|

市場調查報告書

商品編碼

1892799

乙氧基化物市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Ethoxylates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

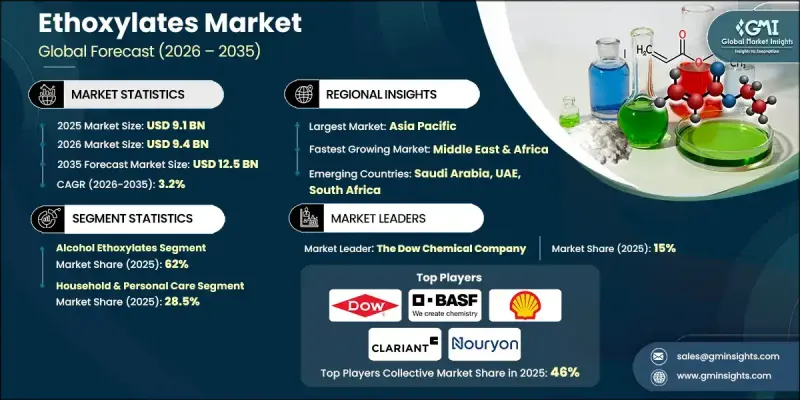

2025 年全球乙氧基化物市場價值為 91 億美元,預計到 2035 年將以 3.2% 的複合年成長率成長至 125 億美元。

乙氧基化物產業在廣泛的工業和消費應用領域中發揮關鍵作用。市場評估包括生產趨勢、定價模式、區域消費以及多個產品系列和應用領域的需求。其成長與個人護理、農業化學品和工業製造業的擴張密切相關,並得益於更廣泛的化學工業的創新。由於亞太、北美和歐洲擁有成熟的化學品製造基地、農業活動和強大的消費品產業,其分銷高度集中於這些地區。中東、非洲和拉丁美洲等新興市場也為成長做出了貢獻,因為當地生產規模的擴大以滿足不斷成長的消費需求,並逐步實現全球供應和消費的多元化。醇類乙氧基化物因其性能高效、符合法規要求和成本優勢而佔據主導地位,而特種級產品則因其技術規格而享有更高的價格。

| 市場範圍 | |

|---|---|

| 起始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 91億美元 |

| 預測值 | 125億美元 |

| 複合年成長率 | 3.2% |

2025年,醇類乙氧基化物市佔率達到62%,預計2035年將以2.7%的複合年成長率成長。由於其優異的乳化和洗滌性能,醇類乙氧基化物是大多數清潔和個人護理配方中的關鍵成分。脂肪胺類乙氧基化物在農業化學品應用中仍然至關重要,可增強農藥的擴散和滲透。此外,甲酯類乙氧基化物正逐漸成為一種永續的替代品,兼具溫和的性質(適用於化妝品和工業用途)和生態優勢。

預計到2025年,家用和個人護理應用領域將佔據28.5%的市場佔有率,並預計2026年至2035年將以2.6%的複合年成長率成長。乙氧基化物對於洗髮精、潔面乳和護膚品的乳化、清潔和配方穩定性至關重要。在農業化學品領域,乙氧基化物作為潤濕劑,可提高精準農業中農藥的功效。在上游油氣領域,它們被用作鑽井液添加劑和去乳化劑,從而提高萃取過程的運作可靠性。

預計到2025年,北美乙氧基化物市場將佔據19.7%的佔有率,並正快速成長。先進的化學品製造能力和嚴格的永續發展法規使該地區成為戰略成長中心。對環保配方和特種化學品創新產品的需求,為面向工業應用的高性能乙氧基化物提供了發展機會。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 對環保表面活性劑的需求不斷成長

- 消費者偏好轉變

- 品牌永續發展承諾

- 產業陷阱與挑戰

- 關於APE/NPE的環境問題

- 水生毒性

- 市場機遇

- 生物基乙氧基化物市場擴張

- 特種乙氧基化物開發

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依產品分類,2022-2035年

- 醇醚

- 天然醇乙氧基化物

- 合成醇乙氧基化物

- 線性醇乙氧基化物(LAE)

- 支鏈醇乙氧基化物(BAE)

- 脂肪胺乙氧基化物

- 脂肪酸乙氧基化物

- 甲基酯乙氧基化物(MEE)

- 甘油酯乙氧基化物

- 烷基酚聚氧乙烯醚(APEs)

- 壬基酚聚氧乙烯醚(NPEs)

- 辛基酚聚氧乙烯醚(OPEs)

- 其他

- 碳酸酯乙氧基化物(CO2基)

- 酵素法生成的乙氧基化物

- 高純度藥用級乙氧基化物

第6章:市場估算與預測:依應用領域分類,2022-2035年

- 居家及個人護理

- 洗衣液和洗碗液

- 工業及機構清潔

- 個人護理

- 農業化學品

- 除草劑

- 殺菌劑

- 殺蟲劑

- 肥料和微量元素

- 石油和天然氣

- 提高石油採收率(EOR)

- 消泡劑和潤濕劑

- 潤滑劑和乳化劑

- 破乳作用

- 製藥

- 藥物溶解與遞送

- 生物製劑和生物相似藥

- 輔料和乳化劑

- 醫療器械滅菌(環氧乙烷相關)

- 紡織加工

- 擦洗和潤濕

- 染色和整理

- 油漆和塗料

- 乳液聚合

- 潤濕劑和分散劑

- 保護塗層

- 建築塗料

- 工業塗料

- 紙漿和造紙

- 脫墨劑

- 分散劑

- 消泡劑

- 皮革加工

- 其他

第7章:市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第8章:公司簡介

- BASF SE

- Royal Dutch Shell PLC

- The Dow Chemical Company

- Clariant AG

- Nouryon

- Huntsman International LLC

- Sasol Limited

- Stepan Company

- Evonik Industries AG

- Solvay SA

- INEOS Group Limited

- Croda International PLC

- Arkema SA

- SABIC (Saudi Basic Industries Corporation)

The Global Ethoxylates Market was valued at USD 9.1 billion in 2025 and is estimated to grow at a CAGR of 3.2% to reach USD 12.5 billion by 2035.

The ethoxylates industry plays a pivotal role across a wide range of industrial and consumer applications. Market evaluation includes production trends, pricing patterns, regional consumption, and demand across multiple product families and applications. Growth is closely aligned with the expansion of personal care, agrochemical, and industrial manufacturing sectors, underpinned by innovations in the broader chemicals industry. Distribution is highly concentrated in Asia-Pacific, North America, and Europe due to established chemical manufacturing bases, agricultural activity, and robust consumer goods industries. Emerging markets in the Middle East, Africa, and Latin America are contributing to growth as domestic production scales up to meet increasing consumer demand, gradually diversifying global supply and consumption. Alcohol ethoxylates dominate due to performance efficiency, regulatory compliance, and cost advantages, while specialty grades command premium pricing for technical specifications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.1 Billion |

| Forecast Value | $12.5 Billion |

| CAGR | 3.2% |

The alcohol ethoxylates segment held a 62% share in 2025 and is projected to grow at a CAGR of 2.7% through 2035. They serve as key ingredients in most cleaning and personal care formulations due to their excellent emulsifying and detergent properties. Fatty amine ethoxylates remain essential in agrochemical applications for enhancing pesticide spreading and penetration. Additionally, methyl ester ethoxylates are emerging as a sustainable alternative, combining mildness for cosmetic and industrial uses with ecological advantages.

The household and personal care applications segment held a 28.5% share in 2025, with expected growth at a CAGR of 2.6% from 2026 to 2035. Ethoxylates are critical for emulsification, cleansing, and formulation stability in shampoos, cleansers, and skincare products. In agrochemicals, ethoxylates act as wetting agents that improve pesticide efficacy in precision farming. In upstream oil and gas, they are utilized as additives in drilling fluids and demulsifiers, enhancing operational reliability in extraction processes.

North America Ethoxylates Market accounted for a 19.7% share in 2025 and is expanding rapidly. Advanced chemical manufacturing capabilities and strong sustainability regulations make the region a strategic growth hub. Demand for environmentally compliant formulations and specialty chemical innovations provides opportunities for high-performance ethoxylates targeting industrial applications.

Key players in the Global Ethoxylates Market include BASF SE, Arkema SA, Croda International PLC, INEOS Group Limited, Clariant AG, The Dow Chemical Company, Evonik Industries AG, Huntsman International LLC, Nouryon, Royal Dutch Shell PLC, Sasol Limited, Solvay SA, and Stepan Company. Companies in the Global Ethoxylates Market are strengthening their position through multiple strategies. They are investing in research and development to create high-performance and sustainable formulations, expanding production facilities in strategic regions to reduce lead times, and diversifying product portfolios to meet sector-specific needs. Partnerships with end-user industries and distributors enhance market reach, while a focus on regulatory compliance and eco-friendly innovations ensures long-term competitiveness. Firms are also leveraging digitalization and advanced analytics for supply chain optimization and cost efficiency, ensuring timely delivery and improved customer satisfaction across industrial and consumer segments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Application

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for eco-friendly surfactants

- 3.2.1.2 Consumer preference shift

- 3.2.1.3 Brand sustainability commitments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Environmental concerns regarding APEs/NPEs

- 3.2.2.2 Aquatic toxicity

- 3.2.3 Market opportunities

- 3.2.3.1 Bio-based ethoxylates market expansion

- 3.2.3.2 Specialty ethoxylates development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Alcohol ethoxylates

- 5.2.1 Natural alcohol ethoxylates

- 5.2.2 Synthetic alcohol ethoxylates

- 5.2.3 Linear alcohol ethoxylates (LAE)

- 5.2.4 Branched alcohol ethoxylates (BAE)

- 5.3 Fatty amine ethoxylates

- 5.4 Fatty acid ethoxylates

- 5.5 Methyl ester ethoxylates (MEE)

- 5.6 Glyceride ethoxylates

- 5.7 Alkylphenol ethoxylates (APEs)

- 5.7.1 Nonylphenol ethoxylates (NPEs)

- 5.7.2 Octylphenol ethoxylates (OPEs)

- 5.8 Others

- 5.8.1 Carbonate ethoxylates (CO2-based)

- 5.8.2 Enzymatically produced ethoxylates

- 5.8.3 High-Purity pharmaceutical-grade ethoxylates

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Household & personal care

- 6.2.1 Laundry & dishwashing detergent

- 6.2.2 Industrial & institutional cleaning

- 6.2.3 Personal care

- 6.3 Agrochemicals

- 6.3.1 Herbicides

- 6.3.2 Fungicides

- 6.3.3 Insecticides

- 6.3.4 Fertilizers & micronutrients

- 6.4 Oil & gas

- 6.4.1 Enhanced oil recovery (EOR)

- 6.4.2 Foam control & wetting agents

- 6.4.3 Lubricants & emulsifiers

- 6.4.4 Demulsification

- 6.5 Pharmaceuticals

- 6.5.1 Drug solubilization & delivery

- 6.5.2 Biologics & biosimilars

- 6.5.3 Excipients & emulsifiers

- 6.5.4 Medical device sterilization (EtO-related)

- 6.6 Textile processing

- 6.6.1 Scouring & wetting

- 6.6.2 Dyeing & finishing

- 6.7 Paints & coatings

- 6.7.1 Emulsion polymerization

- 6.7.2 Wetting & dispersing agents

- 6.7.3 Protective coatings

- 6.7.4 Architectural coatings

- 6.7.5 Industrial coatings

- 6.8 Pulp & paper

- 6.8.1 Deinking agents

- 6.8.2 Dispersing agents

- 6.8.3 Defoamers

- 6.9 Leather processing

- 6.10 Others

Chapter 7 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 BASF SE

- 8.2 Royal Dutch Shell PLC

- 8.3 The Dow Chemical Company

- 8.4 Clariant AG

- 8.5 Nouryon

- 8.6 Huntsman International LLC

- 8.7 Sasol Limited

- 8.8 Stepan Company

- 8.9 Evonik Industries AG

- 8.10 Solvay SA

- 8.11 INEOS Group Limited

- 8.12 Croda International PLC

- 8.13 Arkema SA

- 8.14 SABIC (Saudi Basic Industries Corporation)

2026年全球乙氧基化物市場報告2026年窄譜乙氧基化物全球市場報告

2026年全球乙氧基化物市場報告2026年窄譜乙氧基化物全球市場報告 乙氧基化物市場(依產品類型、應用、最終用途產業、通路和形式)-2025-2032 年全球預測甲基酯乙氧基化物市場按應用、最終用途產業、產品類型、形式、烷基鍊長度和乙氧基化度分類-全球預測,2025-2032年

乙氧基化物市場(依產品類型、應用、最終用途產業、通路和形式)-2025-2032 年全球預測甲基酯乙氧基化物市場按應用、最終用途產業、產品類型、形式、烷基鍊長度和乙氧基化度分類-全球預測,2025-2032年 窄譜乙氧基化物市場-全球產業規模、佔有率、趨勢、機會和預測,按來源(天然和合成)、按應用(商業、住宅、工業)、按地區和競爭細分,2020-2030 年

窄譜乙氧基化物市場-全球產業規模、佔有率、趨勢、機會和預測,按來源(天然和合成)、按應用(商業、住宅、工業)、按地區和競爭細分,2020-2030 年 2025-2033 年乙氧基化物市場報告(按產品、應用和地區)乙氧基化物市場-全球產業規模、佔有率、趨勢、機會與預測,按類型、最終用戶、地區和競爭情況細分,2020-2030 年

2025-2033 年乙氧基化物市場報告(按產品、應用和地區)乙氧基化物市場-全球產業規模、佔有率、趨勢、機會與預測,按類型、最終用戶、地區和競爭情況細分,2020-2030 年 乙氧基化物的全球市場 (~2035年):類型·分子量·各用途

乙氧基化物的全球市場 (~2035年):類型·分子量·各用途 全球窄頻乙氧基化物市場

全球窄頻乙氧基化物市場 全球乙氧基化物市場需求及預測分析(2018-2034)

全球乙氧基化物市場需求及預測分析(2018-2034)