|

市場調查報告書

商品編碼

1885823

航太複合材料碳纖維回收市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Carbon Fiber Recycling from Aerospace Composites Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

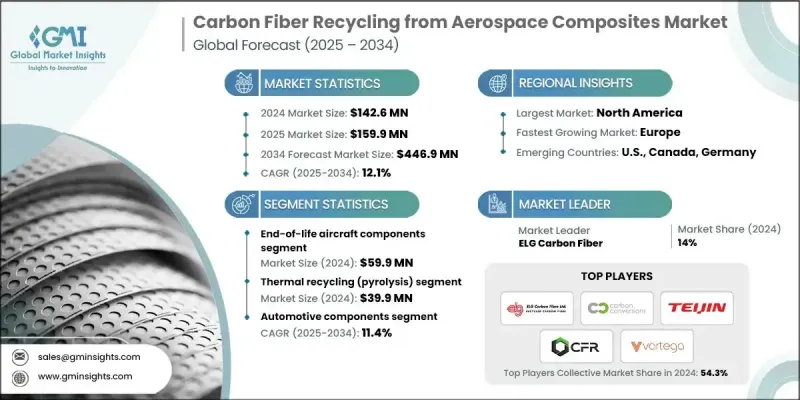

2024 年全球航太複合材料碳纖維回收市場價值為 1.426 億美元,預計到 2034 年將以 12.1% 的複合年成長率成長至 4.469 億美元。

回收技術的快速發展使得再生碳纖維更具成本效益且品質更高,從而促進了其在航太及相關領域的更廣泛應用。在顯著降低能耗的同時保持機械強度的新方法正在加速其商業化應用,並提升製程的永續性。不斷擴大的回收基礎設施和日益成熟的工業能力為處理飛機退役產生的複合材料廢料提供了支援。全球對循環製造的重視、更嚴格的環境目標以及更強力的監管指導也在推動對先進回收系統的投資。廢舊複合材料的日益增多以及將其轉化為高價值再生纖維的技術可行性,為大規模應用創造了有利條件。隨著回收技術的進步和供應鏈整合效率的提高,再生碳纖維正成為航太、汽車和工業應用領域日益重要的策略材料。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 1.426億美元 |

| 預測值 | 4.469億美元 |

| 複合年成長率 | 12.1% |

2024年,報廢飛機零件創造了5,990萬美元的收入。退役飛機包含大量碳纖維結構,例如機身部件、機翼組件和尾翼部件,使其成為極具價值的回收材料來源。全球老舊機隊加速退役,持續擴大原料供應,凸顯了這項材料流在回收的重要性。

2024年,包括熱解在內的熱回收技術市場規模達3,990萬美元。該方法佔據主導地位,因為它能夠可靠地提取高品質纖維,且不會損害其結構特性。其可擴展性、處理大批量複合材料的能力以及相對較低的營運成本,使其成為最具商業可行性的技術。系統的持續改進和能量回收方法的最佳化進一步提升了其經濟效益。雖然其他製程也能回收高純度纖維,但其高昂的成本限制了其廣泛應用,因此熱回收技術鞏固了其作為領先工業解決方案的地位。

受強勁的航太製造業活動和不斷擴大的回收能力推動,北美航空航太複合材料碳纖維回收市場在2024年預計將達到5,200萬美元。該地區受益於眾多原始設備製造商(OEM)、一級供應商和新興回收企業的集中,這些企業不斷提升了自身的生產能力。不斷擴大的商業設施和持續的研究項目增強了國內供應,而下游產業的需求則進一步推動了區域成長。

活躍於航太複合材料碳纖維回收市場的關鍵企業包括東麗先進複合材料公司(東麗集團)、ELG碳纖維公司、三菱化學公司、Carbon Conversions公司、SGL Carbon公司、Carbon Fiber Recycling (CFR)公司、帝人株式會社、Carbon Fiber Conversions GmbH公司、 航太 . Corporation。這些企業透過擴大產能、採用先進的回收技術以及投資節能製程(以維持纖維強度)來提升自身的競爭力。許多企業尋求與航太原始設備製造商(OEM)建立策略合作夥伴關係,以確保穩定的原料供應,並將回收材料整合到下一代零件中。改善製程自動化、降低營運成本以及擴展連續回收系統等措施有助於提高產品可靠性。此外,各企業也致力於制定認證標準,以確保回收纖維符合航空航太級性能要求。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 提高飛機退役率

- 永續發展法規與循環經濟目標

- 回收製程的技術進步

- 產業陷阱與挑戰

- 再生碳纖維的機械性質不一致

- 缺乏標準化和認證框架

- 市場機遇

- 航太領域對輕質材料的需求日益成長

- 政府激勵措施和綠色採購政策

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 原料來源

- 科技

- 應用

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依原料來源分類,2021-2034年

- 主要趨勢

- 報廢飛機部件

- 已退役的機身段

- 機翼和尾翼結構

- 內裝板和配件

- 引擎罩和短艙

- 生產廢料

- 預浸料邊角料和修剪物

- 有缺陷或不合格的鋪層

- 高壓釜廢料和固化廢棄物

- MRO(維修、修理和大修)廢棄物

- 更換或維修面板

- 大修造成的複合材料零件損壞

- 改造後的剩餘零件

- 原型製作和研發廢料

- 測試開發批次的零件

- 未經認證的實驗性組件

- 其他

第6章:市場估計與預測:依技術分類,2021-2034年

- 主要趨勢

- 機械回收

- 碎紙

- 研磨和磨削

- 顆粒化

- 熱回收(熱解)

- 常規熱解(惰性氣體)

- 微波輔助熱解

- 流體化床熱解

- 化學回收(溶劑分解/解聚)

- 酸/鹼催化溶劑分解

- 醇解和糖解作用方法

- 超臨界流體溶劑分解

- 超臨界流體處理

- 超臨界二氧化碳

- 超臨界水氧化

- 其他

第7章:市場估計與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 汽車零件

- 汽車結構件

- 車身面板和外部組件

- 室內應用

- 電子製造

- 電路板應用

- 電子外殼和機箱

- 熱管理元件

- 基礎設施應用

- 電網組件

- 建築材料

- 交通基礎設施

- 體育用品和消費品

- 休閒設備

- 消費性電子產品

- 其他

第8章:市場估算與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- Mitsubishi Chemical

- ELG Carbon Fibre

- Carbon Fiber Conversions GmbH

- Carbon Fiber Recycling (CFR)

- Carbon Conversions

- Teijin Limited

- SGL Carbon

- Toray Advanced Composites(Toray Group)

- Westlake Corporation

- Vartega Inc

The Global Carbon Fiber Recycling from Aerospace Composites Market was valued at USD 142.6 million in 2024 and is estimated to grow at a CAGR of 12.1% to reach USD 446.9 million by 2034.

Rapid progress in recovery technologies is making recycled carbon fiber more cost-effective and higher in quality, encouraging its wider use in aerospace and related sectors. New methods that significantly reduce energy consumption while preserving mechanical strength are accelerating commercial adoption and improving process sustainability. Expanding recycling infrastructure and maturing industrial capabilities support the rising volume of composite waste generated from aircraft decommissioning. Global emphasis on circular manufacturing, stricter environmental targets, and stronger regulatory direction are also driving investments in advanced recycling systems. The increasing availability of end-of-life composite materials and the technical viability of converting them into high-value secondary fibers are creating favorable conditions for large-scale deployment. As recycling technologies evolve and supply chains integrate more efficiently, recycled carbon fiber is becoming an increasingly strategic material for aerospace, automotive, and industrial applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $142.6 Million |

| Forecast Value | $446.9 Million |

| CAGR | 12.1% |

The end-of-life aircraft components generated USD 59.9 million in 2024. Retired aircraft contain substantial quantities of carbon-fiber-based structures such as fuselage elements, wing assemblies, and tail components, making them a valuable source for recovery. The accelerating retirement cycle of older fleets worldwide continues to expand feedstock supply, reinforcing the importance of this material stream in recycling operations.

Thermal recycling, including pyrolysis, reached USD 39.9 million in 2024. This method dominates because it reliably extracts high-quality fibers without undermining their structural characteristics. Its scalability, ability to process large composite volumes, and comparatively low operational costs position it as the most commercially feasible technique. Continuous system advancements and improved energy-recovery approaches further enhance its economic performance. While alternative processes can recover fibers with high purity, their elevated costs limit broad adoption, solidifying thermal recycling as the leading industrial solution.

North America Carbon Fiber Recycling from Aerospace Composites Market captured USD 52 million in 2024, owing to strong aerospace manufacturing activity and expanding recycling capacities. The region benefits from a strong concentration of OEMs, Tier-1 suppliers, and emerging recyclers, increasing their production capabilities. Expanding commercial facilities and ongoing research initiatives strengthen domestic supply, while demand from downstream sectors reinforces regional growth.

Key companies active in the Carbon Fiber Recycling from Aerospace Composites Market include Toray Advanced Composites (Toray Group), ELG Carbon Fibre, Mitsubishi Chemical, Carbon Conversions, SGL Carbon, Carbon Fiber Recycling (CFR), Teijin Limited, Carbon Fiber Conversions GmbH, Westlake Corporation, and Vartega Inc. Companies operating in Carbon Fiber Recycling from Aerospace Composites Market enhance their competitive position by scaling production capacity, adopting advanced recovery technologies, and investing in energy-efficient processes that preserve fiber strength. Many pursue strategic partnerships with aerospace OEMs to secure consistent feedstock and integrate recycled materials into next-generation components. Efforts to improve process automation, reduce operational costs, and expand continuous recycling systems help increase output reliability. Organizations also focus on establishing certification standards, ensuring recycled fibers meet aerospace-grade performance requirements.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Feedstock Source

- 2.2.3 Technology

- 2.2.4 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing aircraft decommissioning rates

- 3.2.1.2 Sustainability regulations and circular economy goals

- 3.2.1.3 Technological advancements in recycling processes

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Inconsistent mechanical properties of recycled carbon fiber

- 3.2.2.2 Lack of standardization and certification frameworks

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for lightweight materials in aerospace

- 3.2.3.2 Government incentives and green procurement policies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Feedstock Source

- 3.7.3 Technology

- 3.7.4 Application

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Feedstock Source, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 End-of-Life Aircraft Components

- 5.2.1 Retired fuselage sections

- 5.2.2 Wing and tail structures

- 5.2.3 Interior panels and fixtures

- 5.2.4 Engine cowls and nacelles

- 5.3 Production Scrap

- 5.3.1 Prepreg offcuts and trimmings

- 5.3.2 Defective or rejected layups

- 5.3.3 Autoclave rejects and cured waste

- 5.4 MRO (Maintenance, Repair & Overhaul) Waste

- 5.4.1 Replaced or repaired panels

- 5.4.2 Damaged composite parts from overhaul

- 5.4.3 Residual parts from retrofitting

- 5.5 Prototyping and R&D Scrap

- 5.5.1 Test parts from development batches

- 5.5.2 Non-certified experimental components

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Mechanical recycling

- 6.2.1 Shredding

- 6.2.2 Milling and grinding

- 6.2.3 Granulation

- 6.3 Thermal Recycling (Pyrolysis)

- 6.3.1 Conventional pyrolysis (inert gas)

- 6.3.2 Microwave-assisted pyrolysis

- 6.3.3 Fluidized bed pyrolysis

- 6.4 Chemical Recycling (Solvolysis / Depolymerization)

- 6.4.1 Acid/base catalyzed solvolysis

- 6.4.2 Alcoholysis and glycolysis methods

- 6.4.3 Supercritical fluid solvolysis

- 6.5 Supercritical fluid processing

- 6.5.1 Supercritical CO2

- 6.5.2 Supercritical water oxidation

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive components

- 7.2.1 Structural automotive parts

- 7.2.2 Body panels & exterior components

- 7.2.3 Interior applications

- 7.3 Electronics manufacturing

- 7.3.1 Circuit board applications

- 7.3.2 Electronic housings & enclosures

- 7.3.3 Thermal management components

- 7.4 Infrastructure applications

- 7.4.1 Electrical grid components

- 7.4.2 Construction & building materials

- 7.4.3 Transportation infrastructure

- 7.5 Sporting goods & consumer products

- 7.5.1 Recreational equipment

- 7.5.2 Consumer electronics

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Mitsubishi Chemical

- 9.2 ELG Carbon Fibre

- 9.3 Carbon Fiber Conversions GmbH

- 9.4 Carbon Fiber Recycling (CFR)

- 9.5 Carbon Conversions

- 9.6 Teijin Limited

- 9.7 SGL Carbon

- 9.8 Toray Advanced Composites(Toray Group)

- 9.9 Westlake Corporation

- 9.10 Vartega Inc

全球碳水化合物市場,2026-2030年

全球碳水化合物市場,2026-2030年 中間相瀝青基碳纖維市場按產品形式、纖維類型、應用和最終用途產業分類-全球預測(2026-2032 年)

中間相瀝青基碳纖維市場按產品形式、纖維類型、應用和最終用途產業分類-全球預測(2026-2032 年) 碳纖維:全球市場

碳纖維:全球市場 CABKOMA市場規模、佔有率和成長分析(按類型、應用和地區分類)-2026-2033年產業預測

CABKOMA市場規模、佔有率和成長分析(按類型、應用和地區分類)-2026-2033年產業預測 碳纖維市場預測至2032年:按產品類型、原料、纖維類型、應用、最終用戶和地區分類的全球分析

碳纖維市場預測至2032年:按產品類型、原料、纖維類型、應用、最終用戶和地區分類的全球分析 碳纖維市場-全球產業規模、佔有率、趨勢、機會和預測,依原料、產品類型、纖維類型、模量、應用、最終用途產業、地區和競爭格局分類,2020-2030年預測

碳纖維市場-全球產業規模、佔有率、趨勢、機會和預測,依原料、產品類型、纖維類型、模量、應用、最終用途產業、地區和競爭格局分類,2020-2030年預測 短切碳纖維:全球市佔率及排名、總收入及需求預測(2025-2031年)熱塑性碳纖維複合材料:全球市佔率及排名、總收入及需求預測(2025-2031年)運動用品用碳纖維:全球市佔率及排名、總收入及需求預測(2025-2031年)依前驅體類型、絲束尺寸、纖維形態和應用分類的大絲碳纖維市場—2025-2032年全球預測

短切碳纖維:全球市佔率及排名、總收入及需求預測(2025-2031年)熱塑性碳纖維複合材料:全球市佔率及排名、總收入及需求預測(2025-2031年)運動用品用碳纖維:全球市佔率及排名、總收入及需求預測(2025-2031年)依前驅體類型、絲束尺寸、纖維形態和應用分類的大絲碳纖維市場—2025-2032年全球預測