|

市場調查報告書

商品編碼

1892813

獸用縫合線市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Veterinary Sutures Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

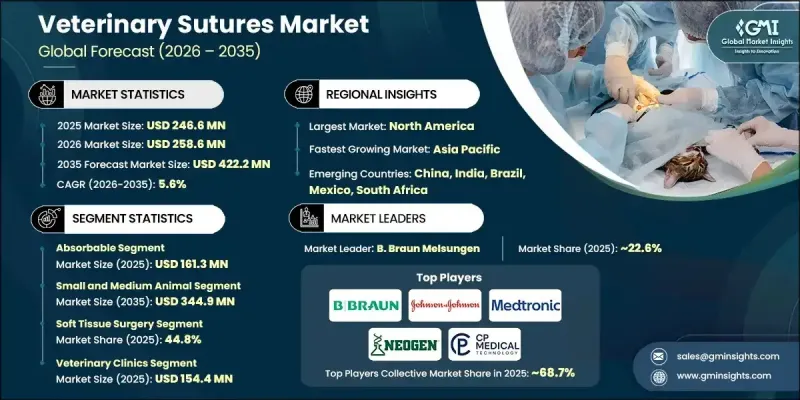

2025 年全球獸用縫線市場價值為 2.466 億美元,預計到 2035 年將以 5.6% 的複合年成長率成長至 4.222 億美元。

寵物數量的成長以及動物慢性病和生活方式相關疾病的日益普遍推動了市場的發展。隨著寵物越來越被視為家庭成員,人們對包括外科手術在內的先進獸醫護理的需求激增。獸用縫合線是獸醫用於閉合傷口和固定手術切口的關鍵醫療工具,確保傷口癒合。縫合材料的創新降低了感染風險,促進了組織修復,從而改善了臨床療效,推動了市場的發展。已開發地區和新興地區獸醫醫院和診所的擴張提高了人們獲得外科手術服務的便利性。縫合線分為可吸收型和不可吸收型,其設計兼顧了生物相容性、耐用性和安全性,適用於各種動物,確保有效的傷口管理和更快的康復。隨著動物健康意識的提高,全球先進獸用縫線的應用持續成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 2.466億美元 |

| 預測值 | 4.222億美元 |

| 複合年成長率 | 5.6% |

可吸收縫線市佔率高達65.4%,預計2025年市場規模將達1.613億美元。可吸收縫合線,包括聚乙醇酸、聚乳酸等類型,因其無需拆線而備受青睞,減少了後續復診的次數。它們在軟組織手術、常規傷口縫合和內科手術中的廣泛應用,使其佔據市場主導地位,深受獸醫和寵物主人的青睞。

預計2035年,中小動物市場規模將達到3.449億美元。推動該市場成長的因素包括犬、貓及其他中小寵物數量的不斷增加,以及寵物主人願意投資先進的獸醫護理。這些動物需要接受各種外科手術,從常規手術到複雜手術,因此對各種縫線的需求持續強勁。

預計2025年,北美獸用縫線市場將佔據39.7%的最大佔有率。該地區市場成長的主要驅動力是龐大的寵物數量、較高的動物健康意識以及完善的獸醫醫療基礎設施。寵物保險的日益普及也促進了市場擴張,使寵物主人能夠投入更多資金用於高品質的外科手術治療。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 產業影響因素

- 成長促進因素

- 寵物飼養和寵物擬人化趨勢日益成長

- 發展中國家牲畜數量不斷增加

- 縫合材料的進展

- 醫療保健支出不斷成長

- 產業陷阱與挑戰

- 高級縫合線成本高昂

- 新興市場意識有限

- 市場機遇

- 對微創和先進外科技術的需求不斷成長

- 寵物保險的普及率不斷提高

- 成長促進因素

- 成長潛力分析

- 監管環境

- 技術格局

- 當前技術趨勢

- 新興技術

- 全球動物族群統計數據

- 寵物數量統計數據

- 狗

- 貓

- 牲畜數量統計數據

- 寵物數量統計數據

- 未來市場趨勢

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 亞太地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依產品類型分類,2022-2035年

- 可吸收縫線

- 聚乙醇酸縫線

- 聚乳酸縫線

- 其他可吸收縫合線

- 不可吸收縫線

- 尼龍縫線

- 聚酯縫線

- 其他不可吸收縫合線

第6章:市場估計與預測:依動物類型分類,2022-2035年

- 小型和中型動物

- 大型動物

第7章:市場估算與預測:依應用領域分類,2022-2035年

- 軟組織手術

- 骨科手術

- 牙科手術

- 眼科手術

- 其他應用

第8章:市場估算與預測:依最終用途分類,2022-2035年

- 獸醫診所

- 獸醫院

- 研究中心和學術界

第9章:市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- AIP Medical

- B. Braun Melsungen

- Cencora

- CP Medical

- DemeTECH Corporation

- Dolphin Sutures

- Johnson & Johnson

- KATSAN

- Lotus Surgicals

- Medtronic

- Neogen Corporation

- Orion Sutures

- SMI

- Vetersut

- Vitrex medical

The Global Veterinary Sutures Market was valued at USD 246.6 million in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 422.2 million by 2035.

The market is driven by the rising pet population and the growing prevalence of chronic and lifestyle-related conditions among animals. With pets increasingly regarded as family members, demand for advanced veterinary care, including surgical procedures, has surged. Veterinary sutures are critical medical tools used by veterinarians to close wounds and secure surgical incisions, ensuring proper healing. The market benefits from innovations in suture materials that reduce infection risks and enhance tissue repair, improving clinical outcomes. Expansion of veterinary hospitals and clinics across both developed and emerging regions has improved access to surgical care. Sutures, available in absorbable and non-absorbable forms, are designed for biocompatibility, durability, and safety across species, ensuring effective wound management and faster recovery. As animal healthcare awareness grows, adoption of advanced veterinary sutures continues to rise globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $246.6 Million |

| Forecast Value | $422.2 Million |

| CAGR | 5.6% |

The absorbable sutures segment held a 65.4% share, valued at USD 161.3 million in 2025. Absorbable sutures, including polyglycolic acid, polyglactin, and other types, are favored for convenience since they do not require removal, reducing the need for follow-up visits. Their broad applicability across soft tissue surgeries, routine wound closures, and internal procedures contributes to their dominance, making them highly preferred by veterinarians and pet owners.

The small and medium animal segment is projected to reach USD 344.9 million by 2035. Growth in this segment is fueled by the increasing population of dogs, cats, and other small to medium pets, along with pet owners' willingness to invest in advanced veterinary care. These animals undergo a variety of surgical procedures, from routine operations to complex interventions, creating consistent demand for diverse suture types.

North America Veterinary Sutures Market held the largest share of 39.7% in 2025. Market growth in the region is driven by a substantial pet population, strong awareness of animal health, and a well-established veterinary care infrastructure. The rising adoption of pet insurance also supports market expansion by enabling owners to invest more in quality surgical care.

Key companies active in the Global Veterinary Sutures Market include B. Braun Melsungen, Vetersut, CP Medical, Medtronic, Orion Sutures, AIP Medical, Vitrex Medical, SMI, DemeTECH Corporation, Dolphin Sutures, Johnson & Johnson, Cencora, Lotus Surgicals, and KATSAN. Companies in the Veterinary Sutures Market are leveraging multiple strategies to strengthen their market presence. They are focusing on research and development to create advanced, biocompatible, and infection-resistant suture materials. Strategic collaborations with veterinary hospitals and clinics enhance product adoption. Expanding distribution networks across emerging and developed regions ensures wider reach and accessibility. Many firms are also adopting digital marketing and e-commerce platforms to target pet owners and veterinary professionals directly. In addition, companies are investing in training programs for veterinarians to promote optimal suture usage, while mergers, acquisitions, and partnerships are employed to increase market share and accelerate entry into new regions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Animal type trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing pet ownership and pet humanization trend

- 3.2.1.2 Rising livestock population in developing countries

- 3.2.1.3 Advancements in suture materials

- 3.2.1.4 Growing healthcare expenditure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced sutures

- 3.2.2.2 Limited awareness in emerging markets

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for minimally invasive and advanced surgical techniques

- 3.2.3.2 Growing adoption of pet insurance

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Global animal population statistics

- 3.6.1 Pet population statistics

- 3.6.1.1 Dogs

- 3.6.1.2 Cats

- 3.6.2 Livestock population statistics

- 3.6.1 Pet population statistics

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Absorbable sutures

- 5.2.1 Polyglycolic acid suture

- 5.2.2 Polyglactin suture

- 5.2.3 Other absorbable sutures

- 5.3 Non-absorbable sutures

- 5.3.1 Nylon suture

- 5.3.2 Polyester suture

- 5.3.3 Other non-absorbable sutures

Chapter 6 Market Estimates and Forecast, By Animal Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Small and medium animals

- 6.3 Large animals

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Soft tissue surgery

- 7.3 Orthopedic surgery

- 7.4 Dental surgery

- 7.5 Ophthalmic surgery

- 7.6 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Veterinary clinics

- 8.3 Veterinary hospitals

- 8.4 Research centers and academia

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AIP Medical

- 10.2 B. Braun Melsungen

- 10.3 Cencora

- 10.4 CP Medical

- 10.5 DemeTECH Corporation

- 10.6 Dolphin Sutures

- 10.7 Johnson & Johnson

- 10.8 KATSAN

- 10.9 Lotus Surgicals

- 10.10 Medtronic

- 10.11 Neogen Corporation

- 10.12 Orion Sutures

- 10.13 SMI

- 10.14 Vetersut

- 10.15 Vitrex medical

獸用護膚產品市場規模、佔有率和成長分析:按產品類型、動物種類、成分類型、應用領域、配銷通路和地區分類-2026-2033年產業預測

獸用護膚產品市場規模、佔有率和成長分析:按產品類型、動物種類、成分類型、應用領域、配銷通路和地區分類-2026-2033年產業預測 施馬倫貝格病毒治療市場 - 全球產業規模、佔有率、趨勢、機會及預測(按治療類型、動物類型、地區和競爭格局分類,2021-2031年)

施馬倫貝格病毒治療市場 - 全球產業規模、佔有率、趨勢、機會及預測(按治療類型、動物類型、地區和競爭格局分類,2021-2031年) 馬關節護理產品市場按產品類型、成分類型、給藥途徑、作用機制、馬匹生命階段、目標關節、分銷管道、應用、最終用途和最終用戶分類-全球預測,2026-2032年

馬關節護理產品市場按產品類型、成分類型、給藥途徑、作用機制、馬匹生命階段、目標關節、分銷管道、應用、最終用途和最終用戶分類-全球預測,2026-2032年 日本獸醫保健市場報告(按產品(治療、診斷)、動物類型(犬貓、馬、反芻動物、豬、家禽及其他)和地區分類,2026-2034年)

日本獸醫保健市場報告(按產品(治療、診斷)、動物類型(犬貓、馬、反芻動物、豬、家禽及其他)和地區分類,2026-2034年) 美國獸醫市場規模、佔有率和趨勢分析報告:按類型、性別和細分市場預測,2025-2033年

美國獸醫市場規模、佔有率和趨勢分析報告:按類型、性別和細分市場預測,2025-2033年 獸醫護理市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察,以及2024年至2032年的預測

獸醫護理市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察,以及2024年至2032年的預測 動物保健:全球市場佔有率和排名、總收入和需求預測(2025-2031年)獸用護膚產品:全球市場佔有率及排名、總收入及需求預測(2025-2031年)獸用調味藥品:全球市場佔有率和排名、總銷售額和需求預測(2025-2031 年)動物血庫市場規模、佔有率和趨勢分析報告:按產品、類別、類型、最終用途、地區和細分市場預測(2025-2033 年)

動物保健:全球市場佔有率和排名、總收入和需求預測(2025-2031年)獸用護膚產品:全球市場佔有率及排名、總收入及需求預測(2025-2031年)獸用調味藥品:全球市場佔有率和排名、總銷售額和需求預測(2025-2031 年)動物血庫市場規模、佔有率和趨勢分析報告:按產品、類別、類型、最終用途、地區和細分市場預測(2025-2033 年)