|

市場調查報告書

商品編碼

1892758

顱內動脈瘤市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Intracranial Aneurysm Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

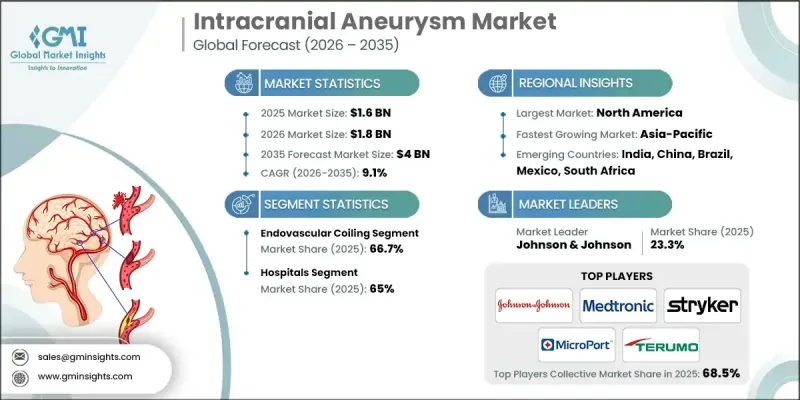

2025 年全球顱內動脈瘤市值為 16 億美元,預計到 2035 年將以 9.1% 的複合年成長率成長至 40 億美元。

微創神經血管技術的快速發展、臨床上對血管內治療而非開放性手術的日益青睞,以及全球顱內動脈瘤發生率的上升,共同推動了市場擴張。顱內動脈瘤是指因動脈壁退化而導致的腦血管局部壁薄弱和向外凸出。隨著時間的推移,這種情況會惡化,並存在破裂的嚴重風險,可能導致危及生命的顱內出血。這些動脈瘤最常發生於腦內動脈交界處附近。器械工程和手術技術的進步顯著提高了治療的精確度,縮短了手術時間,並降低了併發症發生率。隨著醫療系統越來越重視微創治療方案,現代神經介入手術在全球的應用持續成長。領先製造商不斷進行的研究計畫和持續創新正在改善患者的治療效果,並支持已開發和新興醫療系統市場的持續成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 16億美元 |

| 預測值 | 40億美元 |

| 複合年成長率 | 9.1% |

由於其微創性和良好的臨床療效,血管內栓塞術預計在2025年將佔據66.7%的市場佔有率。此技術廣泛應用於破裂和未破裂動脈瘤的治療,尤其適用於老年患者和手術風險較高的人。較短的恢復時間和較低的手術負擔使其繼續成為首選治療方案,隨著醫院推廣微創治療模式,手術量也不斷成長。

預計到2025年,醫院業務將佔市場佔有率的65%,到2035年將創造25億美元的收入。急性神經血管事件和動脈瘤併發症導致的患者入院率居高不下,推動了對住院治療的需求。醫院能夠提供專科醫生、先進影像設備和重症監護等綜合服務,從而實現對複雜動脈瘤病例的快速協調管理。

預計到2025年,北美顱內動脈瘤市佔率將達到41.7%。該地區人口老化和生活方式相關的風險因素導致疾病負擔沉重。篩檢率的提高和早期診斷的普及推動了治療需求的成長。完善的神經血管基礎設施和先進的手術能力進一步鞏固了該地區的市場領先地位。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 產業影響因素

- 成長促進因素

- 高血壓和生活型態相關疾病的發生率不斷上升

- 神經介入手術和訓練有素的專家團隊不斷壯大

- 血管內裝置的技術進步

- 提高對顱內動脈瘤的認知

- 產業陷阱與挑戰

- 設備和手術費用高昂

- 圍手術期及術後併發症及發生率的風險

- 市場機遇

- 向醫療基礎設施日益完善的新興市場擴張

- 對個人化植入物、3D列印設備和患者特定方案的需求激增

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 技術格局

- 當前技術趨勢

- 新興技術

- 報銷方案

- 消費者洞察

- 未來市場趨勢

- 價值鏈分析

- 波特的分析

- PESTEL 分析

- 差距分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 亞太地區

- 競爭定位矩陣

- 主要市場參與者的競爭分析

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依治療類型分類,2022-2035年

- 血管內栓塞術

- 手術夾

- 分流器

- 其他治療類型

第6章:市場估算與預測:依最終用途分類,2022-2035年

- 醫院

- 門診手術中心

- 其他最終用途

第7章:市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第8章:公司簡介

- B. BRAUN

- Balt Group

- INTEGRA

- Johnson & Johnson

- Medtronic

- MicroPort

- MIZUHO

- Penumbra

- Peter LAZIC

- phenox

- Shape Memory Medical

- Stryker

- TERUMO

- Wallaby Medical

- ZYLOX TONBRIDGE

The Global Intracranial Aneurysm Market was valued at USD 1.6 billion in 2025 and is estimated to grow at a CAGR of 9.1% to reach USD 4 billion by 2035.

Market expansion is driven by rapid progress in minimally invasive neurovascular technologies, a growing clinical preference for endovascular therapies over open surgical approaches, and the rising incidence of intracranial aneurysms worldwide. An intracranial aneurysm is defined as a localized weakening and outward bulging of a cerebral blood vessel caused by arterial wall degeneration. Over time, this condition can worsen and carries a serious risk of rupture, which may result in life-threatening intracranial bleeding. These aneurysms are most identified near arterial junctions within the brain. Advancements in device engineering and procedural techniques have significantly improved treatment precision, reduced intervention time, and lowered complication rates. As healthcare systems increasingly prioritize less invasive treatment pathways, adoption of modern neurointerventional procedures continues to rise globally. Ongoing research initiatives and sustained innovation by leading manufacturers are improving patient outcomes and supporting consistent market growth across developed and emerging healthcare systems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.6 Billion |

| Forecast Value | $4 Billion |

| CAGR | 9.1% |

The endovascular coiling segment held a 66.7% share in 2025 owing to its minimally invasive approach and strong clinical performance. This technique is widely favored for both ruptured and unruptured aneurysms, particularly among elderly patients and individuals with elevated surgical risk. Shorter recovery timelines and reduced procedural burden continue to support its role as a primary treatment option, with procedure volumes rising as hospitals expand minimally invasive care models.

The hospitals segment accounted for a 65% share in 2025 and is expected to generate USD 2.5 billion through 2035. High patient admissions related to acute neurovascular events and aneurysm complications are driving demand for hospital-based treatment. Hospitals provide integrated access to specialized clinicians, advanced imaging, and intensive care, enabling rapid and coordinated management of complex aneurysm cases.

North America Intracranial Aneurysm Market held a 41.7% share in 2025. The region experiences a high disease burden linked to aging populations and lifestyle-related risk factors. Increased screening rates and early diagnosis are supporting treatment demand. Well-established neurovascular infrastructure and advanced procedural capabilities further strengthen regional market leadership.

Key companies operating in the Global Intracranial Aneurysm Market include Medtronic, Stryker, TERUMO, Johnson & Johnson, Penumbra, B. BRAUN, Balt Group, MicroPort, INTEGRA, Shape Memory Medical, phenox, Wallaby Medical, ZYLOX TONBRIDGE, MIZUHO, and Peter LAZIC. Companies in the Global Intracranial Aneurysm Market are reinforcing their market position through sustained investment in research, technology refinement, and clinical validation. Manufacturers are focused on developing safer, more effective minimally invasive solutions that improve long-term patient outcomes. Strategic partnerships with hospitals and research institutions help accelerate product adoption and clinical acceptance. Geographic expansion into underserved regions supports volume growth, while regulatory approvals strengthen global reach. Many players are also investing in physician training programs and procedural education to increase familiarity with advanced treatment options.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Treatment type trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of hypertension and lifestyle-related diseases

- 3.2.1.2 Growth in neurointerventional procedures and trained specialists

- 3.2.1.3 Technological advances in endovascular devices

- 3.2.1.4 Increasing awareness about intracranial aneurysms

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of devices and procedures

- 3.2.2.2 Risk of peri- and post-procedural complications and morbidity

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into emerging markets with growing healthcare infrastructure

- 3.2.3.2 Surging need for personalized implants, 3D-printed devices, and patient-specific planning

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario

- 3.7 Consumer insights

- 3.8 Future market trends

- 3.9 Value chain analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Treatment Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Endovascular coiling

- 5.3 Surgical clipping

- 5.4 Flow diverters

- 5.5 Other treatment types

Chapter 6 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Ambulatory surgical centers

- 6.4 Other end use

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 B. BRAUN

- 8.2 Balt Group

- 8.3 INTEGRA

- 8.4 Johnson & Johnson

- 8.5 Medtronic

- 8.6 MicroPort

- 8.7 MIZUHO

- 8.8 Penumbra

- 8.9 Peter LAZIC

- 8.10 phenox

- 8.11 Shape Memory Medical

- 8.12 Stryker

- 8.13 TERUMO

- 8.14 Wallaby Medical

- 8.15 ZYLOX TONBRIDGE

顱內動脈瘤市場:2026年至2032年全球市場預測(依治療方法、動脈瘤位置、患者年齡層及最終用戶分類)

顱內動脈瘤市場:2026年至2032年全球市場預測(依治療方法、動脈瘤位置、患者年齡層及最終用戶分類) 全球顱內動脈瘤市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的考察、未來預測(2026-2034)

全球顱內動脈瘤市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的考察、未來預測(2026-2034) 顱內動脈瘤市場規模、佔有率和成長分析(按產品類型、類型、最終用戶和地區分類)—2026-2033年產業預測

顱內動脈瘤市場規模、佔有率和成長分析(按產品類型、類型、最終用戶和地區分類)—2026-2033年產業預測 2025年全球顱內動脈瘤市場報告

2025年全球顱內動脈瘤市場報告 全球顱內動脈瘤市場:市場規模、佔有率、趨勢、產業分析(依類型、最終用途和地區)、未來預測(2025-2034)顱內動脈瘤市場:2025 年至 2032 年全球產業分析、規模、佔有率、成長、趨勢與預測全球顱內動脈瘤市場 - 全球產業分析、規模、佔有率、成長、趨勢及2032年預測

全球顱內動脈瘤市場:市場規模、佔有率、趨勢、產業分析(依類型、最終用途和地區)、未來預測(2025-2034)顱內動脈瘤市場:2025 年至 2032 年全球產業分析、規模、佔有率、成長、趨勢與預測全球顱內動脈瘤市場 - 全球產業分析、規模、佔有率、成長、趨勢及2032年預測 顱內動脈瘤:市場洞察·競爭環境·市場預測 (~2030年)

顱內動脈瘤:市場洞察·競爭環境·市場預測 (~2030年)