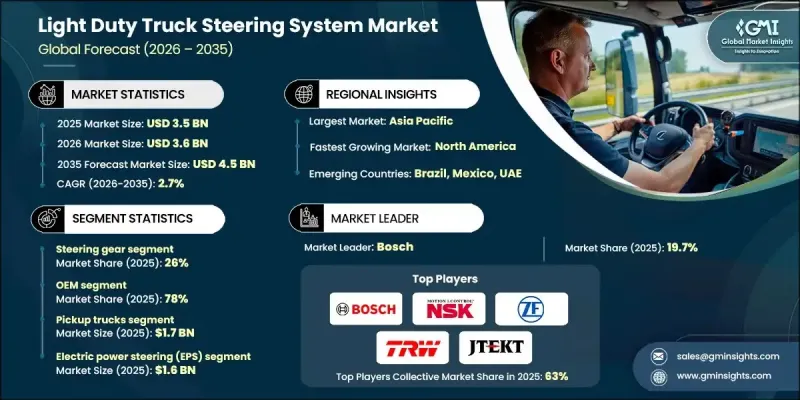

2025 年全球輕型卡車轉向系統市場價值為 35 億美元,預計到 2035 年將以 2.7% 的複合年成長率成長至 45 億美元。

市場擴張的驅動力來自對更先進、更安全、更有效率的轉向技術日益成長的需求,以及電動和混合動力輕型卡車的普及和商業物流業務的成長。車隊營運商和個人買家都將駕駛員的舒適性、車輛操控性和安全性放在首位,因此,現代轉向系統對於在各種路況和作業環境下實現可靠操控至關重要。電動輔助轉向 (EPS)、液壓動力轉向系統、自適應轉向模組以及輕量化高強度零件等創新技術正在改變這些卡車的功能。鋁合金、高強度鋼和耐腐蝕塗層等優質材料確保了轉向解決方案的耐用性和持久性。城市物流、最後一公里配送服務、共享出行車隊的擴張,以及對具備更佳操控性和安全性的卡車的需求,正在加速全球市場的普及。

| 市場範圍 | |

|---|---|

| 起始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 35億美元 |

| 預測值 | 45億美元 |

| 複合年成長率 | 2.7% |

轉向器市場在2025年佔據26%的市場佔有率,預計2026年至2035年將以2.2%的複合年成長率成長。轉向器對於皮卡、廂型車和輕型商用卡車的精準操控、穩定性和機動性至關重要。它們堅固耐用,可相容於液壓、電動和電液系統,並且在重載和多變負載條件下都能保持可靠性,因此成為原始設備製造商 (OEM) 和車隊營運商的首選。

2025年, OEM)OEM達到78%,預計到2035年將以2.3%的複合年成長率成長。 OEM通路將轉向系統整合到新卡車中,確保使用符合安全和性能標準的認證優質組件。這些系統具有無縫的車輛相容性、更高的駕駛舒適性、耐用性和精準性。 OEM安裝因其可靠性以及與EPS(電動OEM系統)、ADAS(高級駕駛輔助系統)和車輛遠端資訊處理等先進技術的兼容性而備受青睞。

中國輕型卡車轉向系統市場佔33%的市場佔有率,預計2025年市場規模將達到4.435億美元。市場成長的主要驅動力包括皮卡和輕型商用車的強勁產量、對先進汽車技術的投資,以及EPS、線控轉向和ADAS整合轉向解決方案的廣泛應用。政府對新能源汽車的支持和日益嚴格的安全法規也進一步推動了現代轉向系統的應用。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 成本結構

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 對先進轉向技術的需求不斷成長

- 輕型卡車車隊的成長

- 注重駕駛員的舒適性和安全性

- 技術整合與材料創新

- 產業陷阱與挑戰

- 高昂的系統成本

- 複雜的維護要求

- 市場機遇

- 電動和混合動力輕型卡車的擴張

- 售後市場和改造解決方案

- ADAS與自動駕駛車輛整合

- 輕便節能的系統

- 成長促進因素

- 成長潛力分析

- 監管環境

- 波特的分析

- PESTEL 分析

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 生產統計

- 生產中心

- 消費中心

- 進出口

- 成本細分分析

- 專利分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 投資與融資分析

- OEM研發投資趨勢

- 供應商資本支出分配

- 科技新創公司融資格局

- 最佳情況

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估算與預測:依組件分類,2022-2035年

- 轉向器

- 轉向柱

- 感測器和控制器

- 轉向泵浦

- 拉桿

- 方向盤

- 其他

第6章:市場估價與預測:依車輛類型分類,2022-2035年

- 皮卡車

- SUV 與跨界車

- 輕型商用車(LCV)

- 范斯

第7章:市場估計與預測:依技術分類,2022-2035年

- 電動輔助轉向系統(EPS)

- 液壓動力轉向(HPS)

- 電液輔助轉向(EHPS)

- 線控轉向

第8章:市場估算與預測:依銷售管道分類,2022-2035年

- OEM

- 售後市場

第9章:市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 比利時

- 荷蘭

- 瑞典

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 新加坡

- 韓國

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第10章:公司簡介

- Global Player

- Bosch

- Denso

- Hyundai Mobis

- JTEKT

- Magna International

- Nexteer Automotive

- NSK

- Thyssenkrupp

- TRW Automotive

- ZF Friedrichshafen

- Regional Player

- Aisin Seiki

- Calsonic Kansei

- Hitachi Astemo

- JMC Steering

- Kongsberg Automotive

- Mando

- Mevotech

- Mubea

- Schaeffler

- KYB

- 新興參與者

- Auto Steering Technologies

- Eberspacher Steering Solutions

- Neapco

- Protean Electric

- Servotronic Systems

The Global Light Duty Truck Steering System Market was valued at USD 3.5 billion in 2025 and is estimated to grow at a CAGR of 2.7% to reach USD 4.5 billion by 2035.

The market expansion is fueled by increasing demand for advanced, safer, and more efficient steering technologies, alongside the rising adoption of electric and hybrid light-duty trucks and the growth of commercial and logistics operations. Fleet operators and individual buyers are prioritizing driver comfort, vehicle maneuverability, and safety, making modern steering systems essential for reliable handling across diverse road conditions and operational settings. Innovations such as electric power steering (EPS), hydraulic-assisted systems, adaptive steering modules, and lightweight, high-strength components are transforming the functionality of these trucks. High-quality materials, including aluminum alloys, high-strength steel, and corrosion-resistant coatings, ensure durable, long-lasting steering solutions. Expanding urban logistics, last-mile delivery services, ride-sharing fleets, and demand for trucks with enhanced handling and safety features are accelerating market adoption globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.5 Billion |

| Forecast Value | $4.5 Billion |

| CAGR | 2.7% |

The steering gear segment held a 26% share in 2025 and is expected to grow at a CAGR of 2.2% from 2026 to 2035. Steering gears are critical for precise vehicle control, stability, and maneuverability across pickups, vans, and light commercial trucks. They offer robustness, compatibility with hydraulic, electric, and electro-hydraulic architectures, and reliability under heavy-duty and variable load conditions, making them a preferred choice for OEMs and fleet operators.

The OEM segment held 78% share in 2025 and is forecasted to grow at a CAGR of 2.3% through 2035. OEM channels integrate steering systems into new trucks, ensuring the use of certified, high-quality components that meet safety and performance standards. These systems offer seamless vehicle compatibility, enhanced driver comfort, durability, and precision. OEM installations are favored for their reliability and alignment with advanced technologies such as EPS, ADAS, and vehicle telematics.

China Light Duty Truck Steering System Market held a 33% share, generating USD 443.5 million in 2025. Growth is driven by strong production of pickups and light commercial vehicles, investments in advanced automotive technologies, and the adoption of EPS, steer-by-wire, and ADAS-integrated steering solutions. Government support for new energy vehicles and stricter safety regulations are further boosting the use of modern steering systems.

Key players operating in the Light Duty Truck Steering System Market include JTEKT, NSK, Thyssenkrupp, ZF Friedrichshafen, Bosch, Hyundai Mobis, Delphi Technologies, TRW Automotive, Denso, and KYB. Companies are focusing on technological innovation to enhance steering system performance, reliability, and fuel efficiency while integrating advanced features like EPS, ADAS, and steer-by-wire capabilities. Strategic partnerships with OEMs and logistics fleet operators enable the adoption of cutting-edge steering solutions in new vehicles and retrofit applications. Firms are investing in lightweight, durable materials to reduce vehicle weight and improve fuel economy. Expanding regional production and supply chain networks ensures timely delivery and cost optimization. Research and development efforts target improved system precision, longevity, and compatibility with hybrid and electric trucks. Companies are also leveraging digital platforms for predictive maintenance, diagnostics, and telematics integration, strengthening their market presence and building long-term relationships with customers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 Technology

- 2.2.5 Sales channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for advanced steering technologies

- 3.2.1.2 Growth of light-duty truck fleets

- 3.2.1.3 Focus on driver comfort and safety

- 3.2.1.4 Technological integration and material innovations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High system costs

- 3.2.2.2 Complex maintenance requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of electric and hybrid light-duty trucks

- 3.2.3.2 Aftermarket and retrofit solutions

- 3.2.3.3 ADAS & autonomous vehicle integration

- 3.2.3.4 Lightweight & energy-efficient systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Investment & Funding Analysis

- 3.13.1 OEM R&D investment trends

- 3.13.2 Supplier capex allocation

- 3.13.3 Technology startup funding landscape

- 3.14 Best case scenarios

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($ Bn, Units)

- 5.1 Key trends

- 5.2 Steering gear

- 5.3 Steering column

- 5.4 Sensors & controllers

- 5.5 Steering pumps

- 5.6 Tie rods

- 5.7 Steering wheel

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($ Bn, Units)

- 6.1 Key trends

- 6.2 Pickup trucks

- 6.3 SUVs & crossovers

- 6.4 Light commercial vehicles (LCV)

- 6.5 Vans

Chapter 7 Market Estimates & Forecast, By Technology, 2022 - 2035 ($ Bn, Units)

- 7.1 Key trends

- 7.2 Electric power steering (EPS)

- 7.3 Hydraulic power steering (HPS)

- 7.4 Electro-hydraulic power steering (EHPS)

- 7.5 Steer-by-wire

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($ Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($ Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Belgium

- 9.3.7 Netherlands

- 9.3.8 Sweden

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 Singapore

- 9.4.6 South Korea

- 9.4.7 Vietnam

- 9.4.8 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Global Player

- 10.1.1 Bosch

- 10.1.2 Denso

- 10.1.3 Hyundai Mobis

- 10.1.4 JTEKT

- 10.1.5 Magna International

- 10.1.6 Nexteer Automotive

- 10.1.7 NSK

- 10.1.8 Thyssenkrupp

- 10.1.9 TRW Automotive

- 10.1.10 ZF Friedrichshafen

- 10.2 Regional Player

- 10.2.1 Aisin Seiki

- 10.2.2 Calsonic Kansei

- 10.2.3 Hitachi Astemo

- 10.2.4 JMC Steering

- 10.2.5 Kongsberg Automotive

- 10.2.6 Mando

- 10.2.7 Mevotech

- 10.2.8 Mubea

- 10.2.9 Schaeffler

- 10.2.10 KYB

- 10.3 Emerging Players

- 10.3.1 Auto Steering Technologies

- 10.3.2 Eberspacher Steering Solutions

- 10.3.3 Neapco

- 10.3.4 Protean Electric

- 10.3.5 Servotronic Systems

小型車輛轉向系統市場:按轉向系統、機構、車輛類型、應用和銷售管道分類-2026-2032年全球市場預測

小型車輛轉向系統市場:按轉向系統、機構、車輛類型、應用和銷售管道分類-2026-2032年全球市場預測 2026年全球中重型卡車轉向系統市場報告2026年全球汽車轉向與懸吊零件市場報告2026年全球汽車電氣電子設備、轉向懸吊和內裝市場報告2026年全球汽車齒輪齒條式轉向系統市場報告2026年全球轉向裝置市場報告2026年輕型商用車轉向系統全球市場報告汽車轉向感測器市場:感測器類型、感測器技術、轉向系統類型和車輛類型—2026-2032年全球市場預測

2026年全球中重型卡車轉向系統市場報告2026年全球汽車轉向與懸吊零件市場報告2026年全球汽車電氣電子設備、轉向懸吊和內裝市場報告2026年全球汽車齒輪齒條式轉向系統市場報告2026年全球轉向裝置市場報告2026年輕型商用車轉向系統全球市場報告汽車轉向感測器市場:感測器類型、感測器技術、轉向系統類型和車輛類型—2026-2032年全球市場預測 汽車轉向節市場 - 全球產業規模、佔有率、趨勢、機會、預測:按車輛類型、按類型、按銷售管道類型、按地區和競爭對手分類,2021-2031年汽車轉向感測器市場-全球產業規模、佔有率、趨勢、機會和預測,按感測器類型、車輛類型、技術、地區和競爭格局分類,2021-2031年預測

汽車轉向節市場 - 全球產業規模、佔有率、趨勢、機會、預測:按車輛類型、按類型、按銷售管道類型、按地區和競爭對手分類,2021-2031年汽車轉向感測器市場-全球產業規模、佔有率、趨勢、機會和預測,按感測器類型、車輛類型、技術、地區和競爭格局分類,2021-2031年預測