|

市場調查報告書

商品編碼

1885881

基於聊天機器人的心理健康應用市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Chatbot-Based Mental Health Apps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

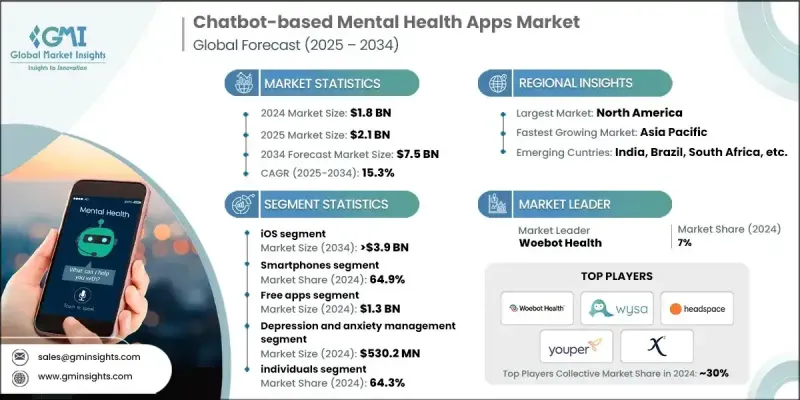

2024 年全球基於聊天機器人的心理健康應用程式市場價值為 18 億美元,預計到 2034 年將以 15.3% 的複合年成長率成長至 75 億美元。

隨著越來越多的人面臨心理健康挑戰,並轉向能夠提供即時、私密且持續支援的數位工具,市場需求正在不斷成長。隨著資金投入的增加和數位化優先護理模式的日益普及,人工智慧驅動的心理健康解決方案的應用也在持續擴大。智慧型手機的普及和網路存取的廣泛應用,使得基於應用程式的心理健康支援服務觸手可及,用戶能夠將這些工具融入日常生活。隨著醫療系統向遠端和預防性護理轉型,聊天機器人技術正在幫助彌合有限的臨床資源與眾多需要持續指導的人群之間的差距。這些應用程式提供可擴展且經濟高效的幫助,為那些可能難以獲得傳統治療的用戶提供了一種切實可行的替代方案。虛擬護理的持續發展以及循證數位治療技術的日益普及,正在各個人群和地區推動市場成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 18億美元 |

| 預測值 | 75億美元 |

| 複合年成長率 | 15.3% |

預計到2024年,iOS平台將佔據48%的市場。該平台之所以領先,是因為其在付費應用程式用戶群中擁有強大的影響力,用戶對蘋果資料保護政策充滿信心,並且與整合設備無縫兼容。 iOS的訂閱制獲利模式也促使開發者優先選擇在該平台上發布應用程式。此外,iOS強大的技術環境也使得先進的AI心理健康功能能夠安全運行,從而吸引那些尋求臨床可靠數位健康工具的使用者。

2024年,憂鬱症和焦慮症管理領域的市場規模預計將達到5.302億美元,佔據最大的市場佔有率。這些疾病在全球範圍內普遍存在,因此成為自動化心理健康工具的主要關注點。基於聊天機器人的平台提供結構化的治療支援、情緒監測和互動指導,旨在幫助使用者管理症狀。由於能夠即時獲得幫助且無需承受任何社會壓力,這些解決方案對於那些難以獲得傳統心理諮商服務的人來說極具吸引力。

2024年,北美基於聊天機器人的心理健康應用市場佔據了56.7%的市場。人們對心理健康的高度重視以及強大的技術基礎設施是其主導的主要原因。該地區對人工智慧賦能的健康工具的接受度迅速提高,這得益於人們對情緒健康的日益關注。企業健康計畫和措施將心理健康應用與保險福利掛鉤,推動了此類應用的普及,並強化了其在應對焦慮、壓力和憂鬱等問題方面的應用。

全球聊天機器人心理健康應用市場的主要參與者包括 MindSpa、Headspace、Daylio、EARKICK、Woebot Health、Wysa、youper、Sonia、Yuna、Luka, Inc.、X2AI, Inc. 和 matellio。這些公司正透過提升人工智慧能力、建立臨床合作關係以及擴展多語言和文化適應性內容來鞏固其競爭優勢。許多開發者正在整合實證治療方法,以提高可信度並獲得醫療網路的更強力的認可。各公司正在改進自然語言模型,以提供更個人化的對話體驗,並擴大所涵蓋的心理健康問題範圍。與保險公司、雇主和遠距醫療服務機構的策略合作有助於公司進入更大的用戶生態系統,並提高用戶的長期參與度。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 產業影響因素

- 成長促進因素

- 精神健康障礙盛行率不斷上升

- 數位健康科技在心理健康領域的應用日益廣泛

- 全天候可及性和消除污名化帶來的益處

- 產業陷阱與挑戰

- 資料隱私和連線問題

- 機會

- 與穿戴式技術的整合

- 越來越重視預防性和個人化健康

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 投資環境

- 報銷方案

- 醫療服務模式轉型

- 聊天機器人技術的演變

- 政策展望

- 波特的分析

- PESTEL 分析

- 差距分析

- 未來市場趨勢

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 亞太地區

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依平台分類,2021-2034年

- 主要趨勢

- iOS

- 安卓

- 其他平台類型

第6章:市場估算與預測:依設備類型分類,2021-2034年

- 主要趨勢

- 智慧型手機

- 片劑

- 筆記型電腦/桌上型電腦

第7章:市場估計與預測:依所得模式分類,2021-2034年

- 主要趨勢

- 免費應用

- 訂閱制

第8章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 憂鬱症與焦慮症管理

- 冥想管理

- 壓力管理

- 健康管理

- 其他應用

第9章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 個人

- 企業和雇主

- 其他最終用途

第10章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- Daylio

- EARKICK

- Headspace

- Luka, Inc.

- mindspa

- Sonia

- Woebot Health

- Wysa

- youper

- Yuna

- matellio

- X2AI, Inc.

The Global Chatbot-Based Mental Health Apps Market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 15.3% to reach USD 7.5 billion by 2034.

Demand is rising as more people face mental health challenges and turn toward digital tools that offer immediate, discreet, and continuous support. Adoption of AI-driven mental wellness solutions continues to expand as funding increases and digital-first care models become more common. Growing smartphone ownership and broader internet access have made app-based mental health support widely available, enabling users to integrate these tools into everyday routines. As health systems shift toward remote and preventive care, chatbot technologies are helping close the gap between limited clinical resources and the large number of individuals who need consistent guidance. By offering scalable and cost-efficient assistance, these applications provide a practical alternative for users who may not have easy access to traditional therapy. The ongoing move toward virtual care and the growing acceptance of evidence-based digital therapeutic techniques are reinforcing the market's momentum across various demographics and regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $7.5 Billion |

| CAGR | 15.3% |

The iOS segment held 48% share in 2024. This platform leads due to its strong presence among premium app users, confidence in Apple's data protection policies, and seamless compatibility with integrated devices. The structure of subscription-based monetization on iOS often encourages developers to prioritize launches on this system. Its robust technological environment also allows advanced AI-powered mental health features to operate securely, appealing to users looking for clinically reliable digital wellness tools.

The depression and anxiety management segment was valued at USD 530.2 million in 2024, representing the largest share of the market. These conditions are widespread worldwide, making them a primary focus for automated mental health tools. Chatbot-based platforms deliver structured therapeutic support, mood monitoring, and interactive guidance designed to help manage symptoms. The ability to access assistance immediately, with no social pressure attached, makes these solutions compelling for people who have limited access to conventional counseling.

North America Chatbot-Based Mental Health Apps Market accounted for a 56.7% share in 2024. High awareness of mental well-being and strong technological infrastructure contribute to this dominance. The region demonstrates rapid uptake of AI-enabled health tools, supported by a growing emphasis on emotional wellness. Adoption is propelled by workplace wellness programs and initiatives that connect mental health apps with insurance-backed benefits, reinforcing their use for issues such as anxiety, stress, and depression.

Prominent companies active in the Global Chatbot-Based Mental Health Apps Market include MindSpa, Headspace, Daylio, EARKICK, Woebot Health, Wysa, youper, Sonia, Yuna, Luka, Inc., X2AI, Inc., and matellio. Companies operating in this market are strengthening their competitive positions by enhancing AI capabilities, forming clinical partnerships, and expanding multilingual and culturally adaptive content. Many developers are integrating evidence-based therapeutic methods to improve credibility and achieve stronger validation from healthcare networks. Firms are refining natural language models to deliver more personalized conversational experiences and broaden the scope of mental health conditions addressed. Strategic collaborations with insurers, employers, and telehealth services help companies enter larger user ecosystems and increase long-term engagement.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Platform trends

- 2.2.3 Device trends

- 2.2.4 Revenue model trends

- 2.2.5 Application trends

- 2.2.6 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of mental health disorders

- 3.2.1.2 Growing adoption of digital health technologies for mental wellness

- 3.2.1.3 Round-the-clock accessibility and destigmatization benefits

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data privacy and connectivity issues

- 3.2.3 Opportunities

- 3.2.3.1 Integration with wearable technology

- 3.2.3.2 Growing focus on preventive and personalized wellness

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Investment landscape

- 3.7 Reimbursement scenario

- 3.8 Healthcare delivery model transformation

- 3.9 Evolution of chatbot technology

- 3.10 Policy outlook

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Gap analysis

- 3.14 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Platform, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 iOS

- 5.3 Android

- 5.4 Other platform types

Chapter 6 Market Estimates and Forecast, By Device, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Smartphones

- 6.3 Tablets

- 6.4 Laptops/desktops

Chapter 7 Market Estimates and Forecast, By Revenue Model, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Free apps

- 7.3 Subscription-based

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Depression and anxiety management

- 8.3 Meditation management

- 8.4 Stress management

- 8.5 Wellness management

- 8.6 Other applications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Individuals

- 9.3 Corporates & employers

- 9.4 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Daylio

- 11.2 EARKICK

- 11.3 Headspace

- 11.4 Luka, Inc.

- 11.5 mindspa

- 11.6 Sonia

- 11.7 Woebot Health

- 11.8 Wysa

- 11.9 youper

- 11.10 Yuna

- 11.11 matellio

- 11.12 X2AI, Inc.

醫療聊天機器人市場:按組件、類型、平台、技術、應用、部署管道和最終用戶分類-2026-2032年全球市場預測

醫療聊天機器人市場:按組件、類型、平台、技術、應用、部署管道和最終用戶分類-2026-2032年全球市場預測 醫療聊天機器人市場報告:按組件、部署模式、應用程式、最終用戶和地區分類(2026-2034 年)

醫療聊天機器人市場報告:按組件、部署模式、應用程式、最終用戶和地區分類(2026-2034 年) 2026年全球醫療保健聊天機器人市場報告

2026年全球醫療保健聊天機器人市場報告 醫療聊天機器人市場規模、佔有率、成長、全球產業分析:依類型、應用、區域洞察和預測(2026-2034年)

醫療聊天機器人市場規模、佔有率、成長、全球產業分析:依類型、應用、區域洞察和預測(2026-2034年) 醫療保健聊天機器人市場 - 全球產業規模、佔有率、趨勢、機會和預測,按組件、類型、部署方式、應用、地區和競爭格局細分,2020-2030 年預測

醫療保健聊天機器人市場 - 全球產業規模、佔有率、趨勢、機會和預測,按組件、類型、部署方式、應用、地區和競爭格局細分,2020-2030 年預測 基於聊天機器人的心理健康應用市場規模、佔有率、行業分析報告:按技術、設備、應用、平台、地區、展望和預測,2025-2032 年2025年全球心理健康與治療聊天機器人市場報告心理健康聊天機器人市場(按組件、技術、治療方法、部署類型、最終用戶和應用)—2025-2030 年全球預測

基於聊天機器人的心理健康應用市場規模、佔有率、行業分析報告:按技術、設備、應用、平台、地區、展望和預測,2025-2032 年2025年全球心理健康與治療聊天機器人市場報告心理健康聊天機器人市場(按組件、技術、治療方法、部署類型、最終用戶和應用)—2025-2030 年全球預測 美國基於聊天機器人的心理健康應用市場規模、佔有率、趨勢分析報告:按應用、平台、技術、設備、細分市場預測,2025 年至 2033 年基於聊天機器人的心理健康應用市場規模、佔有率、趨勢分析報告:按技術、應用、平台、設備、最終用途、地區和細分市場預測,2025 年至 2033 年

美國基於聊天機器人的心理健康應用市場規模、佔有率、趨勢分析報告:按應用、平台、技術、設備、細分市場預測,2025 年至 2033 年基於聊天機器人的心理健康應用市場規模、佔有率、趨勢分析報告:按技術、應用、平台、設備、最終用途、地區和細分市場預測,2025 年至 2033 年