|

市場調查報告書

商品編碼

1885821

張量處理單元 (TPU) 市場機會、成長促進因素、產業趨勢分析及預測(2025-2034 年)Tensor Processing Unit (TPU) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

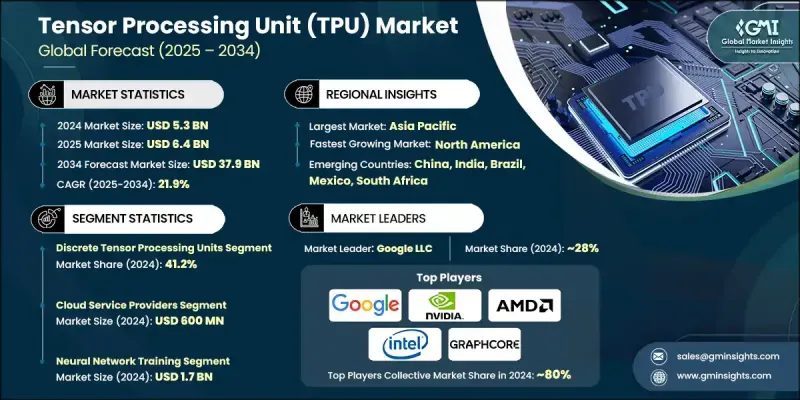

2024 年全球張量處理單元 (TPU) 市值為 53 億美元,預計到 2034 年將以 21.9% 的複合年成長率成長至 379 億美元。

人工智慧 (AI) 和機器學習 (ML) 在醫療保健、金融、汽車和機器人等行業的廣泛應用推動了這一成長。 TPU 提供高速處理和節能效能,使其非常適合深度學習應用。雲端運算基礎設施的快速擴張和對即時分析日益成長的需求進一步加速了 TPU 的普及。各行各業對可擴展、高效能 AI 解決方案的需求日益成長,而 TPU 正成為現代資料中心和邊緣運算框架不可或缺的一部分。 TPU 針對深度學習工作負載進行了最佳化,可提供更快的訓練和推理速度,這對於即時決策和智慧自動化至關重要。領先的雲端服務供應商正在將 TPU 嵌入到其平台中,使企業能夠有效地利用 AI。隨著企業向雲端系統轉型,像 TPU 這樣的高效能、高能源效率處理器對於降低營運成本和加速資料處理至關重要。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 53億美元 |

| 預測值 | 379億美元 |

| 複合年成長率 | 21.9% |

到2024年,離散張量處理單元(TPU)市佔率將達到41.2%。離散TPU憑藉其卓越的性能和處理複雜AI任務的靈活性而佔據主導地位。這些獨立單元專為深度學習工作負載而設計,可為企業和資料中心應用提供高運算吞吐量和可擴展性。它們無需依賴CPU或GPU即可相容於各種硬體配置,這增強了它們在大規模AI訓練和推理中的適用性,從而推動了其在雲端運算和高效能運算環境中的廣泛應用。

預計到2024年,雲端服務供應商市場規模將達6億美元。這些供應商憑藉其為企業和開發者提供的可擴展、高效能人工智慧基礎設施,佔據了市場主導地位。透過將TPU整合到雲端平台中,他們無需大量前期投資即可經濟高效地存取先進的機器學習功能。憑藉強大的全球資料中心和對多種人工智慧框架的支持,雲端服務供應商正在加速各行業人工智慧的普及應用。基於TPU的雲端服務的持續創新進一步鞏固了他們在市場上的領先地位。

2024年,北美張量處理單元(TPU)市佔率達40.2%。該地區的成長主要得益於對高效能運算的需求不斷成長,以支援人工智慧和機器學習應用。雲端服務、資料中心的擴張以及深度學習技術的進步是主要的成長因素。領先科技公司對TPU基礎設施的投資正在推動人工智慧工作負載的成長。此外,醫療保健、金融和汽車等行業對節能處理和即時資料處理的需求日益成長,也促進了北美市場的擴張。

全球張量處理單元 (TPU) 市場的主要參與者包括 SambaNova Systems, Inc.、Arm Holdings plc、Graphcore Ltd.、華為技術有限公司、Tenstorrent Inc.、富士通有限公司、亞馬遜網路服務公司、英特爾公司、寒武紀科技有限公司、微軟公司、高通技術公司、百度公司、有限責任公司、寒武紀科技公司、微軟公司、高通技術公司、百度公司、有限責任公司、DIBence公司Inc.、惠普企業公司、Synopsys, Inc. 和英偉達公司。這些企業正利用多種策略來鞏固其市場地位。它們大力投資研發,以提升 TPU 的性能和能源效率。策略合作、併購拓展了它們的市場覆蓋範圍,並實現了與雲端平台和企業平台的整合。此外,這些企業也致力於拓展產品組合,以滿足多樣化的人工智慧和機器學習需求。優先考慮永續性和節能解決方案有助於提升競爭力。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 產業影響因素

- 成長促進因素

- 對人工智慧和機器學習應用的需求不斷成長

- 雲端運算服務的日益普及

- 對深度學習技術的投資不斷增加

- 半導體技術的進步

- 需要強大的運算能力來處理大規模資料處理任務

- 產業陷阱與挑戰

- TPU硬體的初始投資成本較高

- TPU程式設計領域熟練專業人員數量有限

- 市場機遇

- 新興經濟體TPU市場的擴張

- 為特定產業開發客製化TPU解決方案

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 美國

- 加拿大

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 北美洲

- 技術格局

- 當前趨勢

- 新興技術

- 管道分析

- 未來市場趨勢

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依產品分類,2021-2034年

- 主要趨勢

- 離散張量處理單元

- 晶圓級人工智慧處理器

- 智慧處理單元

- 整合神經處理單元

第6章:市場估算與預測:依最終用途產業分類,2021-2034年

- 主要趨勢

- 政府與國防

- 研究機構

- 雲端服務供應商

- 企業技術

- 其他

第7章:市場估計與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 神經網路訓練

- 人工智慧推理處理

- 科學計算

- 邊緣人工智慧

第8章:市場估算與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Google LLC (USA)

- NVIDIA Corporation (USA)

- Advanced Micro Devices, Inc. (AMD) (USA)

- Intel Corporation (USA)

- Microsoft Corporation (USA)

- Amazon Web Services, Inc. (USA)

- Huawei Technologies Co., Ltd. (China)

- Alibaba Group Holding Limited (China)

- Baidu, Inc. (China)

- Graphcore Ltd. (UK)

- SambaNova Systems, Inc. (USA)

- Tenstorrent Inc. (Canada)

- Cambricon Technologies Corporation Limited (China)

- Qualcomm Technologies, Inc. (USA)

- IBM Corporation (USA)

- Arm Holdings plc (UK)

- Cadence Design Systems, Inc. (USA)

- Synopsys, Inc. (USA)

- Fujitsu Limited (Japan)

- Hewlett Packard Enterprise Company (USA)

The Global Tensor Processing Unit (TPU) Market was valued at USD 5.3 billion in 2024 and is estimated to grow at a CAGR of 21.9% to reach USD 37.9 billion by 2034.

The growth is fueled by the widespread adoption of artificial intelligence (AI) and machine learning (ML) across sectors such as healthcare, finance, automotive, and robotics. TPUs provide high-speed processing and energy-efficient performance, making them highly suited for deep learning applications. The rapid expansion of cloud computing infrastructure and the rising demand for real-time analytics are further accelerating TPU adoption. Industries increasingly require scalable, high-performance AI solutions, and TPUs are becoming integral to modern data centers and edge computing frameworks. Optimized for deep learning workloads, TPUs deliver faster training and inference times, essential for real-time decision-making and intelligent automation. Leading cloud service providers are embedding TPUs into their platforms, enabling enterprises to leverage AI efficiently. As businesses transition to cloud-based systems, high-performance and energy-efficient processors like TPUs are critical for reducing operational costs and accelerating data processing.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.3 Billion |

| Forecast Value | $37.9 Billion |

| CAGR | 21.9% |

The discrete tensor processing units segment accounted for a 41.2% share in 2024. Discrete TPUs dominate due to their exceptional performance and flexibility in managing complex AI tasks. These standalone units are engineered for deep learning workloads, offering high computational throughput and scalability for enterprise and data center applications. Their compatibility with diverse hardware setups without relying on CPUs or GPUs enhances their suitability for large-scale AI training and inference, driving widespread adoption across cloud and high-performance computing environments.

The cloud service providers segment generated USD 600 million in 2024. These providers hold a dominant position as they offer scalable, high-performance AI infrastructure for businesses and developers. By integrating TPUs into cloud platforms, they provide cost-effective access to advanced machine learning capabilities without requiring significant upfront investment. With robust global data centers and support for multiple AI frameworks, cloud service providers are accelerating AI adoption across industries. Continuous innovation in TPU-based cloud services strengthens their leadership in the market.

North America Tensor Processing Unit (TPU) Market held a 40.2% share in 2024. Growth in this region is driven by increasing demand for high-performance computing to support AI and machine learning applications. The expansion of cloud-based services, data centers, and advancements in deep learning technologies are major growth factors. Investments by leading tech companies in TPU infrastructure are boosting AI workloads. Furthermore, the growing need for energy-efficient processing and real-time data handling in sectors such as healthcare, finance, and automotive is enhancing market expansion in North America.

Key players in the Global Tensor Processing Unit (TPU) Market include SambaNova Systems, Inc., Arm Holdings plc, Graphcore Ltd., Huawei Technologies Co., Ltd., Tenstorrent Inc., Fujitsu Limited, Amazon Web Services, Inc., Intel Corporation, Cambricon Technologies Corporation Limited, Microsoft Corporation, Qualcomm Technologies, Inc., Baidu, Inc., Google LLC, Advanced Micro Devices, Inc. (AMD), IBM Corporation, Alibaba Group Holding Limited, Cadence Design Systems, Inc., Hewlett Packard Enterprise Company, Synopsys, Inc., and NVIDIA Corporation. Companies in the Global Tensor Processing Unit (TPU) Market are leveraging multiple strategies to strengthen their foothold. They are heavily investing in research and development to enhance TPU performance and energy efficiency. Strategic partnerships, mergers, and acquisitions expand their market reach and enable integration with cloud and enterprise platforms. Companies are also focusing on broadening their product portfolios to meet diverse AI and machine learning requirements. Prioritizing sustainability and energy-efficient solutions improves competitiveness.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product Trends

- 2.2.2 End use Industry Trends

- 2.2.3 Application Trends

- 2.2.4 Regional Trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for artificial intelligence and machine learning applications

- 3.2.1.2 Growing adoption of cloud computing services

- 3.2.1.3 Rising investments in deep learning technologies

- 3.2.1.4 Advancements in semiconductor technology

- 3.2.1.5 Need for high computational power for handling large-scale data processing tasks

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment cost for TPU hardware

- 3.2.2.2 Limited availability of skilled professionals in TPU programming

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of TPU market in emerging economies

- 3.2.3.2 Development of customized TPU solutions for specific industries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.4.1 North America

- 3.5 Technology landscape

- 3.5.1 Current trends

- 3.5.2 Emerging technologies

- 3.6 Pipeline analysis

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 Middle East and Africa

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Bn)

- 5.1 Key trends

- 5.2 Discrete Tensor Processing Units

- 5.3 Wafer-Scale AI Processors

- 5.4 Intelligence Processing Units

- 5.5 Integrated Neural Processing Units

Chapter 6 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 ($ Bn)

- 6.1 Key trends

- 6.2 Government & Defense

- 6.3 Research Institutions

- 6.4 Cloud Service Providers

- 6.5 Enterprise Technology

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Bn)

- 7.1 Key trends

- 7.2 Neural Network Training

- 7.3 AI Inference Processing

- 7.4 Scientific Computing

- 7.5 Edge AI

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Bn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Google LLC (USA)

- 9.2 NVIDIA Corporation (USA)

- 9.3 Advanced Micro Devices, Inc. (AMD) (USA)

- 9.4 Intel Corporation (USA)

- 9.5 Microsoft Corporation (USA)

- 9.6 Amazon Web Services, Inc. (USA)

- 9.7 Huawei Technologies Co., Ltd. (China)

- 9.8 Alibaba Group Holding Limited (China)

- 9.9 Baidu, Inc. (China)

- 9.10 Graphcore Ltd. (UK)

- 9.11 SambaNova Systems, Inc. (USA)

- 9.12 Tenstorrent Inc. (Canada)

- 9.13 Cambricon Technologies Corporation Limited (China)

- 9.14 Qualcomm Technologies, Inc. (USA)

- 9.15 IBM Corporation (USA)

- 9.16 Arm Holdings plc (UK)

- 9.17 Cadence Design Systems, Inc. (USA)

- 9.18 Synopsys, Inc. (USA)

- 9.19 Fujitsu Limited (Japan)

- 9.20 Hewlett Packard Enterprise Company (USA)