|

市場調查報告書

商品編碼

1892763

植物固醇市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Phytosterols Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

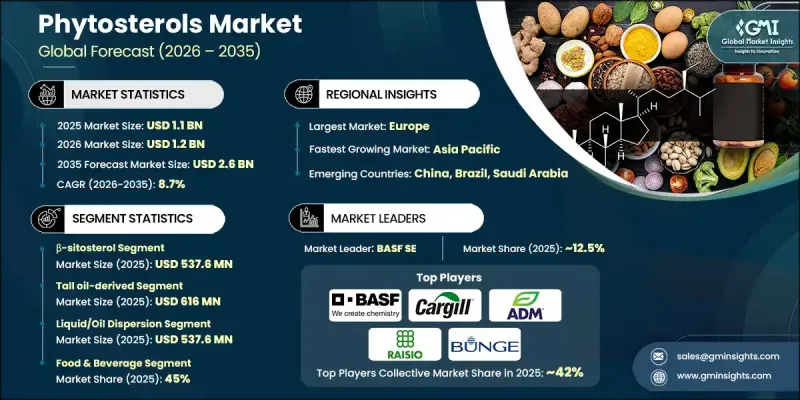

2025 年全球植物固醇市場價值為 11 億美元,預計到 2035 年將以 8.7% 的複合年成長率成長至 26 億美元。

市場成長得益於消費者對支持心血管健康和預防性營養的植物性生物活性成分需求的不斷成長。植物固醇是天然存在的植物化合物,其結構與膽固醇相似,並因其能夠限制消化系統對膽固醇的吸收而廣為人知。消費者對心臟健康的日益關注,以及功能性食品、膳食補充劑和藥品製劑的滲透率不斷提高,並持續推動市場需求的成長。萃取、純化和製劑技術的不斷進步顯著提高了產品的純度、穩定性和吸收效率。先進的加工方法使得植物固醇更廣泛地應用於各種食品和保健產品中,同時確保符合監管要求並維持穩定的品質。改良的製劑技術也有助於克服溶解性難題,從而促進其在食品、營養保健品和藥品供應鏈中的更廣泛應用。總而言之,這些發展使植物固醇成為符合長期健康發展趨勢的高價值成分。

| 市場範圍 | |

|---|---|

| 起始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 11億美元 |

| 預測值 | 26億美元 |

| 複合年成長率 | 8.7% |

2025年,BETA-谷甾醇市場規模預計將達5.376億美元。其強大的市場地位得益於其廣泛的植物來源、大規模生產的經濟效益以及公認的降膽固醇功效。 BETA-谷甾醇在食品、醫藥和營養保健品領域的廣泛應用也持續推動市場需求的穩定成長。

到 2025 年,妥爾油衍生的植物固醇市場規模將達到 6.16 億美元。其領先地位的促進因素是成本效益、可靠的原料供應以及與成熟的工業加工基礎設施的整合,從而支持高純度甾醇成分的穩定生產。

2025年,美國植物固醇市場規模將達2.452億美元。消費者對心血管健康的強烈關注、成熟的功能性食品產業以及先進的膳食補充劑生產能力,將繼續支撐對符合嚴格監管標準的高品質植物固醇成分的持續需求。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 產業陷阱與挑戰

- 市場機遇

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按甾醇類型

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依固醇類型分類,2022-2035年

- BETA-谷甾醇

- 菜油甾醇

- 豆甾醇

- BETA-谷甾醇

- 菜油甾醇

- 蕓薹甾醇

- 岩藻甾醇

- 其他

第6章:市場估算與預測:依來源分類,2022-2035年

- 妥爾油衍生品

- 大豆衍生

- 向日葵衍生

- 油菜籽/芥花籽油衍生品

- 米糠衍生

- 其他植物來源

第7章:市場估算與預測:以實物形式分類,2022-2035年

- 液體/油分散體

- 粉末/晶體

- 微膠囊化

- 乳液

- 微米級/奈米級

第8章:市場估算與預測:依應用領域分類,2022-2035年

- 餐飲

- 塗抹醬和人造奶油

- 乳製品

- 飲料

- 烘焙產品

- 零食棒和糖果

- 其他

- 製藥

- 膽固醇管理

- 動脈粥狀硬化預防

- 良性攝護腺增生治療

- 抗發炎療法

- 癌症預防及輔助治療

- 代謝症候群管理

- 營養保健品和膳食補充劑

- 化妝品及個人護理

- 保濕霜和乳霜

- 抗衰老配方

- 保養

- 護髮產品

- 唇部護理

- 防曬護理

- 其他

- 動物營養與獸醫

第9章:市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第10章:公司簡介

- ExxonMobil Corporation

- Royal Dutch Shell plc

- Chevron Corporation

- Petro-Canada/Suncor Energy

- Sonneborn LLC

- H&R Group (Hansen & Rosenthal KG)

- FUCHS Petrolub SE

- APAR Industries Limited

- Savita Oil Technologies Ltd.

- Panama Petrochem Ltd.

- Raj Petro Specialities Pvt. Ltd.

- Lodha Petro

- SEOJIN Chemical Co., Ltd.

- JX Nippon Oil & Energy Corporation

The Global Phytosterols Market was valued at USD 1.1 billion in 2025 and is estimated to grow at a CAGR of 8.7% to reach USD 2.6 billion by 2035.

Market growth is supported by rising demand for plant-based bioactive ingredients that support cardiovascular health and preventive nutrition. Phytosterols are naturally occurring plant compounds that share a structural resemblance with cholesterol and are widely recognized for their ability to limit cholesterol absorption in the digestive system. Increasing consumer focus on heart health, combined with the growing penetration of functional foods, dietary supplements, and pharmaceutical formulations, continues to strengthen market demand. Ongoing progress in extraction, purification, and formulation technologies has significantly improved product purity, stability, and absorption efficiency. Advanced processing methods have enabled broader incorporation of phytosterols into a wide range of food and wellness products while maintaining regulatory compliance and consistent quality. Improved formulation techniques have also helped overcome solubility challenges, supporting wider adoption across food, nutraceutical, and pharmaceutical supply chains. Together, these developments are positioning phytosterols as a high-value ingredient aligned with long-term health and wellness trends.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.1 Billion |

| Forecast Value | $2.6 Billion |

| CAGR | 8.7% |

The B-sitosterol segment generated USD 537.6 million in 2025. Its strong market position is supported by widespread availability from plant sources, favorable economics for large-scale production, and well-established cholesterol-lowering performance. Its broad acceptance across food, pharmaceutical, and nutraceutical applications continues to reinforce steady demand.

The tall oil-derived phytosterols segment reached USD 616 million in 2025. Their leadership is driven by cost efficiency, reliable raw material availability, and integration with established industrial processing infrastructure, supporting consistent production of high-purity sterol ingredients.

U.S. Phytosterols Market reached USD 245.2 million in 2025. Strong consumer awareness of cardiovascular health, a mature functional food sector, and advanced supplement manufacturing capabilities continue to support sustained demand for high-quality phytosterol ingredients that meet stringent regulatory standards.

Key companies operating in the Global Phytosterols Market include Cargill, Incorporated, BASF SE, Archer Daniels Midland, Wilmar International Ltd., Bunge Limited, Raisio Oyj, DuPont de Nemours / IFF, Kensing LLC, DRT (Les Derives Resiniques et Terpeniques), Vitae Naturals, Arboris LLC, Advanced Organic Materials (AOM) S.A., COFCO Biotechnology Co., Ltd., Ashland Global Holdings Inc., and Gustav Parmentier GmbH. Companies in the Global Phytosterols Market are strengthening their competitive position through investments in advanced extraction technologies, capacity expansion, and product purity enhancement. Strategic focus is placed on developing high-bioavailability formulations that align with functional food and nutraceutical trends. Partnerships with food manufacturers and supplement brands support long-term demand visibility and application-driven innovation.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Sterol Grade

- 2.2.2 Source

- 2.2.3 Physical form

- 2.2.4 Application

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By sterol type

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code)( Note: the trade statistics will be provided for key countries only)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Sterol Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Β-sitosterol

- 5.3 Campesterol

- 5.4 Stigmasterol

- 5.5 Β-sitostanol

- 5.6 Campestanol

- 5.7 Brassicasterol

- 5.8 Fucosterol

- 5.9 Others

Chapter 6 Market Estimates and Forecast, By Source, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Tall oil-derived

- 6.3 Soybean-derived

- 6.4 Sunflower-derived

- 6.5 Rapeseed/canola-derived

- 6.6 Rice bran-derived

- 6.7 Other plant sources

Chapter 7 Market Estimates and Forecast, By Physical Form, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Liquid / oil dispersion

- 7.3 Powder / crystalline

- 7.4 Microencapsulated

- 7.5 Emulsion

- 7.6 Micronized / nano-sized

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Food & beverage

- 8.2.1 Spreads & margarines

- 8.2.2 Dairy products

- 8.2.3 Beverages

- 8.2.4 Bakery products

- 8.2.5 Snack bars & confectionery

- 8.2.6 Others

- 8.3 Pharmaceuticals

- 8.3.1 Cholesterol management

- 8.3.2 Atherosclerosis prevention

- 8.3.3 BPH treatment

- 8.3.4 Anti-inflammatory therapies

- 8.3.5 Cancer prevention & adjunct therapy

- 8.3.6 Metabolic syndrome management

- 8.4 Nutraceuticals & dietary supplements

- 8.5 Cosmetics & personal care

- 8.5.1 Moisturizers & creams

- 8.5.2 Anti-aging formulations

- 8.5.3 Skin care

- 8.5.4 Hair care products

- 8.5.5 Lip care

- 8.5.6 Sun care

- 8.5.7 Others

- 8.6 Animal nutrition & veterinary

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 ExxonMobil Corporation

- 10.2 Royal Dutch Shell plc

- 10.3 Chevron Corporation

- 10.4 Petro-Canada/Suncor Energy

- 10.5 Sonneborn LLC

- 10.6 H&R Group (Hansen & Rosenthal KG)

- 10.7 FUCHS Petrolub SE

- 10.8 APAR Industries Limited

- 10.9 Savita Oil Technologies Ltd.

- 10.10 Panama Petrochem Ltd.

- 10.11 Raj Petro Specialities Pvt. Ltd.

- 10.12 Lodha Petro

- 10.13 SEOJIN Chemical Co., Ltd.

- 10.14 JX Nippon Oil & Energy Corporation

全球植物固醇市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球植物固醇市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 植物固醇市場規模、佔有率和成長分析(按成分、來源、形態、應用和地區分類)-2026-2033年產業預測全球植物固醇市場-2025-2030年預測

植物固醇市場規模、佔有率和成長分析(按成分、來源、形態、應用和地區分類)-2026-2033年產業預測全球植物固醇市場-2025-2030年預測 植物固醇市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、應用、地區和競爭細分,2020-2030 年)

植物固醇市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、應用、地區和競爭細分,2020-2030 年) 全球植物固醇市場規模、佔有率、趨勢分析報告:2025-2032 年應用、產品與地區展望與預測

全球植物固醇市場規模、佔有率、趨勢分析報告:2025-2032 年應用、產品與地區展望與預測 植物固醇的全球市場:市場規模·佔有率·趨勢,產業分析 (各類型·不同形狀·各原料·各用途·各地區),未來預測 (2025年~2034年)

植物固醇的全球市場:市場規模·佔有率·趨勢,產業分析 (各類型·不同形狀·各原料·各用途·各地區),未來預測 (2025年~2034年) 植物固醇市場分析及預測至 2033 年:類型、產品、應用、形式、最終用戶、技術、材料類型、製程、功能

植物固醇市場分析及預測至 2033 年:類型、產品、應用、形式、最終用戶、技術、材料類型、製程、功能 植物固醇的全球市場

植物固醇的全球市場