|

市場調查報告書

商品編碼

1892828

導絲市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Guidewires Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

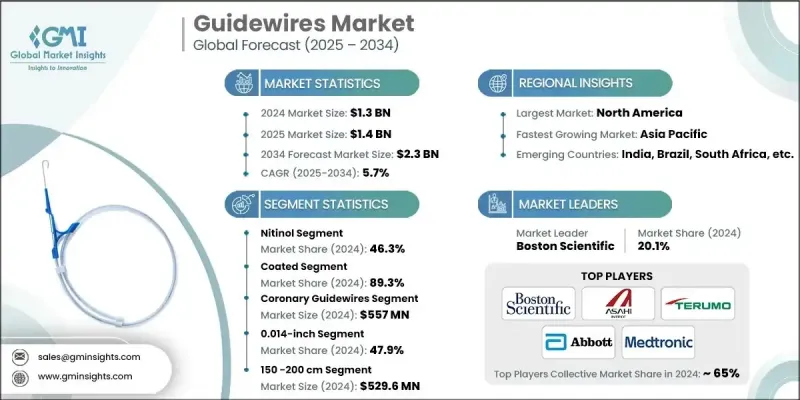

2024 年全球導絲市場價值為 13 億美元,預計到 2034 年將以 5.7% 的複合年成長率成長至 23 億美元。

市場擴張的促進因素包括老年人口的成長、生活型態相關疾病盛行率的上升、已開發國家有利的健保報銷政策以及心血管疾病發生率的增加。導絲設計的技術進步,例如智慧導絲和生物可吸收導絲,進一步推動了導絲的應用。醫療保健從傳統開放性手術轉變為微創手術(包括經皮冠狀動脈介入治療 (PCI)、神經血管介入治療和血管內治療)的轉變,顯著促進了市場成長。這些手術可以減少創傷、縮短住院時間並加速復原。導絲在幫助臨床醫生精準操控複雜血管結構、提高手術成功率和改善患者預後方面發揮著至關重要的作用。新興經濟體醫療基礎設施的擴建也為導絲的應用創造了新的機會。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 13億美元 |

| 預測值 | 23億美元 |

| 複合年成長率 | 5.7% |

2024 年,鎳鈦諾細分市場佔 46.3% 的市佔率。由於有利的報銷政策和優異的材料性能(包括形狀記憶和超彈性),預計該細分市場將繼續成長,這些性能為在心血管、外周和神經血管手術中穿過迂曲血管提供了增強的柔韌性和抗扭結性。

2024 年,塗層導絲佔了 89.3% 的市佔率。採用親水、抗血栓、疏水和矽基技術的塗層導絲因其臨床療效和在介入手術中的廣泛應用而備受青睞。

2024年,北美導絲市佔率將達到37.7%。該地區受益於先進的醫療基礎設施、高手術量、微創介入治療的快速普及以及持續的技術創新。心血管疾病、周邊動脈疾病、神經血管疾病和泌尿系統疾病的高發生率推動了導絲在診斷和治療應用方面的需求。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 產業影響因素

- 成長促進因素

- 微創手術的普及率不斷提高

- 發展中國家生活方式疾病數量不斷增加

- 已開發國家的各種報銷政策

- 全球老年人口基數不斷成長

- 產業陷阱與挑戰

- 導絲成本高昂

- 發展中經濟體缺乏技術熟練的專業人才

- 導絲相關風險

- 機會

- 新興經濟體醫療衛生基礎設施的擴張

- 影像導引和機器人輔助介入治療技術的應用日益廣泛

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 美國

- 加拿大

- 歐洲

- 中國

- 北美洲

- 技術與創新格局

- 當前技術趨勢

- 增強型親水和疏水塗層技術

- 扭矩控制和轉向性能最佳化

- 多層複合材料的整合

- 新興技術

- 奈米技術增強的表面工程

- 磁導導航系統

- 3D列印個人化導絲原型

- 當前技術趨勢

- 未來市場趨勢

- 向完全整合的數位化介入治療中心轉變的趨勢日益明顯

- 人們越來越傾向選擇一次性、無菌且經濟實惠的導絲

- 擴大微創和門診介入治療

- 報銷方案

- 2024年各地區定價分析

- 按材料

- 透過申請

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依材料分類,2021-2034年

- 鎳鈦諾

- 不銹鋼

- 混合

- 其他材料

第6章:市場估算與預測:依塗料產業分類,2021-2034年

- 塗層

- 親水塗層

- 抗血栓/肝素塗層

- 疏水塗層

- 矽塗層

- 四氟乙烯(TFE)塗層

- 未塗層

第7章:市場估計與預測:依應用領域分類,2021-2034年

- 冠狀動脈導絲

- 外周導絲

- 泌尿科導絲

- 神經血管導絲

- 其他應用

第8章:市場估算與預測:依直徑分類,2021-2034年

- 0.014英寸

- 0.018英寸

- 0.025英寸

- 0.032英寸

- 0.035英寸

- 0.038英寸

第9章:市場估計與預測:依長度分類,2021-2034年

- 80-145厘米

- 150-200厘米

- 210-300厘米

- 305公分以上

第10章:市場估計與預測:依最終用途分類,2021-2034年

- 醫院

- 門診手術中心

- 其他最終用途

第11章:市場估計與預測:按地區分類,2021-2034年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- Abbott Laboratories

- AngioDynamics

- ASAHI INTECC

- B. Braun SE

- Becton, Dickinson and Company

- Boston Scientific

- Cordis

- Cook Medical

- Medtronic

- Merit Medical Systems

- Olympus

- Stryker

- Teleflex

- Terumo

The Global Guidewires Market was valued at USD 1.3 billion in 2024 and is estimated to grow at a CAGR of 5.7% to reach USD 2.3 billion by 2034.

Market expansion is driven by the rising elderly population, increasing prevalence of lifestyle-related disorders, supportive reimbursement policies in developed countries, and growing rates of cardiovascular diseases. Technological advancements in guidewire design, such as smart and bioresorbable models, are further fueling adoption. The shift in healthcare from traditional open surgeries to minimally invasive procedures, including Percutaneous Coronary Intervention (PCI), neurovascular interventions, and endovascular therapies, is significantly contributing to market growth. These procedures reduce trauma, shorten hospital stays, and accelerate recovery. Guidewires play a critical role in enabling clinicians to navigate complex vascular structures with precision, improving procedural success and patient outcomes. Expansion of healthcare infrastructure in emerging economies is also creating new opportunities for guidewire deployment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $2.3 Billion |

| CAGR | 5.7% |

In 2024, the nitinol segment held a 46.3% share 2024. This segment is expected to continue growing due to favorable reimbursement policies and superior material properties, including shape-memory and super-elasticity, which provide enhanced flexibility and kink resistance for navigating tortuous vessels in cardiovascular, peripheral, and neurovascular procedures.

The coated segment held a 89.3% share in 2024. Coated guidewires, using hydrophilic, anti-thrombogenic, hydrophobic, and silicone-based technologies, are preferred for their clinical efficiency and widespread use in interventional procedures.

North America Guidewires Market accounted for a 37.7% share in 2024. The region benefits from advanced healthcare infrastructure, high procedural volumes, rapid adoption of minimally invasive interventions, and continuous technological innovation. High prevalence of cardiovascular diseases, peripheral artery disease, neurovascular conditions, and urological disorders drives demand for guidewires for both diagnostic and therapeutic applications.

Key players operating in the Global Guidewires Market include Boston Scientific, Medtronic, Abbott Laboratories, Cook Medical, Stryker, B. Braun SE, AngioDynamics, Teleflex, Cordis, Olympus, Merit Medical Systems, ASAHI INTECC, Becton Dickinson and Company, and Terumo. Companies in the Global Guidewires Market are strengthening their position by focusing on technological innovation and product differentiation, including the development of smart, coated, and bioresorbable guidewires. Collaborations with hospitals, research centers, and medical device distributors enhance market penetration and clinical adoption. Firms are expanding their footprint in emerging markets by establishing local manufacturing and distribution networks to meet growing procedural demand. Regulatory compliance and securing favorable reimbursement policies also play a vital role in driving sales. Strategic mergers and acquisitions enable companies to consolidate expertise, expand product portfolios, and access advanced R&D capabilities.a

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends (USD Mn & 000' Units)

- 2.2.2 Material trends (USD Mn & 000' Units)

- 2.2.3 Coating trends

- 2.2.4 Application trends (USD Mn & 000' Units)

- 2.2.5 Diameter trends (USD Mn & 000' Units)

- 2.2.6 Length trends (USD Mn & 000' Units)

- 2.2.7 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of minimally invasive surgical procedures

- 3.2.1.2 Increasing number of lifestyle disorders in developing countries

- 3.2.1.3 Various reimbursement policies in developed countries

- 3.2.1.4 Growing geriatric population base across the globe

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of guidewires

- 3.2.2.2 Dearth of skilled professionals in developing economies

- 3.2.2.3 Risks associated with guidewires

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of healthcare infrastructure in emerging economies

- 3.2.3.2 Growing adoption of image-guided and robotic-assisted interventions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 China

- 3.4.1 North America

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.1.1 Enhanced hydrophilic and hydrophobic coating technologies

- 3.5.1.2 Torque-control and steerability optimization

- 3.5.1.3 Integration of multi-layered composite materials

- 3.5.2 Emerging technologies

- 3.5.2.1 Nanotechnology-enhanced surface engineering

- 3.5.2.2 Magnetically guided navigation systems

- 3.5.2.3 3D-printed personalized guidewire prototypes

- 3.5.1 Current technological trends

- 3.6 Future market trends

- 3.6.1 Rising shift toward fully integrated digital interventional suites

- 3.6.2 Growing preference for single-use, sterile, and cost-efficient guidewires

- 3.6.3 Expansion of minimally invasive and outpatient-based interventions

- 3.7 Reimbursement scenario

- 3.8 Pricing analysis, by region, 2024

- 3.8.1 By Material

- 3.8.2 By Application

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 Latin America

- 4.3.6 MEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Nitinol

- 5.3 Stainless steel

- 5.4 Hybrid

- 5.5 Other materials

Chapter 6 Market Estimates and Forecast, By Coating, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Coated

- 6.2.1 Hydrophilic coating

- 6.2.2 Anti-thrombogenic/Heparin coating

- 6.2.3 Hydrophobic coating

- 6.2.4 Silicone coating

- 6.2.5 Tetrafluoroethylene (TFE) coating

- 6.3 Non-coated

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn and Units)

- 7.1 Key trends

- 7.2 Coronary guidewires

- 7.3 Peripheral guidewires

- 7.4 Urology guidewires

- 7.5 Neurovascular guidewires

- 7.6 Other applications

Chapter 8 Market Estimates and Forecast, By Diameter, 2021 - 2034 ($ Mn and Units)

- 8.1 Key trends

- 8.2 0.014 inch

- 8.3 0.018 inch

- 8.4 0.025 inch

- 8.5 0.032 inch

- 8.6 0.035 inch

- 8.7 0.038 inch

Chapter 9 Market Estimates and Forecast, By Length, 2021 - 2034 ($ Mn and Units)

- 9.1 Key trends

- 9.2 80 - 145 cm

- 9.3 150 - 200 cm

- 9.4 210 - 300 cm

- 9.5 Above 305 cm

Chapter 10 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Hospitals

- 10.3 Ambulatory surgical centers

- 10.4 Other End use

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Abbott Laboratories

- 12.2 AngioDynamics

- 12.3 ASAHI INTECC

- 12.4 B. Braun SE

- 12.5 Becton, Dickinson and Company

- 12.6 Boston Scientific

- 12.7 Cordis

- 12.8 Cook Medical

- 12.9 Medtronic

- 12.10 Merit Medical Systems

- 12.11 Olympus

- 12.12 Stryker

- 12.13 Teleflex

- 12.14 Terumo

導管導引線市場:按材料、類型、應用和最終用戶分類-2026-2032年全球市場預測血管導管導引線市場:2026-2032年全球市場預測(依產品類型、應用、材質、塗層、直徑範圍、尖端形狀和最終用戶分類)壓力導管導引線市場:按類型、技術、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測

導管導引線市場:按材料、類型、應用和最終用戶分類-2026-2032年全球市場預測血管導管導引線市場:2026-2032年全球市場預測(依產品類型、應用、材質、塗層、直徑範圍、尖端形狀和最終用戶分類)壓力導管導引線市場:按類型、技術、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測 2026年全球醫用鎢合金屏蔽市場報告導管導引線全球市場報告2026

2026年全球醫用鎢合金屏蔽市場報告導管導引線全球市場報告2026 全球微引導管市場規模、佔有率、趨勢和成長分析報告(2026-2034年)導管導引線全球市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球微引導管市場規模、佔有率、趨勢和成長分析報告(2026-2034年)導管導引線全球市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026-2030年全球導管導引線市場一次性神經血管導引線市場按產品類型、材料、銷售管道、應用和最終用戶分類-全球預測,2026-2032年介入支撐線市場按類型、材質、產品、直徑、應用和最終用戶分類-2026-2032年全球預測

2026-2030年全球導管導引線市場一次性神經血管導引線市場按產品類型、材料、銷售管道、應用和最終用戶分類-全球預測,2026-2032年介入支撐線市場按類型、材質、產品、直徑、應用和最終用戶分類-2026-2032年全球預測