|

市場調查報告書

商品編碼

1885899

植物性海鮮配料市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Plant-Based Seafood Ingredients Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

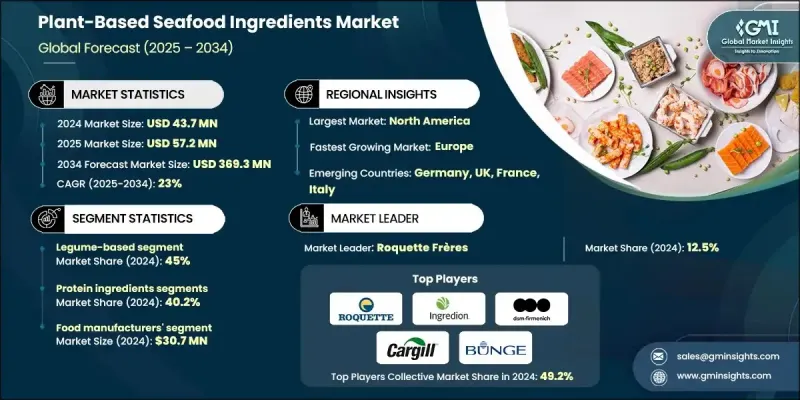

2024 年全球植物性海鮮配料市場價值為 4,370 萬美元,預計到 2034 年將以 23% 的複合年成長率成長至 3.693 億美元。

需求的激增反映了消費者對永續、符合倫理且注重健康的食品日益成長的偏好。植物性海鮮替代品因其在口味、質地和外觀上能夠高度還原傳統海鮮,同時又能解決過度捕撈、海洋污染和氣候變遷等問題而備受青睞。消費者越來越意識到植物性飲食的健康益處,包括降低膽固醇、改善心血管健康和控制體重。這些成分的主要用途是為傳統海鮮提供永續且營養豐富的替代品,以滿足不斷成長的純素食者、素食者和彈性素食者的需求。這些成分被用於生產海鮮替代品、即食食品、零食和功能性食品,使食品生產商能夠在滿足消費者感官需求的同時,減少對環境的影響。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 4370萬美元 |

| 預測值 | 3.693億美元 |

| 複合年成長率 | 23% |

由於豆類具有高蛋白質含量、用途廣泛和環境效益等優點,預計到2024年,豆類原料將佔45%的市場佔有率。大豆、豌豆和鷹嘴豆的衍生物擴大被用於模仿海鮮的口感和風味,以滿足注重健康和環保的消費者的需求。加工技術的進步正在提升它們在海鮮應用中的功能性。

預計到2024年,蛋白質配料市佔率將達到40.2%,主要集中在能夠改善營養成分和功能特性的植物性蛋白質。蛋白質萃取和加工技術的創新顯著提升了產品的口感和質地,而清潔標籤和無過敏原的趨勢也持續推動產品研發。

2024年,北美植物性海鮮配料市佔率達到42.3%,預計到2034年將以23.1%的複合年成長率成長,其中美國市場2024年的市場規模將達到1,480萬美元。該地區的成長主要受消費者健康意識的提升、對永續發展的關注以及倫理因素的考慮所驅動。植物性蛋白質萃取和發酵技術的進步使得生產出具有真實口感和質地的海鮮替代品成為可能。此外,有利的監管政策以及零售和餐飲服務業不斷湧現的新產品也進一步推動了市場成長。

植物性海鮮配料市場的主要參與者包括嘉吉公司(Cargill, Incorporated)、帝斯曼-菲美意公司(DSM-Firmenich)、英聯食品公司(Ingredion Incorporated)、邦吉有限公司(Bunge Limited)、CP Kelco(JM Huber Corporation)、羅蓋特兄弟公司(Roquette Fres)、酵母公司(Anjgel)、酵母公司(Roquette Freer)、酵母公司。 Ltd.)、瑪拉再生能源公司(Mara Renewables Corporation)、Paleo(原Miruku)、BENEO GmbH(Sudzucker集團)、FMC公司(生物聚合物事業部)、Kalys(MERIDIS集團)和Algama Foods。植物性海鮮配料市場的領導者正在採取多種策略,例如拓展產品組合、加大研發投入以改善產品質地和口感、與餐飲服務和零售品牌建立合作關係,以及利用永續性和清潔標籤等宣傳語。此外,他們還專注於地理擴張、策略合作以及蛋白質提取和發酵過程的技術創新,以增強市場佔有率,並吸引具有環保意識和健康意識的消費者。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 產業陷阱與挑戰

- 市場機遇

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按產品類別

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依來源分類,2021-2034年

- 主要趨勢

- 豆類成分

- 穀物及穀類原料

- 海藻及藻類成分

- 其他

第6章:市場估算與預測:依成分類型分類,2021-2034年

- 主要趨勢

- 蛋白質成分

- 豌豆蛋白

- 大豆蛋白

- 小麥麩質

- 水膠體和質地改良劑

- 卡拉膠

- 海藻酸鹽

- 瓊脂

- 蒟蒻葡甘露聚醣

- 其他水膠體

- 調味成分

- 酵母萃取物

- 海藻調味料和萃取物

- 蔬菜鮮味與天然香料

- 油脂

- 藻油(ω-3)

- 微生物油(精準發酵)

- 植物油(芥花油、椰子油、葵花油)

- 功能性添加劑

- 澱粉

- 纖維(纖維素、柑橘、亞麻籽、奇亞籽)

- 天然色素(藻膽蛋白、植物濃縮物)

第7章:市場估計與預測:依功能分類,2021-2034年

- 關鍵趨勢

- 蛋白質和營養增強

- 紋理和結構形成

- 風味和口感增強

- 結合與凝膠化

- 顏色和外觀

- 其他

第8章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 食品製造商(B2B)

- 餐飲服務及餐廳

- 零售品牌

第9章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第10章:公司簡介

- AGT Foods & Ingredients

- Algama Foods

- Angel Yeast Co., Ltd.

- BENEO GmbH (Sudzucker Group)

- Bunge Limited

- Cargill, Incorporated

- CP Kelco (JM Huber Corporation)

- dsm-firmenich

- FMC Corporation (BioPolymer Division)

- Ingredion Incorporated

- Kalys (MERIDIS Group)

- Mara Renewables Corporation

- MGP Ingredients, Inc.

- Paleo (formerly Miruku)

- Roquette Freres

The Global Plant-Based Seafood Ingredients Market was valued at USD 43.7 million in 2024 and is estimated to grow at a CAGR of 23% to reach USD 369.3 million by 2034.

The surge in demand reflects consumers' growing preference for sustainable, ethical, and health-conscious foods. Plant-based seafood alternatives are gaining traction due to their ability to closely replicate conventional seafood in taste, texture, and appearance, while addressing concerns about overfishing, marine pollution, and climate change. Consumers are increasingly aware of the health advantages of plant-based diets, including lower cholesterol levels, improved cardiovascular health, and weight management. The primary application of these ingredients is to provide a sustainable and nutritious substitute for traditional seafood, catering to the expanding vegan, vegetarian, and flexitarian populations. These ingredients are utilized in the production of seafood analogs, ready-to-eat meals, snacks, and functional food products, enabling food manufacturers to reduce environmental impact while delivering the sensory qualities consumers desire.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $43.7 Million |

| Forecast Value | $369.3 Million |

| CAGR | 23% |

The legume-based ingredients segment held a 45% share in 2024, due to their high protein content, versatility, and environmental benefits. Soy, pea, and chickpea derivatives are increasingly used to replicate seafood textures and flavors for health-conscious and eco-aware consumers. Processing advancements are enhancing their functionality for seafood applications.

The protein ingredients segment held 40.2% share in 2024, focusing on plant-derived proteins that improve nutritional content and functional properties. Innovations in protein extraction and processing have significantly improved taste and texture, while clean-label and allergen-free trends continue to drive product development.

North America Plant-Based Seafood Ingredients Market held a 42.3% share in 2024 and is expected to grow at a 23.1% CAGR through 2034, with the U.S. market valued at USD 14.8 million in 2024. Growth in this region is driven by health-conscious consumers, sustainability concerns, and ethical considerations. Technological advancements in plant protein extraction and fermentation have enabled the creation of seafood alternatives with authentic taste and texture. Additional market momentum comes from favorable regulations and increased product launches across retail and food service sectors.

Key players in the Plant-Based Seafood Ingredients Market include Cargill, Incorporated; DSM-Firmenich; Ingredion Incorporated; Bunge Limited; CP Kelco (J.M. Huber Corporation); Roquette Freres; AGT Foods & Ingredients; Angel Yeast Co., Ltd.; Mara Renewables Corporation; Paleo (formerly Miruku); BENEO GmbH (Sudzucker Group); FMC Corporation (BioPolymer Division); Kalys (MERIDIS Group); and Algama Foods. Leading companies in the Plant-Based Seafood Ingredients Market are adopting strategies such as expanding product portfolios, investing in R&D for texture and taste improvements, forming partnerships with foodservice and retail brands, and leveraging sustainable and clean-label claims. They are also focusing on geographic expansion, strategic collaborations, and technological innovations in protein extraction and fermentation processes to strengthen market presence and appeal to environmentally conscious and health-focused consumers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Source

- 2.2.3 Ingredient type

- 2.2.4 Functionality

- 2.2.5 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product category

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Source, 2021-2034 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 Legume-based ingredients

- 5.3 Cereal & grain-based ingredients

- 5.4 Seaweed & algae-based ingredients

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Ingredient Type, 2021-2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 Protein ingredients

- 6.2.1 Pea protein

- 6.2.2 Soy protein

- 6.2.3 Wheat gluten

- 6.3 Hydrocolloids & texturizing agents

- 6.3.1 Carrageenan

- 6.3.2 Alginate

- 6.3.3 Agar

- 6.3.4 Konjac glucomannan

- 6.3.5 Other hydrocolloids

- 6.4 Flavoring ingredients

- 6.4.1 Yeast extract

- 6.4.2 Seaweed seasoning & extracts

- 6.4.3 Vegetable umami & natural flavors

- 6.5 Oils & fats

- 6.5.1 Algal oil (omega-3)

- 6.5.2 Microbial oils (precision fermentation)

- 6.5.3 Plant oils (canola, coconut, sunflower)

- 6.6 Functional additives

- 6.6.1 Starches

- 6.6.2 Fibers (cellulose, citrus, flax, chia)

- 6.6.3 Natural colorants (phycobiliproteins, vegetable concentrates)

Chapter 7 Market Estimates and Forecast, By Functionality, 2021-2034 (USD Million & Kilo Tons)

- 7.1 Key trend

- 7.2 Protein & nutrition enhancement

- 7.3 Texture & structure formation

- 7.4 Flavor & taste enhancement

- 7.5 Binding & gelation

- 7.6 Color & appearance

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By End Use, 2021-2034 (USD Million & Kilo Tons)

- 8.1 Key trends

- 8.2 Food manufacturers (B2B)

- 8.3 Foodservice & restaurants

- 8.4 Retail brands

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Million & Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 AGT Foods & Ingredients

- 10.2 Algama Foods

- 10.3 Angel Yeast Co., Ltd.

- 10.4 BENEO GmbH (Sudzucker Group)

- 10.5 Bunge Limited

- 10.6 Cargill, Incorporated

- 10.7 CP Kelco (J.M. Huber Corporation)

- 10.8 dsm-firmenich

- 10.9 FMC Corporation (BioPolymer Division)

- 10.10 Ingredion Incorporated

- 10.11 Kalys (MERIDIS Group)

- 10.12 Mara Renewables Corporation

- 10.13 MGP Ingredients, Inc.

- 10.14 Paleo (formerly Miruku)

- 10.15 Roquette Freres