|

市場調查報告書

商品編碼

1885794

庫欣氏症候群診斷及治療市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Cushing's Syndrome Diagnostics and Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

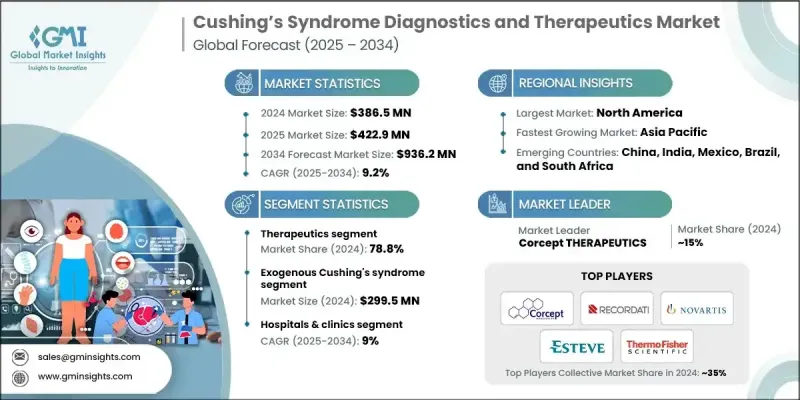

2024 年全球庫欣氏症候群診斷與治療市場價值為 3.865 億美元,預計到 2034 年將以 9.2% 的複合年成長率成長至 9.362 億美元。

由於疾病盛行率上升、監管激勵措施不斷加強以及對下一代皮質醇調節藥物研究投入的增加,市場正在成長,這些因素也促進了藥物的普及應用。新的診斷方法提高了高皮質醇血症的檢測準確性,有助於最大限度地減少誤診,並改善患者的長期預後。現代內分泌治療正朝著精準醫療的方向發展,為臨床醫生提供更好的工具來評估疾病嚴重程度並制定有效的治療方案。旨在糾正荷爾蒙失衡的創新正在改變那些需要更安全、更永續治療方案的患者的治療方式。傳統的介入措施常常為復發性或難治性疾病患者帶來挑戰,這促使人們尋求能夠提供更可預測和耐受性更好的長期療效的新型醫療替代方案。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 3.865億美元 |

| 預測值 | 9.362億美元 |

| 複合年成長率 | 9.2% |

2024年,治療類藥物市佔率將達到78.8%,因為對於無法接受手術或面臨疾病復發的患者而言,藥物治療仍然至關重要。標靶藥物的普及進一步鞏固了該領域的領先地位,這些藥物能夠提高整體治療的一致性並改善慢性病管理效果。這些藥物透過調節皮質醇活性發揮作用,使臨床醫生能夠在更長的時間內控制症狀,並減少併發症。

2024年,內源性庫欣氏症候群市場規模達到8,700萬美元,預計2034年將以8.6%的複合年成長率成長。該領域的成長得益於臨床意識的提高、檢測技術的進步以及對潛在疾病病因的更精準鑑別。專科治療方案的研發和相關監管政策的支持,使得更多患有複雜內分泌疾病的患者能夠獲得治療。

2024年,美國庫欣氏症候群診斷與治療市場規模預估為1.537億美元。完善的監管體系、有利的報銷機制以及包括諾華、Corcept Therapeutics、輝瑞、Recordati、梯瓦、賽默飛世爾科技等在內的眾多製藥創新企業,以及其他行業貢獻者,共同推動了市場的發展。肥胖症和糖尿病等內分泌相關疾病發生率的上升,持續擴大美國庫欣氏症候群患者族群。

全球庫欣氏症候群診斷與治療市場的主要參與者包括Labcorp、Esteve、Salimetrics、ALPCO、Lucichem Pharma、DiaMetra以及其他業界知名企業。庫欣氏症候群診斷和治療領域的領導者正透過優先投入持續研發、爭取監管激勵以及與臨床研究機構和學術夥伴建立策略合作關係來擴大市場佔有率。這些企業正透過專注於開發選擇性皮質醇調節療法以及利用先進的檢測技術來提高診斷準確性來豐富產品組合。此外,這些企業還透過最佳化商業化策略、爭取有利的報銷政策以及擴大患者支持計畫來增強市場准入,從而鼓勵患者長期堅持治療。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 產業影響因素

- 成長促進因素

- 庫欣氏症候群發生率上升

- 擴大孤兒藥認定範圍和監管激勵措施

- 診斷技術的進步

- 增加選擇性皮質醇調節劑的研發投入

- 產業陷阱與挑戰

- 高昂的治療費用

- 診斷複雜性和檢測延遲

- 市場機遇

- 個人化醫療的日益普及

- 成長促進因素

- 成長潛力分析

- 投資環境

- 管道分析

- 未來市場趨勢

- 報銷方案

- 監管環境

- 技術格局

- 目前技術

- 新興技術

- 差距分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 擴張計劃

第5章:市場估算與預測:依類別分類,2021-2034年

- 主要趨勢

- 療法

- 手術

- 經蝶竇手術

- 腎上腺切除術

- 藥物

- 腦下垂體標靶藥物

- 腎上腺類固醇生成抑制劑

- 糖皮質激素受體拮抗劑

- 其他藥物

- 放射治療

- 手術

- 診斷

- 下岩竇取樣

- 深夜唾液皮質醇測試

- 24小時尿液和血液皮質醇檢測

- 影像檢查

- 其他診斷測試

第6章:市場估計與預測:依疾病類型分類,2021-2034年

- 主要趨勢

- 外源性庫欣氏症候群

- 內源性庫欣氏症候群

第7章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 醫院和診所

- 家庭護理機構

- 診斷中心

- 其他最終用途

第8章:市場估算與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- ALPCO

- Corcept THERAPEUTICS

- DiaMetra

- ESTEVE

- labcorp

- Lucichem Pharma

- NOVARTIS

- Pfizer

- RECORDATI

- SALIMETRICS

- teva

- Thermo Fisher SCIENTIFIC

The Global Cushing's Syndrome Diagnostics and Therapeutics Market was valued at USD 386.5 million in 2024 and is estimated to grow at a CAGR of 9.2% to reach USD 936.2 million by 2034.

The market is growing owing to the rising disease prevalence, expanding regulatory incentives, and increased investment in next-generation cortisol-modulating research, which strengthens adoption. The newer diagnostic approaches are improving accuracy in detecting hypercortisolemia, helping to minimize misdiagnosis and enhance long-term patient outcomes. The modern endocrine care is shifting toward precision-driven management, offering clinicians better tools for evaluating disease severity and determining effective treatment plans. The innovations aimed at correcting hormonal imbalance are transforming care for individuals who require safer, more sustainable therapeutic options. Traditional interventions often pose challenges for patients with recurring or difficult-to-treat conditions, which is driving interest in updated medical alternatives that offer more predictable and tolerable long-term outcomes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $386.5 Million |

| Forecast Value | $936.2 Million |

| CAGR | 9.2% |

The therapeutics category segment held 78.8% share in 2024 as medical management remains essential for individuals who cannot undergo surgical procedures or who face disease recurrence. The dominance of this segment is reinforced by broader access to targeted drug classes that improve overall treatment consistency and chronic care outcomes. These medicines provide mechanisms designed to regulate cortisol activity and allow clinicians to manage symptoms over extended periods with fewer complications.

The endogenous Cushing's syndrome segment generated USD 87 million in 2024 and is projected to grow at an 8.6% CAGR through 2034. The growth in this area is supported by heightened clinical awareness, advancements in testing, and better differentiation of underlying disease origins. The development of specialty treatments and supportive regulatory designations is enabling wider access for individuals with complex endocrine disorders.

United States Cushing's Syndrome Diagnostics and Therapeutics Market was valued at USD 153.7 million in 2024. The regulatory systems, supportive reimbursement pathways, and a strong base of pharmaceutical innovators, including Novartis, Corcept Therapeutics, Pfizer, Recordati, Teva, Thermo Fisher Scientific, and other industry contributors, strengthen market performance. Rising rates of endocrine-related disorders and conditions, such as obesity and diabetes, continue to broaden the national patient population.

Key companies active in the Global Cushing's Syndrome Diagnostics and Therapeutics Market include Labcorp, Esteve, Salimetrics, ALPCO, Lucichem Pharma, DiaMetra, and other established industry participants. Leading companies in the Cushing's syndrome diagnostics and therapeutics field are expanding their presence by prioritizing continuous research investment, pursuing regulatory incentives, and forming strategic collaborations with clinical research organizations and academic partners. Firms are enhancing product portfolios through focused development of selective cortisol-modulating therapies and by improving diagnostic accuracy through advanced assay technologies. Companies are strengthening market access by optimizing commercialization strategies, securing favorable reimbursement, and expanding patient-support programs to encourage long-term therapy adherence.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Category trends

- 2.2.3 Disease type trends

- 2.2.4 End Use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of Cushing’s syndrome

- 3.2.1.2 Expansion of orphan drug designations and regulatory incentives

- 3.2.1.3 Advancements in diagnostic technologies

- 3.2.1.4 Increasing R&D investments in selective cortisol modulators

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High treatment costs

- 3.2.2.2 Diagnostic complexity and delayed detection

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing adoption of personalized medicine

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Investment landscape

- 3.5 Pipeline analysis

- 3.6 Future market trends

- 3.7 Reimbursement scenario

- 3.8 Regulatory landscape

- 3.9 Technology landscape

- 3.9.1 Current technologies

- 3.9.2 Emerging technologies

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 Expansion plans

Chapter 5 Market Estimates and Forecast, By Category, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Therapeutics

- 5.2.1 Surgery

- 5.2.1.1 Transsphenoidal surgery

- 5.2.1.2 Adrenalectomy

- 5.2.2 Drugs

- 5.2.2.1 Pituitary-directed drugs

- 5.2.2.2 Adrenal steroidogenesis inhibitors

- 5.2.2.3 Glucocorticoid receptor antagonists

- 5.2.2.4 Other drugs

- 5.2.3 Radiation Therapy

- 5.2.1 Surgery

- 5.3 Diagnostics

- 5.3.1 Inferior petrosal sinus sampling

- 5.3.2 Late-night salivary cortisol test

- 5.3.3 24-hour urine & blood cortisol panels

- 5.3.4 Imaging tests

- 5.3.5 Other diagnostic tests

Chapter 6 Market Estimates and Forecast, By Disease Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Exogenous Cushing's syndrome

- 6.3 Endogenous Cushing's syndrome

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals & clinics

- 7.3 Homecare settings

- 7.4 Diagnostic centers

- 7.5 Other End Use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 ALPCO

- 9.2 Corcept THERAPEUTICS

- 9.3 DiaMetra

- 9.4 ESTEVE

- 9.5 labcorp

- 9.6 Lucichem Pharma

- 9.7 NOVARTIS

- 9.8 Pfizer

- 9.9 RECORDATI

- 9.10 SALIMETRICS

- 9.11 teva

- 9.12 Thermo Fisher SCIENTIFIC