|

市場調查報告書

商品編碼

1892745

農業感測器市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Agriculture Sensor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

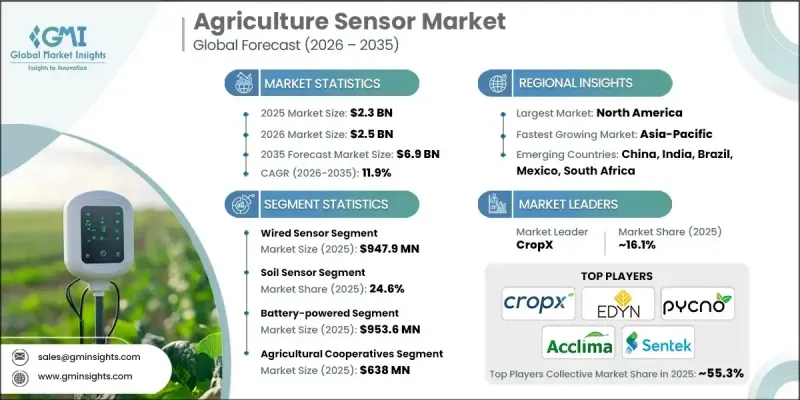

2025 年全球農業感測器市場價值為 23 億美元,預計到 2035 年將以 11.9% 的複合年成長率成長至 69 億美元。

精準農業正在改變傳統農業,從千篇一律的田間耕作方式轉向因地制宜的作物管理。隨著全球糧食需求成長和耕地日益稀缺,農民面臨著用更少的資源生產更多糧食的巨大壓力。這促使數據驅動技術得到廣泛應用,從而實現更明智的決策。

| 市場範圍 | |

|---|---|

| 起始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 23億美元 |

| 預測值 | 69億美元 |

| 複合年成長率 | 11.9% |

無線感測器市場預計在2025年將創造9.479億美元的市場規模,這主要得益於其易於部署和無需大量佈線基礎設施即可支援即時資料採集的能力。這些感測器使農民能夠遠端監測環境狀況、作物生長情況和灌溉系統,從而幫助他們更快、更明智地做出決策。隨著精準農業和物聯網技術的興起,無論是大型商業農場或小型農戶,對無線解決方案的需求都非常強勁。

預計到2025年,土壤感測器市場佔有率將達到24.6%,這主要得益於其對土壤濕度、溫度、鹽度和養分含量等關鍵資訊的精準洞察。農民依靠這些感測器來最佳化灌溉計劃、防止過度施肥並提高作物整體產量。隨著節水和永續發展成為全球農業的首要任務,土壤感測器在已開發市場和新興市場都越來越受歡迎。這些工具在面臨乾旱或土壤退化的地區尤其有價值。

2024年,北美農業感測器市佔率達34.3%。高度機械化、農場規模龐大以及對農業科技的大力投資,使該地區成為精準農業實踐的領導者。美國和加拿大的農民正擴大採用基於感測器的技術來監測土壤狀況、最佳化灌溉並實現作物管理的自動化。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 成本結構

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 精準農業和智慧農業的日益普及

- 政府補貼和政策促進數位農業

- 對永續農業實踐的需求日益成長

- 物聯網、人工智慧和無線連接在農村地區的擴展

- 全球糧食需求不斷成長,而耕地面積卻在減少

- 產業陷阱與挑戰

- 前期成本高昂,小農戶難以負擔。

- 農村經濟中有限的數位基礎設施和資料素養

- 市場機遇

- 與人工智慧、巨量資料和農場管理軟體整合

- 垂直農業和可控制環境農業的發展

- 農業無人機和機器人應用的擴展

- 開發低成本、太陽能供電的無線感測器

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興商業模式

- 合規要求

- 永續性措施

- 消費者情緒分析

- 專利和智慧財產權分析

- 地緣政治與貿易動態

第4章:競爭格局

- 公司市佔率分析簡介

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 市場集中度分析

- 主要參與者的競爭基準化分析

- 財務績效比較

- 收入

- 利潤率

- 研發

- 產品組合比較

- 產品範圍廣度

- 科技

- 創新

- 地理分佈比較

- 全球足跡分析

- 服務網路覆蓋範圍

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導人

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年主要發展動態

- 併購

- 夥伴關係與合作

- 技術進步

- 擴張和投資策略

- 永續發展計劃

- 數位轉型計劃

- 新興/新創企業競爭對手格局

第5章:市場估算與預測:依感測器類型分類,2022-2035年

- 土壤感測器

- 水感測器

- 氣候/天氣感測器

- 位置感測器

- 光學感測器

- 機械感測器

- 生物感測器

- 其他專用感測器

第6章:市場估算與預測:以連結方式分類,2022-2035年

- 有線感應器

- 無線感測器

第7章:市場估算與預測:依電源類型分類,2022-2035年

- 電池供電

- 太陽能驅動

- 混合

第8章:市場估算與預測:依最終用途分類,2022-2035年

- 農民/個體種植者

- 農業合作社

- 研究機構和大學

- 農業綜合企業

- 政府和公共機構

- 其他

第9章:市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第10章:公司簡介

- Acclima Inc.

- Acquity Agriculture

- Agsmarts Inc.

- Aker Technology Co., Ltd.

- AquaSpy Inc.

- Auroras (Auroras srl)

- Bosch Sensortec

- Caipos GmbH

- Changsha Zoko Link Technology Co., Ltd.

- CropX Inc.

- Decagon Devices (METER Group)

- dol-sensors A/S

- Honde Technology Co., Ltd.

- Hunan Rika Electronic Tech Co., Ltd.

- John Deere

- Libelium Comunicaciones Distribuidas SL

- Lindsay Corporation

- Monnit Corporation

- OMRON Electronic Components

- Pycno

- Sensaphone

- Sensoterra

- Sentek Ltd

- Teralytic

- Texas Instruments Incorporated

- Vegetronix Inc.

- Wevolver

The Global Agriculture Sensor Market was valued at USD 2.3 billion in 2025 and is estimated to grow at a CAGR of 11.9% to reach USD 6.9 billion by 2035.

Precision farming is transforming traditional agriculture by shifting from uniform field practices to site-specific crop management. As global food demand rises and arable land becomes more limited, farmers are under increasing pressure to produce more with fewer resources. This has led to the widespread adoption of data-driven technologies, enabling smarter decision-making.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.3 Billion |

| Forecast Value | $6.9 Billion |

| CAGR | 11.9% |

The wireless sensors segment generated USD 947.9 million in 2025, driven by its ease of deployment and ability to support real-time data collection without the need for extensive cabling infrastructure. These sensors enable farmers to monitor environmental conditions, crop status, and irrigation systems remotely, helping them make faster and more informed decisions. With the rise of precision farming and IoT integration, wireless solutions are in high demand across both large-scale commercial farms and smallholder operations.

The soil sensors segment held a significant share of 24.6% in 2025, driven by vital insights into soil moisture, temperature, salinity, and nutrient content. Farmers rely on these sensors to fine-tune irrigation schedules, prevent over-fertilization, and enhance overall crop productivity. As water conservation and sustainability become top priorities across global agriculture, soil sensors are gaining traction in both developed and emerging markets. These tools are especially valuable in regions facing drought or soil degradation.

North America Agriculture Sensor Market held a 34.3% share in 2024. High levels of mechanization, large farm sizes, and strong investment in agri-tech have made the region a leader in adopting precision farming practices. Farmers in the United States and Canada are increasingly integrating sensor-based technologies to monitor soil conditions, optimize irrigation, and automate crop management.

Major players in the Global Agriculture Sensor Market are Libelium Comunicaciones Distribuidas SL, Acuity Agriculture, Pycno, Caipos GmbH, dol-sensors A/S, Monnit Corporation, Wevolver, Changsha Zoko Link Technology Co., Ltd., Bosch Sensortec, Sensoterra, CropX Inc., Auroras (Auroras s.r.l.), Sensaphone, John Deere, Aker Technology Co., Ltd., Texas Instruments Incorporated, AquaSpy Inc., Sentek Ltd, Lindsay Corporation, Hunan Rika Electronic Tech Co., Ltd., Acclima Inc., Decagon Devices (METER Group), AgSmarts Inc., OMRON Electronic Components, Teralytic, Honde Technology Co., Ltd. To strengthen their position, companies in the agriculture sensor market are focusing on product innovation, affordability, and data integration. Many are investing in R&D to develop multi-functional sensors that can track multiple variables simultaneously while minimizing energy consumption. Strategic partnerships with agri-tech startups, irrigation system manufacturers, and agri-software providers are helping companies offer end-to-end solutions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Sensor Type Trends

- 2.2.2 Connectivity Trends

- 2.2.3 Power Source Trends

- 2.2.4 End use Trends

- 2.2.5 Region

- 2.3 TAM Analysis, 2025-2034 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Executive decision points

- 2.6 Critical Success Factors

- 2.7 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of precision agriculture and smart farming

- 3.2.1.2 Government subsidies & policies promoting digital agriculture

- 3.2.1.3 Growing need for sustainable farming practices

- 3.2.1.4 Expansion of IoT, AI, and wireless connectivity in rural areas

- 3.2.1.5 Rising global food demand with shrinking arable land

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High upfront costs and lack of affordability for smallholder farmers

- 3.2.2.2 Limited digital infrastructure and data literacy in rural economies

- 3.2.3 Market Opportunities

- 3.2.3.1 Integration with AI, big data, and farm management software

- 3.2.3.2 Growth of vertical farming and controlled-environment agriculture

- 3.2.3.3 Expansion of agricultural drone and robotics applications

- 3.2.3.4 Development of low-cost, solar-powered and wireless sensors

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technological and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price Trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Sustainability measures

- 3.13 Consumer sentiment analysis

- 3.14 Patent and IP analysis

- 3.15 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction Company market share analysis

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1. North America

- 4.2.2. Europe

- 4.2.3. Asia Pacific

- 4.2.2 Market concentration analysis

- 4.3 Competitive Benchmarking of key Players

- 4.3.1 Financial Performance Comparison

- 4.3.1.1. Revenue

- 4.3.1.2. Profit Margin

- 4.3.1.3. R&D

- 4.3.2 Product Portfolio Comparison

- 4.3.2.1. Product Range Breadth

- 4.3.2.2. Technology

- 4.3.2.3. Innovation

- 4.3.3 Geographic Presence Comparison

- 4.3.3.1. Global Footprint Analysis

- 4.3.3.2. Service Network Coverage

- 4.3.3.3. Market Penetration by Region

- 4.3.4 Competitive Positioning Matrix

- 4.3.4.1. Leaders

- 4.3.4.2. Challengers

- 4.3.4.3. Followers

- 4.3.4.4. Niche Players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial Performance Comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and Acquisitions

- 4.4.2 Partnerships and Collaborations

- 4.4.3 Technological Advancements

- 4.4.4 Expansion and Investment Strategies

- 4.4.5 Sustainability Initiatives

- 4.4.6 Digital Transformation Initiatives

- 4.5 Emerging/ Startup Competitors Landscape

Chapter 5 Market Estimates & Forecast, By Sensor Type, 2022 - 2035 (USD Million & Units)

- 5.1 Key trends

- 5.2 Soil sensors

- 5.3 Water sensors

- 5.4 Climate/weather sensors

- 5.5 Location sensors

- 5.6 Optical sensors

- 5.7 Mechanical sensors

- 5.8 Biosensors

- 5.9 Other specialized sensors

Chapter 6 Market estimates & forecast, By Connectivity, 2022 - 2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 Wired sensors

- 6.3 Wireless sensors

Chapter 7 Market estimates & forecast, By Power Source, 2022 - 2035 (USD Million & Units)

- 7.1 Key trends

- 7.2 Battery-powered

- 7.3 Solar-powered

- 7.4 Hybrid

Chapter 8 Market estimates & forecast, By End Use, 2022-2035 (USD Million & Units)

- 8.1 Key trends

- 8.2 Farmers/individual growers

- 8.3 Agricultural cooperatives

- 8.4 Research institutes & universities

- 8.5 Agribusiness corporations

- 8.6 Government & public agencies

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 U.K.

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East & Africa

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profile

- 10.1 Acclima Inc.

- 10.2 Acquity Agriculture

- 10.3 Agsmarts Inc.

- 10.4 Aker Technology Co., Ltd.

- 10.5 AquaSpy Inc.

- 10.6 Auroras (Auroras s.r.l.)

- 10.7 Bosch Sensortec

- 10.8 Caipos GmbH

- 10.9 Changsha Zoko Link Technology Co., Ltd.

- 10.10 CropX Inc.

- 10.11 Decagon Devices (METER Group)

- 10.12 dol-sensors A/S

- 10.13 Honde Technology Co., Ltd.

- 10.14 Hunan Rika Electronic Tech Co., Ltd.

- 10.15 John Deere

- 10.16 Libelium Comunicaciones Distribuidas SL

- 10.17 Lindsay Corporation

- 10.18 Monnit Corporation

- 10.19 OMRON Electronic Components

- 10.20 Pycno

- 10.21 Sensaphone

- 10.22 Sensoterra

- 10.23 Sentek Ltd

- 10.24 Teralytic

- 10.25 Texas Instruments Incorporated

- 10.26 Vegetronix Inc.

- 10.27 Wevolver

農業感測器市場:2026-2032年全球市場預測(按交付方式、感測器類型、連接方式、應用、最終用戶和部署模式分類)農作物掃描器市場:依技術、平台類型、應用、交付方式及最終用戶分類-2026-2032年全球市場預測

農業感測器市場:2026-2032年全球市場預測(按交付方式、感測器類型、連接方式、應用、最終用戶和部署模式分類)農作物掃描器市場:依技術、平台類型、應用、交付方式及最終用戶分類-2026-2032年全球市場預測 全球農業感測器市場:按類型、應用、連接方式、國家和地區分類-產業分析、市場規模、佔有率及未來預測(2025-2032年)

全球農業感測器市場:按類型、應用、連接方式、國家和地區分類-產業分析、市場規模、佔有率及未來預測(2025-2032年) 以半導體為基礎的害蟲偵測系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、最終用戶及功能分類

以半導體為基礎的害蟲偵測系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、最終用戶及功能分類 2026年全球農業感測器市場報告

2026年全球農業感測器市場報告 農業感測器市場按類型、應用、技術和地區分類

農業感測器市場按類型、應用、技術和地區分類 2032 年農業感測器市場預測:按感測器類型、連接性、電源、農場規模、應用和地區進行的全球分析2032 年農業感測器市場預測:按類型、農場類型、應用、最終用戶和地區進行的全球分析

2032 年農業感測器市場預測:按感測器類型、連接性、電源、農場規模、應用和地區進行的全球分析2032 年農業感測器市場預測:按類型、農場類型、應用、最終用戶和地區進行的全球分析 全球農業感測器市場

全球農業感測器市場 農業感測器市場規模、佔有率、趨勢分析報告:按類型、應用、地區、細分市場預測,2025-2030 年

農業感測器市場規模、佔有率、趨勢分析報告:按類型、應用、地區、細分市場預測,2025-2030 年