|

市場調查報告書

商品編碼

1885865

清潔標籤蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Clean Label Protein Hydrolysates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

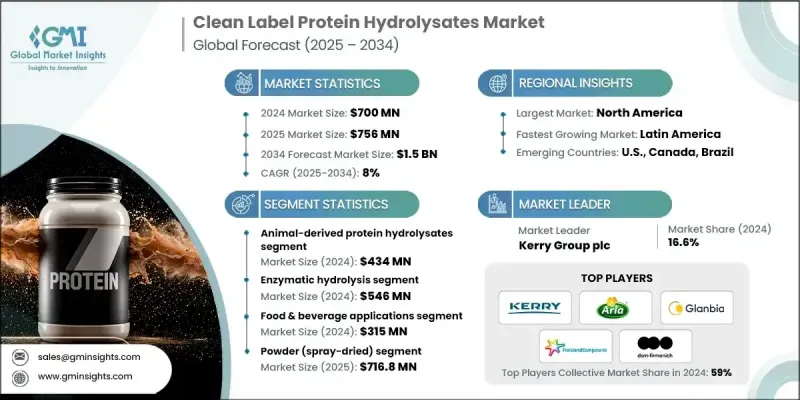

2024 年全球清潔標籤蛋白質水解物市場價值為 7 億美元,預計到 2034 年將以 8% 的複合年成長率成長至 15 億美元。

隨著運動營養和以提升運動表現為導向的配方產品逐漸獲得主流市場的青睞,消費者更加注重能夠快速吸收、易於消化的蛋白質,以促進肌肉恢復和維持能量,因此,蛋白質市場的成長速度正在加快。這種轉變促使各大品牌重新配製飲料、點心和粉狀補充劑,採用酵素解蛋白來提高胺基酸的使用率和消化舒適度。消費者對清潔標籤的期望正在重塑採購模式,他們更傾向於加工過程最少、來源透明且成分清晰的產品。酶解蛋白水解物因其可控的加工過程、高功能性和經過驗證的純度,完美契合了這些需求。其應用範圍不斷擴大,涵蓋了嬰幼兒營養、健康飲品和強化食品等領域。此外,水解蛋白卓越的消化率和生物利用度也使其在臨床和治療營養領域擁有廣闊的應用前景。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 7億美元 |

| 預測值 | 15億美元 |

| 複合年成長率 | 8% |

2024年,酵素水解領域創造了5.46億美元的收入,並憑藉其生產具有精確胜肽結構的高品質純淨水解物的能力,保持著領先的市場佔有率。此方法最佳化了消化率、生物利用度和感官性能,使其適用於嬰幼兒營養品、特殊配方奶粉和高性能營養補充劑。

至2034年,噴霧乾燥粉末產品市場將以7.8%的複合年成長率成長。這些粉末產品憑藉其保存期限長、穩定性好以及便於全球運輸等優勢佔據市場主導地位。其低水分含量和高濃度使其能夠進行大規模生產,並可無縫應用於運動營養粉、嬰幼兒營養品和臨床營養產品。

2024年,北美清潔標章蛋白水解物市場規模將達2.24億美元,佔全球市佔率的32%。該地區的領先地位主要由美國推動,這得益於其發達的運動營養產業、強大的臨床營養品生產能力以及對嬰幼兒配方奶粉和膳食補充劑的強勁需求。高人均蛋白質攝取量以及健全的乳製品和生物技術生態系統進一步鞏固了該地區的市場成長。

全球清潔標籤蛋白水解物市場的主要企業包括Arla Foods Ingredients、Kerry Group plc、Glanbia Nutritionals、FrieslandCampina Ingredients、Archer Daniels Midland Company (ADM)、Cargill, Incorporated、DSM-Firmenich、Norilia AS、Roquette Freres、Tate & Lyygeny、Norilia AS、Roquette Freres、Tate &leyalis. GmbH。這些企業正透過對先進酵素加工、高純度原料研發和清潔標籤認證的定向投資來提升自身的競爭力。許多公司正在擴大產能以支持全球分銷,同時致力於透過精確的水解控制來改善產品的風味、溶解性和消化率。與運動營養品、嬰幼兒配方奶粉和醫用營養品生產商建立策略合作夥伴關係,有助於建立長期的供應和創新管道。此外,為了滿足不斷變化的消費者期望,企業也在優先考慮透明的採購、可追溯性系統以及減少添加劑的使用。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 增加運動營養和功能性食品的消費

- 消費者對清潔標籤產品的需求不斷成長

- 臨床和醫學營養應用領域的成長

- 產業陷阱與挑戰

- 酶水解生產成本高

- 複雜的監理合規要求

- 市場機遇

- 用於熱飲的耐熱水解物

- 有機和非基因改造認證水解物

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 產品

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依蛋白質來源分類,2021-2034年

- 主要趨勢

- 動物源性蛋白質水解物

- 乳製品水解物

- 乳清蛋白水解物

- 酪蛋白水解物

- 乳蛋白水解物

- 肉類和家禽水解物

- 水解禽肉蛋白

- 水解牛肉和豬肉蛋白

- 海洋來源水解物

- 其他動物來源

- 膠原蛋白和明膠水解物

- 蛋清蛋白水解物

- 血液蛋白水解物

- 乳製品水解物

- 植物源蛋白水解物

- 大豆蛋白水解物

- 豌豆蛋白水解物

- 米蛋白水解物

- 小麥蛋白水解物

- 玉米蛋白水解物

- 其他植物來源(蠶豆、大麻、高粱)

第6章:市場估算與預測:依加工方式分類,2021-2034年

- 主要趨勢

- 酵素水解

- 化學水解(酸性和鹼性)

- 微生物發酵

第7章:市場估計與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 食品飲料應用

- 運動營養及性能產品

- 嬰兒營養與低敏配方奶粉

- 臨床與醫學營養

- 功能性食品和飲料

- 烘焙食品和糖果

- 鹹味應用及風味增強

- 乳製品

- 動物飼料與營養

- 水產飼料

- 寵物食品

- 牲畜飼料

- 生物製藥與細胞培養

- 哺乳動物細胞培養基

- 疫苗生產

- 單株抗體生產

- 化妝品及個人護理

第8章:市場估算與預測:依形式分類,2021-2034年

- 主要趨勢

- 粉末(噴霧乾燥)

- 液體和濃縮膏體

- 半固體形式

第9章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第10章:公司簡介

- Arla Foods Ingredients

- Kerry Group plc

- Glanbia Nutritionals

- FrieslandCampina Ingredients

- Archer Daniels Midland Company (ADM)

- Cargill, Incorporated

- DSM-Firmenich

- Norilia AS

- Roquette Freres

- Tate & Lyle PLC

- Lactalis Ingredients

- Peak Protein LLC

- Nuritas

- AB Enzymes GmbH

The Global Clean Label Protein Hydrolysates Market was valued at USD 700 million in 2024 and is estimated to grow at a CAGR of 8% to reach USD 1.5 billion by 2034.

Growth is accelerating as sports nutrition and performance-focused formulations gain mainstream traction, with consumers prioritizing fast-absorbing, easily digestible proteins that assist in muscle recovery and sustained energy. This shift is encouraging brands to reformulate beverages, snacks, and powdered supplements using enzyme-processed proteins to improve amino acid availability and digestive comfort. Clean-label expectations are reshaping procurement practices, as buyers prefer minimal processing, transparent sourcing, and recognizable ingredient lists. Enzyme-generated hydrolysates align well with these preferences due to their controlled processing, high functionality, and verified purity. Their expanding use extends into early-life nutrition, wellness beverages, and fortified foods. Clinical and therapeutic nutrition also represents a strong application area, supported by the exceptional digestibility and bioavailability of hydrolyzed proteins.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $700 Million |

| Forecast Value | $1.5 Billion |

| CAGR | 8% |

The enzymatic hydrolysis segment generated USD 546 million in 2024 and maintains a leading share due to its ability to produce clean, high-quality hydrolysates with precise peptide structures. This method optimizes digestibility, bioavailability, and sensory performance, making it suitable for infant nutrition, medical formulas, and high-performance supplements.

The powder (spray-dried) formats segment will grow at a CAGR of 7.8% through 2034. These powders dominate because of their long shelf life, stability, and ease of global transport. Their low moisture content and high concentration support large-scale production, enabling seamless integration into sports powders, infant nutrition, and clinical nutrition products.

North America Clean Label Protein Hydrolysates Market accounted for USD 224 million in 2024, representing a 32% share. The region's leadership is driven by the United States, supported by a well-developed sports nutrition industry, extensive clinical nutrition manufacturing capacity, and strong demand for infant formula and dietary supplements. High per-capita protein intake and a robust dairy and biotechnology ecosystem further reinforce regional expansion.

Major companies active in the Global Clean Label Protein Hydrolysates Market include Arla Foods Ingredients, Kerry Group plc, Glanbia Nutritionals, FrieslandCampina Ingredients, Archer Daniels Midland Company (ADM), Cargill, Incorporated, DSM-Firmenich, Norilia AS, Roquette Freres, Tate & Lyle PLC, Lactalis Ingredients, Peak Protein LLC, Nuritas, and AB Enzymes GmbH. Companies in the Global Clean Label Protein Hydrolysates Market are enhancing their competitive position through targeted investments in advanced enzymatic processing, high-purity ingredient development, and clean-label certification. Many firms are expanding production capacity to support global distribution while focusing on improving flavor, solubility, and digestibility through precise hydrolysis controls. Strategic partnerships with sports nutrition, infant formula, and medical nutrition manufacturers are helping create long-term supply and innovation pipelines. Businesses are also prioritizing transparent sourcing, traceability systems, and reduced additive use to align with evolving consumer expectations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Protein Source

- 2.2.3 Processing Method

- 2.2.4 Application

- 2.2.5 Form

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing sports nutrition & functional food consumption

- 3.2.1.2 Rising consumer demand for clean label products

- 3.2.1.3 Growth in clinical & medical nutrition applications

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs of enzymatic hydrolysis

- 3.2.2.2 Complex regulatory compliance requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Heat-stable hydrolysates for hot beverage applications

- 3.2.3.2 Organic & non-GMO certified hydrolysates

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Product

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Protein Source, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Animal-derived protein hydrolysates

- 5.2.1 Dairy-based hydrolysates

- 5.2.1.1 Whey protein hydrolysates

- 5.2.1.2 Casein hydrolysates

- 5.2.1.3 Milk protein hydrolysates

- 5.2.2 Meat & poultry hydrolysates

- 5.2.2.1 Hydrolyzed poultry protein

- 5.2.2.2 Hydrolyzed beef & pork proteins

- 5.2.3 Marine-derived hydrolysates

- 5.2.4 Other animal sources

- 5.2.4.1 Collagen & gelatin hydrolysates

- 5.2.4.2 Egg protein hydrolysates

- 5.2.4.3 Blood protein hydrolysates

- 5.2.1 Dairy-based hydrolysates

- 5.3 Plant-Derived Protein Hydrolysates

- 5.3.1 Soy protein hydrolysates

- 5.3.2 Pea protein hydrolysates

- 5.3.3 Rice protein hydrolysates

- 5.3.4 Wheat protein hydrolysates

- 5.3.5 Corn protein hydrolysates

- 5.3.6 Other plant sources (fava bean, hemp, sorghum)

Chapter 6 Market Estimates and Forecast, By Processing Method, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Enzymatic hydrolysis

- 6.3 Chemical hydrolysis (acid & alkaline)

- 6.4 Microbial fermentation

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverage applications

- 7.2.1 Sports nutrition & performance products

- 7.2.2 Infant nutrition & hypoallergenic formulas

- 7.2.3 Clinical & medical nutrition

- 7.2.4 Functional foods & beverages

- 7.2.5 Bakery & confectionery

- 7.2.6 Savory applications & flavor enhancement

- 7.2.7 Dairy products

- 7.3 Animal feed & nutrition

- 7.3.1 Aquaculture feed

- 7.3.2 Pet food

- 7.3.3 Livestock feed

- 7.4 Biopharmaceutical & cell culture

- 7.4.1 Mammalian cell culture media

- 7.4.2 Vaccine production

- 7.4.3 Monoclonal antibody manufacturing

- 7.5 Cosmetics & personal care

Chapter 8 Market Estimates and Forecast, By Form, 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Powder (spray-dried)

- 8.3 Liquid & concentrated paste

- 8.4 Semi-solid forms

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Arla Foods Ingredients

- 10.2 Kerry Group plc

- 10.3 Glanbia Nutritionals

- 10.4 FrieslandCampina Ingredients

- 10.5 Archer Daniels Midland Company (ADM)

- 10.6 Cargill, Incorporated

- 10.7 DSM-Firmenich

- 10.8 Norilia AS

- 10.9 Roquette Freres

- 10.10 Tate & Lyle PLC

- 10.11 Lactalis Ingredients

- 10.12 Peak Protein LLC

- 10.13 Nuritas

- 10.14 AB Enzymes GmbH