|

市場調查報告書

商品編碼

1885822

硬體在環 (HIL) 測試市場機會、成長促進因素、產業趨勢分析及預測(2025-2034 年)Hardware-in-the-Loop (HIL) Testing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

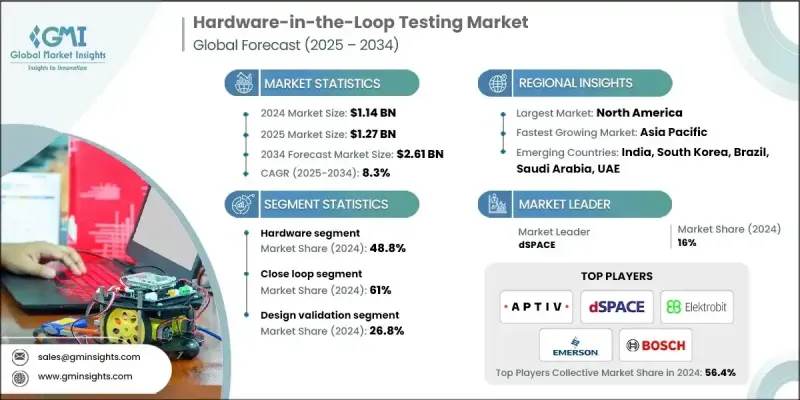

2024 年全球硬體在環 (HIL) 測試市場價值為 11.4 億美元,預計到 2034 年將以 8.3% 的複合年成長率成長至 26.1 億美元。

快速向先進控制架構的轉變以及對更快產品驗證的需求,凸顯了對能夠模擬高度複雜系統行為的即時模擬環境的迫切需求。硬體在環 (HIL) 平台支援持續軟體驗證、廣泛的多領域測試以及更早地檢測運行故障,使其成為現代工程工作流程中不可或缺的一部分。隨著開發週期的加速,解決方案供應商正在拓展其技術能力,擴展即時運算資源,增加更高密度的 I/O 闆卡,並深化與軟體工具鏈的合作。這些改進旨在滿足電動車、航空研究和下一代能源系統等領域日益成長的需求。企業越來越依賴 HIL 測試來評估高壓架構、推進裝置和併網設備在熱、老化和負載波動條件下的性能,而無需將實際設備置於風險之中。這種發展趨勢使 HIL 技術成為多個工業領域先進驗證實踐的核心推動力。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 11.4億美元 |

| 預測值 | 26.1億美元 |

| 複合年成長率 | 8.3% |

2024年,硬體部分佔據48.8%的市場佔有率,預計到2034年將以7.1%的複合年成長率成長。其重要性源自於對高效能實體組件的需求,包括即時運算單元、通道豐富的介面模組、可程式處理器、專用負載單元和功率密集測試平台。這些系統能夠提供微秒級的精確效能,用於驗證關鍵運作環境中使用的控制器和嵌入式邏輯。交通運輸、國防和能源等產業依賴這些硬體平台來檢驗電力推進系統、安全控制器和先進保護技術的實際運作。

2024年,閉迴路測試佔據了61%的市場佔有率,預計從2025年到2034年將以8%的年成長率成長。這種方法之所以保持主導地位,是因為它能夠實現實體組件和虛擬模型之間的無縫交互,從而創建一個能夠模擬實際運行情況的動態測試週期。工程師利用閉迴路測試系統,在高度逼真的條件下安全地檢驗控制單元、電氣系統和智慧功能的性能,而無需將實體原型暴露於實際運作風險之中。

2024年,北美硬體在環(HIL)測試市場規模達3.553億美元。該國市場的成長得益於自動化技術的持續進步、電動車的發展以及高度模組化車輛架構的廣泛應用。美國企業正在擴展驗證項目,以滿足不斷變化的安全、合規和數位系統完整性標準。電池開發、電氣化平台和下一代動力傳動系統的顯著進步,正在加速HIL環境的普及,從而降低與實體原型相關的成本並縮短工程週期。

硬體在環 (HIL) 測試市場的主要參與者包括 Aptiv、dSPACE、Elektrobit、Emerson、IPG Automotive、Lynx Software Technologies、MathWorks、Robert Bosch、Typhoon HIL 和 Vector Informatik。硬體在環測試市場中,各公司採取的關鍵策略是深化技術研發並加強協作開發。供應商正在投資增強型即時運算叢集、更高容量的介面板和先進的處理架構,以支援日益複雜的模擬。許多組織正在與軟體平台建立聯盟,以確保建模、測試和自動化工作流程之間的無縫整合。此外,各公司也正在擴大生產能力、拓展服務組合,並推出模組化 HIL 系統,以滿足不斷變化的設計需求。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基準估算和計算

- 基準年計算

- 市場估算的關鍵趨勢

- 初步研究和驗證

- 原始資料

- 預測模型

- 研究假設和局限性

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 矽和核心技術供應商

- 平台和系統供應商

- 軟體和模型提供者

- 系統整合商和專業服務

- 利潤率分析

- 矽和核心技術供應商

- 平台和系統供應商

- 軟體和模型提供者

- 系統整合商和服務

- 成本結構

- 每個階段的價值增加

- 影響價值鏈的因素

- 生態系統破壞

- 供應商格局

- 產業影響因素

- 成長促進因素

- 電動車普及及電池系統驗證要求分析

- ADAS/自動駕駛汽車的複雜性與軟體定義車輛架構

- 監理要求與功能安全標準(ISO 26262、IEC 61508、DO-178C)

- 電力電子與再生能源併網

- 降低成本勢在必行,虛擬驗證已證明其投資報酬率。

- 產業陷阱與挑戰

- 中小企業資本投入高,投資回收期長

- 熟練勞動力短缺和知識移轉挑戰

- 模型保真度和驗證挑戰

- 市場機遇

- 基於雲端的硬體在環測試和硬體在環即服務 (HILaaS)

- AI/ML驅動的測試自動化與場景生成

- 數位孿生整合和生命週期驗證

- 亞太市場擴張和本地化

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美監管格局

- 美國:聯邦和州級要求

- 加拿大:與美國標準協調

- 歐洲監管格局

- 歐盟:全面的型式認可和網路安全強制性要求

- 英國:脫歐後的監管差異

- 亞太地區監管環境

- 中國:國內標準和資料本地化

- 日本:品質標準與汽車卓越性

- 印度:新興市場,監管快速演變

- 韓國:先進技術和出口導向企業

- 拉丁美洲監管格局

- 巴西:具有本地化要求的區域領導者

- 墨西哥:美墨加協定整合及汽車製造中心

- 中東和非洲監管環境

- 阿拉伯聯合大公國和沙烏地阿拉伯:雄心勃勃的技術應用

- 南非:區域製造業中心

- 跨區域監理趨勢及其策略意義

- 北美監管格局

- 波特的分析

- PESTEL 分析

- 技術與創新格局

- 當前技術趨勢

- 基於FPGA加速的即時模擬平台

- 基於模型的設計(MBD)和模擬工具鏈

- 基於模組化 PXI/EtherCAT 的 HIL 架構

- 認證的安全與合規工具鏈

- 新興技術

- 雲端原生硬體在環平台和硬體在環即服務 (HILaaS)

- AI/ML驅動的測試自動化與場景生成

- 用於生命週期驗證的數位孿生整合

- 網路安全驗證與安全OTA更新測試

- 當前技術趨勢

- 專利分析

- 成本細分分析

- 貿易流分析

- 進口市場動態

- 全球進口模式

- 貿易壁壘和本地化

- 出口市場結構

- 出口障礙和激勵措施

- 貿易流趨勢及其策略意義

- 進口市場動態

- 永續性和環境方面

- 永續實踐的採納

- 廢棄物減量創新

- 能源效率最佳化

- 環境計劃的影響

- 用例

- 鐵鳥測試

- 飛彈研發

- 自主無人機測試

- ADAS和自動駕駛

- 電動出行和電動驅動

- 電網

- 車輛動力學

- 虛擬車輛

- 測試台

- 實際駕駛排放量(RDE)

- 最佳情況

- 全生命週期數位孿生-硬體在環整合

- 面向全球協作的雲端原生 HILaaS

- AI/ML驅動的自主驗證

- PHIL 用於再生能源併網

- 模組化、可升級、循環式硬體在環架構

- HIL市場主要競爭對手使用的FPGA系統

- 性能與應用契合度

- 可擴展性、模組化和生命週期成本

- 監管與認證優勢

- 生態系與整合

- 區域和監管差異

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估算與預測:依組件分類,2021-2034年

- 主要趨勢

- 硬體

- 輸入/輸出介面

- 基於 PCIe 的 I/O 介面

- 標準 PCIe 卡

- 高速資料擷取模組

- 客製化的FPGA整合PCIe解決方案

- 基於FPGA的I/O解決方案

- 基於英特爾(Altera)Arria的介面模組

- 基於 Xilinx Zynq 的介面模組

- FPGA I/O 擴充板

- 即時邏輯控制與訊號調理介面

- 基於乙太網路和 EtherCAT 的介面

- 工業乙太網路(千兆乙太網路、萬兆乙太網路、支援TSN)

- EtherCAT 主/從模組

- 使用 EtherCAT 的分散式 I/O 節點

- 時間同步通訊模組

- 基於 PCIe 的 I/O 介面

- 處理器

- 即時模擬器

- 數據採集系統

- 其他

- 輸入/輸出介面

- 軟體

- 服務

- 專業服務

- 託管服務

第6章:市場估算與預測:依產品類型分類,2021-2034年

- 主要趨勢

- 開迴路

- 閉迴路

第7章:市場估算與預測:依測試階段分類,2021-2034年

- 主要趨勢

- 設計驗證

- 整合測試

- 驗收測試

- 製造測試

- 性能測試

- 其他

第8章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 航太

- 防禦

- 鐵路

- 電力電子

- 汽車

- 醫療器材

- 再生能源系統

- 電信和網路

- 其他

第9章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第10章:公司簡介

- 全球參與者

- MathWorks

- National Instruments

- dSPACE

- Vector Informatik

- Spirent Communications

- Wind River

- Robert Bosch

- Emerson

- 區域玩家

- ADVANTECH

- APTIV

- Wabtec

- ETAS

- Hinduja Tech

- Elektrobit

- 小眾/新興玩家

- ADD2

- Concurrent Real-Time

- IPG Automotive

- Lynx Software Technologies

- Opal-RT Technologies

- Plexim

- RealTime Wave

- Speedgoat

- Typhoon HIL

The Global Hardware-in-the-Loop (HIL) Testing Market was valued at USD 1.14 billion in 2024 and is estimated to grow at a CAGR of 8.3% to reach USD 2.61 billion by 2034.

The rapid shift toward advanced control architectures and the push for faster product validation have amplified the need for real-time simulation environments that can mirror highly complex system behaviors. HIL platforms support continuous software verification, broad multi-domain testing, and earlier detection of operational faults, making them an essential part of modern engineering workflows. With development cycles accelerating, solution providers are broadening their technical capabilities, scaling real-time computing resources, adding higher-density I/O boards, and deepening cooperation with software toolchains. These enhancements cater to rising demand in electric mobility, aviation research, and next-generation energy systems. Companies are increasingly relying on HIL testing to evaluate high-voltage architectures, propulsion units, and grid-connected equipment under thermal, aging, and fluctuating load conditions without placing actual devices at risk. This evolution positions HIL technology as a core enabler for advanced verification practices across multiple industrial sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.14 Billion |

| Forecast Value | $2.61 Billion |

| CAGR | 8.3% |

The hardware segment held 48.8% share in 2024 and is projected to grow at a 7.1% CAGR through 2034. Its prominence stems from the need for high-performance physical components, including real-time computing units, channel-rich interface modules, programmable processors, specialized load units, and power-focused rigs. These systems deliver precise, microsecond-level performance needed to validate controllers and embedded logic used in critical operational environments. Industries such as transportation, defense, and energy rely on these hardware platforms to examine real-world behavior of electric propulsion systems, safety-driven controllers, and advanced protection technologies.

The closed-loop category held a 61% share in 2024 and is projected to grow at 8% from 2025 to 2034. This approach remains dominant because it enables seamless interaction between physical components and virtual models, creating a dynamic test cycle that mirrors operational behavior. Engineers use closed-loop setups to safely examine the performance of control units, electrified systems, and intelligent functions under highly realistic conditions without exposing physical prototypes to operational hazards.

North America Hardware-in-the-Loop (HIL) Testing Market generated USD 355.3 million in 2024. The country's growth is supported by continued progress in automated technologies, electric mobility development, and the wider adoption of highly modular vehicle architectures. Companies in the US are expanding validation programs to meet evolving standards in safety, compliance, and digital system integrity. Significant advancements in battery development, electrified platforms, and next-generation drivetrain systems are helping accelerate the adoption of HIL environments to reduce costs tied to physical prototyping and to shorten engineering timelines.

Prominent participants in the Hardware-in-the-Loop (HIL) Testing Market include Aptiv, dSPACE, Elektrobit, Emerson, IPG Automotive, Lynx Software Technologies, MathWorks, Robert Bosch, Typhoon HIL, and Vector Informatik. Key strategies used by companies in the hardware-in-the-loop testing market focus on expanding technological depth and strengthening collaborative development. Providers are investing in enhanced real-time computing clusters, higher-capacity interface boards, and advanced processing architectures to support increasingly complex simulations. Many organizations are forming alliances with software platforms to ensure seamless integration across modeling, testing, and automation workflows. Firms are also scaling production capabilities, broadening service portfolios, and introducing modular HIL systems that accommodate evolving design demands.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Offering

- 2.2.4 Testing phase

- 2.2.5 End use

- 2.3 TAM Analysis, 2026-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Silicon & Core Technology Providers

- 3.1.1.2 Platform & System Suppliers

- 3.1.1.3 Software & Model Providers

- 3.1.1.4 System Integrators & Professional Services

- 3.1.2 Profit margin analysis

- 3.1.2.1 Silicon & Core Technology Providers

- 3.1.2.2 Platform & System Suppliers

- 3.1.2.3 Software & Model Providers

- 3.1.2.4 System Integrators & Services

- 3.1.3 Cost Structure

- 3.1.4 Value Addition at Each Stage

- 3.1.5 Factors Affecting the Value Chain

- 3.1.6 Ecosystem Disruptions

- 3.1.1 Supplier landscape

- 3.2 Industry Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 electric vehicle proliferation and battery system validation requirements analysis

- 3.2.1.2 ADAS/autonomous vehicle complexity and software-defined vehicle architecture

- 3.2.1.3 regulatory mandates and functional safety standards (ISO 26262, IEC 61508, DO-178C)

- 3.2.1.4 power electronics and renewable energy grid integration

- 3.2.1.5 cost reduction imperative and demonstrated ROI from virtual validation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital investment and extended payback periods for SMEs

- 3.2.2.2 Skilled workforce shortage and knowledge transfer challenges

- 3.2.2.3 Model fidelity and validation challenges

- 3.2.3 Market Opportunities

- 3.2.3.1 Cloud-based HIL and hardware-in-the-loop-as-a-service (HILaaS)

- 3.2.3.2 AI/ML-driven test automation and scenario generation

- 3.2.3.3 Digital twin integration and lifecycle validation

- 3.2.3.4 Asia-pacific market expansion and localization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America Regulatory Landscape

- 3.4.1.1 United States: Federal and State-Level Requirements

- 3.4.1.2 Canada: Harmonization with U.S. Standards

- 3.4.2 Europe Regulatory Landscape

- 3.4.2.1 European Union: comprehensive type approval and cybersecurity mandates

- 3.4.2.2 United Kingdom: post-brexit regulatory divergence

- 3.4.3 Asia Pacific Regulatory Landscape

- 3.4.3.1 China: domestic standards and data localization

- 3.4.3.2 Japan: quality standards and automotive excellence

- 3.4.3.3 India: emerging market with rapid regulatory evolution

- 3.4.3.4 South korea: advanced technology and export focus

- 3.4.4 Latin America Regulatory Landscape

- 3.4.4.1 Brazil: regional leader with localization requirements

- 3.4.4.2 Mexico: USMCA integration and automotive manufacturing hub

- 3.4.5 Middle East & Africa Regulatory Landscape

- 3.4.5.1 UAE & Saudi Arabia: ambitious technology adoption

- 3.4.5.2 South Africa: regional manufacturing hub

- 3.4.6 Cross-regional regulatory trends and strategic implications

- 3.4.1 North America Regulatory Landscape

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 FPGA-accelerated real-time simulation platforms

- 3.7.1.2 Model-based design (MBD) & simulation toolchains

- 3.7.1.3 Modular PXI/EtherCAT-based HIL architectures

- 3.7.1.4 Certified safety & compliance toolchains

- 3.7.2 Emerging technologies

- 3.7.2.1 Cloud-native HIL platforms & hil-as-a-service (HILaaS)

- 3.7.2.2 AI/ML-driven test automation & scenario generation

- 3.7.2.3 Digital twin integration for lifecycle validation

- 3.7.2.4 Cybersecurity validation & secure OTA update testing

- 3.7.1 Current technological trends

- 3.8 Patent analysis

- 3.9 Cost breakdown analysis

- 3.10 Trade flow analysis

- 3.10.1 Import market dynamics

- 3.10.1.1 Global import patterns

- 3.10.1.2 Trade barriers and localization

- 3.10.2 Export market structure

- 3.10.3 Export barriers and incentives

- 3.10.4 Trade flow trends & strategic implications

- 3.10.1 Import market dynamics

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practice adoption

- 3.11.2 Waste reduction innovation

- 3.11.3 Energy efficiency optimization

- 3.11.4 Environmental initiative impact

- 3.12 Use cases

- 3.12.1 Iron bird testing

- 3.12.2 Missile development

- 3.12.3 Autonomous drone testing

- 3.12.4 ADAS and autonomous driving

- 3.12.5 Electromobility and electric drives

- 3.12.6 Power grids

- 3.12.7 Vehicle dynamics

- 3.12.8 Virtual vehicle

- 3.12.9 Test benches

- 3.12.10 Real driving emissions (RDE)

- 3.13 Best case scenarios

- 3.13.1 Full lifecycle digital twin-HIL integration

- 3.13.2 Cloud-native HILaaS for global collaboration

- 3.13.3 AI/ML-driven autonomous validation

- 3.13.4 PHIL for renewable grid integration

- 3.13.5 Modular, upgradable, circular HIL architectures

- 3.14 FPGA systems used by major competitors in HIL market

- 3.14.1 Performance & application fit

- 3.14.2 Scalability, modularity & lifecycle cost

- 3.14.3 Regulatory & certification advantage

- 3.14.4 Ecosystem & integration

- 3.14.5 Regional & regulatory differentiation

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 I/O interfaces

- 5.2.1.1 PCIe-based I/O interfaces

- 5.2.1.1.1 Standard PCIe cards

- 5.2.1.1.2 High-speed DAQ modules

- 5.2.1.1.3 Custom FPGA-integrated PCIe solutions

- 5.2.1.2 FPGA-based I/O solutions

- 5.2.1.2.1 Intel (Altera) Arria-based interface modules

- 5.2.1.2.2 Xilinx Zynq-based interface modules

- 5.2.1.2.3 FPGA I/O expansion boards

- 5.2.1.2.4 Real-time logic control & signal conditioning interfaces

- 5.2.1.3 Ethernet-based and EtherCAT interfaces

- 5.2.1.3.1 Industrial ethernet (GigE, 10GigE, TSN-enabled)

- 5.2.1.3.2 EtherCAT master/slave modules

- 5.2.1.3.3 Distributed I/O nodes with EtherCAT

- 5.2.1.3.4 Time-synchronized communication modules

- 5.2.1.1 PCIe-based I/O interfaces

- 5.2.2 Processors

- 5.2.3 Real-time simulators

- 5.2.4 Data acquisition systems

- 5.2.5 Others

- 5.2.1 I/O interfaces

- 5.3 Software

- 5.4 Services

- 5.4.1 Professional services

- 5.4.2 Managed services

Chapter 6 Market Estimates & Forecast, By Offering, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.1.1 Open loop

- 6.1.2 Close loop

Chapter 7 Market Estimates & Forecast, By Testing phase, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Design validation

- 7.3 Integration testing

- 7.4 Acceptance testing

- 7.5 Manufacturing testing

- 7.6 Performance testing

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Aerospace

- 8.3 Defence

- 8.4 Railway

- 8.5 Power electronics

- 8.6 Automotive

- 8.7 Medical devices

- 8.8 Renewable energy systems

- 8.9 Telecom and networking

- 8.10 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 MathWorks

- 10.1.2 National Instruments

- 10.1.3 dSPACE

- 10.1.4 Vector Informatik

- 10.1.5 Spirent Communications

- 10.1.6 Wind River

- 10.1.7 Robert Bosch

- 10.1.8 Emerson

- 10.2 Regional players

- 10.2.1 ADVANTECH

- 10.2.2 APTIV

- 10.2.3 Wabtec

- 10.2.4 ETAS

- 10.2.5 Hinduja Tech

- 10.2.6 Elektrobit

- 10.3 Niche/emerging players

- 10.3.1 ADD2

- 10.3.2 Concurrent Real-Time

- 10.3.3 IPG Automotive

- 10.3.4 Lynx Software Technologies

- 10.3.5 Opal-RT Technologies

- 10.3.6 Plexim

- 10.3.7 RealTime Wave

- 10.3.8 Speedgoat

- 10.3.9 Typhoon HIL