|

市場調查報告書

商品編碼

1892827

尿囊素市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Allantoin Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

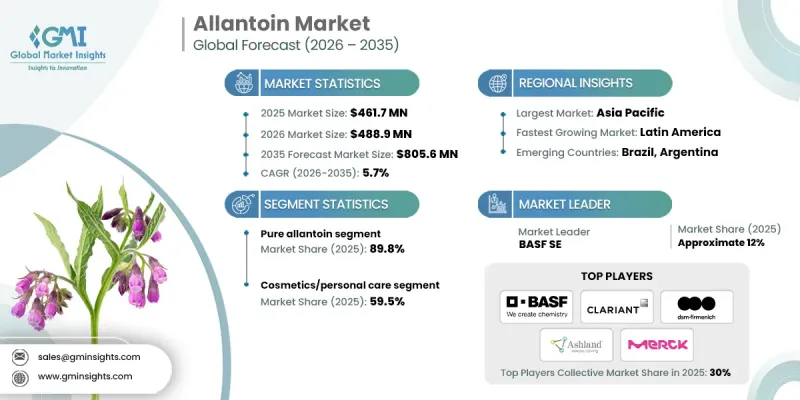

2025 年全球尿囊素市場價值為 4.617 億美元,預計到 2035 年將以 5.7% 的複合年成長率成長至 8.056 億美元。

市場擴張主要受化妝品、個人護理和外用治療配方中對多功能護膚成分日益成長的需求所驅動。尿囊素有植物來源和合成兩種形式,因其舒緩、保濕和促進肌膚更新的功效而備受推崇,尤其適用於針對乾燥、刺激和表層皮膚損傷的配方。監管機構的認可進一步增強了製造商的信心,因為尿囊素在規定的濃度範圍內被認定為安全有效,可用於非處方外用保護劑。此外,更清潔的配方、以植物為主導的原料採購以及不斷發展的生產技術也促進了市場成長,這些都有助於確保產品品質和配方的穩定性。對某些合成化合物的調節壓力加速了向更安全、更成熟的活性成分的過渡,提高了安全性和功效俱佳的成分的採用率。這些因素共同鞏固了尿囊素作為現代護膚和治療產品開發中核心成分的地位。

| 市場範圍 | |

|---|---|

| 起始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 4.617億美元 |

| 預測值 | 8.056億美元 |

| 複合年成長率 | 5.7% |

2025 年,純尿囊素市佔率達到 89.8%,預計到 2035 年將以 5.6% 的複合年成長率成長。其穩定的性能、配方穩定性和與多種產品的兼容性,使其在臨床級和清潔標籤配方中廣泛應用。

2025年,化妝品和個人護理應用領域佔市場佔有率的59.5%,預計從2026年到2035年將以5.4%的複合年成長率成長。由於尿囊素具有多功能功效,其在護膚、美容和護髮產品中的廣泛應用將繼續推動需求成長。

2025年歐洲尿囊素市場創造了1.551億美元的收入。強大的生產標準、穩固的製藥能力以及對優質製劑的高需求支撐了該地區的業績,儘管經濟擴張速度相對較慢。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 產業陷阱與挑戰

- 市場機遇

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依類型分類,2022-2035年

- 純尿囊素

- ALCLOXA(尿囊素+氫氧化鋁)

- ALDIOXA(尿囊素 + 二羥基尿囊素鋁)

- ALPANTHA(尿囊素 + D-泛醇)

- 其他衍生性商品

第6章:市場估算與預測:依來源分類,2022-2035年

- 合成的

- 天然/植物

第7章:市場估算與預測:依等級分類,2022-2035年

- USP/EP(藥品)

- CTFA(化妝品級)

- 技術級

第8章:市場估算與預測:依應用領域分類,2022-2035年

- 化妝品/個人護理

- 護膚霜和乳液

- 抗衰老產品

- 痤瘡治療

- 防曬乳

- 刮鬍產品

- 護髮產品

- 唇部護理及潤唇膏

- 嬰兒護理產品

- 製藥

- 傷口癒合軟膏

- 燒傷治療產品

- 痔瘡膏

- 外用消炎凝膠

- 處方皮膚科產品

- 疤痕修復產品

- 口腔衛生

- 牙膏

- 漱口水

- 牙齦癒合產品

- 敏感牙齒配方

- 農業

- 植物生長促進劑

- 土壤改良劑

- 作物保護噴霧劑

- 生物促效劑

- 其他

- 寵物護理產品

- 工業皮膚保護霜

- 盥洗用品和衛生濕紙巾

- 消毒霜

第9章:市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第10章:公司簡介

- BASF SE

- Akema Srl

- Alfa Aesar

- Allan Chemical Corporation

- Ashland Inc.

- Clariant AG

- DSM-Firmenich

- Hubei Guanhao Biological Technology Co., Ltd.

- Innospec Inc.

- Jeen International Corporation

- Luotian Guanghui Chemical Co., Ltd.

- Luvena SA

- Merck KGaA

- Rita Corporation

- Shandong Xinhua Pharmaceutical Co., Ltd.

- SinoLion Chemical Co., Ltd.

- Suzhou-Chem Inc.

- Yongan Pharmaceutical Co., Ltd.

- Zhanjiang Dongjian Chemicals Co., Ltd.

- Zhejiang NHU Co., Ltd.

- Others

The Global Allantoin Market was valued at USD 461.7 million in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 805.6 million by 2035.

Market expansion is shaped by rising demand for multifunctional skin-conditioning ingredients used across cosmetic, personal care, and topical therapeutic formulations. Allantoin, available in plant-derived and synthetic forms, is widely valued for its skin-soothing, moisturizing, and renewal-supporting properties, which make it suitable for formulations targeting dryness, irritation, and surface-level skin damage. Regulatory recognition has further strengthened confidence among manufacturers, as allantoin is classified as safe and effective for over-the-counter topical protectants within regulated concentration limits. Growth is also supported by the broader movement toward cleaner formulations, plant-forward ingredient sourcing, and evolving production technologies that support consistent quality and formulation stability. Regulatory pressure on certain synthetic compounds has accelerated the transition toward safer and well-established actives, increasing the adoption of ingredients with a strong safety and performance profile. These factors collectively reinforce allantoin's role as a staple ingredient across modern skincare and therapeutic product development.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $461.7 Million |

| Forecast Value | $805.6 Million |

| CAGR | 5.7% |

The pure allantoin segment held 89.8% share in 2025 and is expected to grow at a CAGR of 5.6% through 2035. Its consistent performance, formulation stability, and compatibility with a wide range of products support strong uptake across clinical-grade and clean-label formulations.

The cosmetics and personal care application segment accounted for a 59.5% share in 2025 and is forecast to grow at a CAGR of 5.4% from 2026 to 2035. Broad adoption across skincare, grooming, and haircare products continues to drive demand due to allantoin's multifunctional benefits.

Europe Allantoin Market generated USD 155.1 million in 2025. Strong manufacturing standards established pharmaceutical capabilities, and high demand for premium formulations supports regional performance, despite comparatively slower economic expansion.

Key companies active in the Global Allantoin Market include Merck KGaA, BASF SE, DSM-Firmenich, Ashland Inc., Clariant AG, Alfa Aesar, Akema S.r.l., Innospec Inc., Allan Chemical Corporation, Rita Corporation, Jeen International Corporation, Zhejiang NHU Co., Ltd., Yongan Pharmaceutical Co., Ltd., SinoLion Chemical Co., Ltd., Shandong Xinhua Pharmaceutical Co., Ltd., Hubei Guanhao Biological Technology Co., Ltd., Luotian Guanghui Chemical Co., Ltd., Suzhou-Chem Inc., Zhanjiang Dongjian Chemicals Co., Ltd., and Luvena S.A. Companies operating in the Global Allantoin Market are strengthening their market position by focusing on high-purity production, consistent quality assurance, and compliance with global cosmetic and pharmaceutical regulations. Many players are investing in cleaner manufacturing processes and traceable sourcing to align with the rising demand for transparent and sustainable ingredients. Strategic partnerships with cosmetic formulators and OTC product manufacturers help secure long-term supply agreements and expand application reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Source

- 2.2.4 Grade

- 2.2.5 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Pure Allantoin

- 5.3 ALCLOXA (Allantoin + Aluminum Chlorohydroxide)

- 5.4 ALDIOXA (Allantoin + Aluminum Dihydroxyallantoinate)

- 5.5 ALPANTHA (Allantoin + D-Panthenol)

- 5.6 Other Derivatives

Chapter 6 Market Estimates and Forecast, By Source, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Synthetic

- 6.3 Natural/Botanical

Chapter 7 Market Estimates and Forecast, By Grade, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 USP/EP (Pharmaceutical)

- 7.3 CTFA (Cosmetic Grade)

- 7.4 Technical Grade

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Cosmetics/Personal Care

- 8.2.1 Skin Care Creams & Lotions

- 8.2.2 Anti-aging Products

- 8.2.3 Acne Treatments

- 8.2.4 Sunscreens

- 8.2.5 Shaving Products

- 8.2.6 Hair Care Products

- 8.2.7 Lip Care & Balms

- 8.2.8 Baby Care Products

- 8.3 Pharmaceutical

- 8.3.1 Wound Healing Ointments

- 8.3.2 Burn Treatment Products

- 8.3.3 Hemorrhoid Creams

- 8.3.4 Topical Anti-inflammatory Gels

- 8.3.5 Prescription Dermatology Products

- 8.3.6 Scar Recovery Products

- 8.4 Oral Hygiene

- 8.4.1 Toothpastes

- 8.4.2 Mouthwashes

- 8.4.3 Gum Healing Products

- 8.4.4 Sensitive Teeth Formulations

- 8.5 Agricultural

- 8.5.1 Plant Growth Promoters

- 8.5.2 Soil Conditioners

- 8.5.3 Crop Protection Sprays

- 8.5.4 Bio-Stimulants

- 8.6 Others

- 8.6.1 Pet Care Products

- 8.6.2 Industrial Skin Protection Creams

- 8.6.3 Toiletries & Hygiene Wipes

- 8.6.4 Sanitizing Creams

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 BASF SE

- 10.2 Akema S.r.l.

- 10.3 Alfa Aesar

- 10.4 Allan Chemical Corporation

- 10.5 Ashland Inc.

- 10.6 Clariant AG

- 10.7 DSM-Firmenich

- 10.8 Hubei Guanhao Biological Technology Co., Ltd.

- 10.9 Innospec Inc.

- 10.10 Jeen International Corporation

- 10.11 Luotian Guanghui Chemical Co., Ltd.

- 10.12 Luvena S.A.

- 10.13 Merck KGaA

- 10.14 Rita Corporation

- 10.15 Shandong Xinhua Pharmaceutical Co., Ltd.

- 10.16 SinoLion Chemical Co., Ltd.

- 10.17 Suzhou-Chem Inc.

- 10.18 Yongan Pharmaceutical Co., Ltd.

- 10.19 Zhanjiang Dongjian Chemicals Co., Ltd.

- 10.20 Zhejiang NHU Co., Ltd.

- 10.21 Others

尿囊素市場報告:趨勢、預測和競爭分析(至2031年)

尿囊素市場報告:趨勢、預測和競爭分析(至2031年) 尿囊素市場按最終用途產業、形式、來源、功能和分銷管道分類-2025-2032 年全球預測

尿囊素市場按最終用途產業、形式、來源、功能和分銷管道分類-2025-2032 年全球預測 全球尿囊素市場規模研究與預測,按應用、來源、純度、形式、等級和區域預測 2025-2035

全球尿囊素市場規模研究與預測,按應用、來源、純度、形式、等級和區域預測 2025-2035