|

市場調查報告書

商品編碼

1885788

基於區塊鏈的醫療記錄系統市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Blockchain-based Medical Record System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

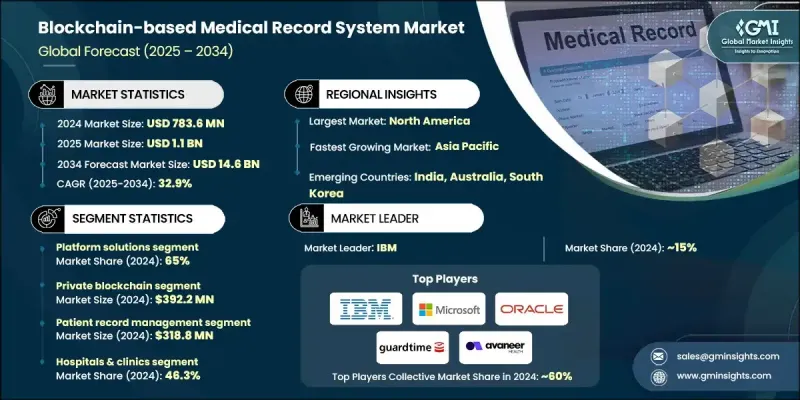

2024 年全球基於區塊鏈的醫療記錄系統市場價值為 7.836 億美元,預計到 2034 年將以 32.9% 的複合年成長率成長至 146 億美元。

市場成長的促進因素包括:對以患者為中心的醫療模式的日益重視、對無縫醫療資料互通性的需求,以及網路安全漏洞帶來的成本和風險不斷增加。電子健康記錄 (EHR) 和整合互通性解決方案的普及,正在加速對安全、透明資料管理的需求。區塊鏈技術在臨床試驗中也越來越受歡迎,用於確保資料的完整性、透明度和可審計性。醫療服務提供者優先考慮能夠賦予患者對其個人資料控制權,同時實現安全、基於許可的資料共享的解決方案。區塊鏈的去中心化架構和加密保護能夠減少漏洞、降低網路風險,並為醫療機構提供高水準的資料安全性、合規性和營運效率。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 7.836億美元 |

| 預測值 | 146億美元 |

| 複合年成長率 | 32.9% |

到 2024 年,平台解決方案領域佔據了 65% 的市場。這些平台為醫療資料的安全儲存、加密和去中心化存取提供了底層基礎設施,實現了醫院、保險公司和患者之間的互通性,同時遵守了 HIPAA 和 GDPR 等隱私法規。

2024年,私有區塊鏈市場規模達3.922億美元。私有區塊鏈限制只有授權用戶才能訪問,提供高速交易、更高安全性和集中控制,使其成為管理敏感患者資訊的醫療機構的理想選擇。醫院和保險公司傾向於使用私人網路,以符合監管框架並確保資料機密性。

2024年,北美基於區塊鏈的醫療記錄系統市佔率達到60.1%,預計在預測期內將維持顯著成長。該地區強大的醫療基礎設施、嚴格的監管以及對數位醫療和遠距醫療解決方案的早期應用,推動了對支援區塊鏈的互通醫療記錄系統的需求。醫院、保險公司和研究機構為保護患者資料、減少詐欺和實現無縫資料共享而進行的投資,進一步促進了市場成長。

全球基於區塊鏈的醫療記錄系統市場的主要參與者包括微軟、甲骨文公司、IBM、Avaneer HEALTH、burstIQ、Chronicled、embleema、Factom、Guardtime、Patientory Inc.、SOLULAB 和 SOLVE CARE。各公司致力於區塊鏈架構和資料加密方面的創新,以增強安全性、互通性和患者對醫療記錄的控制權。與醫院、保險公司和醫療技術提供者建立策略合作夥伴關係,使各公司能夠將區塊鏈解決方案無縫整合到現有的醫療保健生態系統中。對平台可擴展性、雲端整合和人工智慧分析的研發投入,增強了產品功能並促進了應用。市場參與者也在進行區域擴張,瞄準資料隱私法規嚴格的高需求地區。併購有助於整合技術、拓展產品組合併提升競爭地位。各公司強調合規性,遵守 HIPAA 和 GDPR 法規,並獲得相關認證,以確保客戶對系統的可靠性。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 產業影響因素

- 成長促進因素

- 醫療保健資料外洩事件及網路安全成本不斷上升

- 以病人為中心的照護模式的需求日益成長

- 遠距醫療和遠距護理的興起

- 對無縫健康資料互通性的需求日益成長

- 產業陷阱與挑戰

- 監管的不確定性和合規性問題

- 技術可擴展性和技能短缺

- 機會

- 人工智慧與區塊鏈融合助力進階分析

- 與物聯網醫療和遠端監控系統的整合

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 技術與創新格局

- 去中心化身分認同和自主解決方案

- 零知識證明與隱私保護技術

- 抗量子密碼學與安全

- 邊緣運算與物聯網整合

- 智慧合約的演進與自動化

- 投資環境

- 醫療服務模式轉型

- 新興用例

- 波特的分析

- PESTEL 分析

- 差距分析

- 未來市場趨勢

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依產品類型分類,2021-2034年

- 主要趨勢

- 平台解決方案

- 服務

第6章:市場估算與預測:依類型分類,2021-2034年

- 主要趨勢

- 私有區塊鏈

- 聯盟/許可型區塊鏈

- 公共區塊鏈

- 混合區塊鏈

第7章:市場估計與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 病患記錄管理

- 臨床試驗資料共享

- 保險索賠和詐欺檢測

- 其他應用

第8章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 醫院和診所

- 製藥公司

- 保險公司

- 其他最終用途

第9章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 世界其他地區(RoW)

第10章:公司簡介

- Avaneer HEALTH

- burstIQ

- Chronicled

- embleema

- Factom

- Guardtime

- IBM

- Microsoft

- Oracle Corporation

- patientory inc.

- SOLULAB

- SOLVE CARE

The Global Blockchain-based Medical Record System Market was valued at USD 783.6 million in 2024 and is estimated to grow at a CAGR of 32.9% to reach USD 14.6 billion by 2034.

Market growth is fueled by the rising focus on patient-centric care models, the need for seamless healthcare data interoperability, and the increasing costs and risks associated with cybersecurity breaches. The adoption of electronic health records (EHR) and integrated interoperability solutions is accelerating demand for secure, transparent data management. Blockchain technology is also gaining traction in clinical trials for ensuring data integrity, transparency, and auditability. Healthcare providers are prioritizing solutions that empower patients with control over their personal data while enabling secure, permission-based sharing. The decentralized architecture and cryptographic protection of blockchain reduce vulnerabilities, mitigate cyber risks, and provide healthcare organizations with a high level of data security, compliance assurance, and operational efficiency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $783.6 Million |

| Forecast Value | $14.6 Billion |

| CAGR | 32.9% |

The platform solutions segment held a share of 65% in 2024. These platforms provide the underlying infrastructure for secure storage, encryption, and decentralized access of medical data, enabling interoperability between hospitals, insurers, and patients while adhering to privacy regulations like HIPAA and GDPR.

The private blockchain segment generated USD 392.2 million in 2024. Private blockchains restrict access to authorized users, offering high transaction speed, greater security, and centralized control, which makes them ideal for healthcare organizations managing sensitive patient information. Hospitals and insurers prefer private networks for compliance with regulatory frameworks and to ensure data confidentiality.

North America Blockchain-based Medical Record System Market held 60.1% share in 2024 and is expected to maintain significant growth during the forecast period. The region's strong healthcare infrastructure, strict regulations, and early adoption of digital health and telehealth solutions are driving demand for blockchain-enabled interoperable medical record systems. Investments from hospitals, insurers, and research institutions to protect patient data, reduce fraud, and enable seamless data sharing have further strengthened market growth.

Key players in the Global Blockchain-based Medical Record System Market include Microsoft, Oracle Corporation, IBM, Avaneer HEALTH, burstIQ, Chronicled, embleema, Factom, Guardtime, Patientory Inc., SOLULAB, and SOLVE CARE. Companies are focusing on innovation in blockchain architecture and data encryption to enhance security, interoperability, and patient control over medical records. Strategic partnerships with hospitals, insurers, and health-tech providers allow companies to integrate blockchain solutions seamlessly into existing healthcare ecosystems. Investment in R&D for platform scalability, cloud integration, and AI-enabled analytics strengthens product offerings and supports adoption. Market players are also expanding regionally, targeting high-demand areas with strict data privacy regulations. Mergers and acquisitions help consolidate technology, broaden portfolios, and improve competitive positioning. Companies emphasize regulatory compliance, HIPAA and GDPR adherence, and certification to assure clients of system reliability.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Offering trends

- 2.2.3 Type trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising healthcare data breaches & cybersecurity costs

- 3.2.1.2 Growing demand for patient-centric care models

- 3.2.1.3 Rise in telehealth and remote care

- 3.2.1.4 Increasing need for seamless health data interoperability

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory uncertainty and compliance concerns

- 3.2.2.2 Technical scalability and skill shortage

- 3.2.3 Opportunities

- 3.2.3.1 AI-blockchain convergence for advanced analytics

- 3.2.3.2 Integration with IoMT and remote monitoring systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape

- 3.5.1 Decentralized identity & self-sovereign solutions

- 3.5.2 Zero-knowledge proofs & privacy-preserving technologies

- 3.5.3 Quantum-resistant cryptography & security

- 3.5.4 Edge computing & IoT integration

- 3.5.5 Smart contract evolution & automation

- 3.6 Investment landscape

- 3.7 Healthcare delivery model transformation

- 3.8 Emerging use cases

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Gap analysis

- 3.12 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Offering, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Platform solutions

- 5.3 Services

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Private blockchain

- 6.3 Consortium/Permissioned blockchain

- 6.4 Public blockchain

- 6.5 Hybrid blockchain

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Patient record management

- 7.3 Clinical trial data sharing

- 7.4 Insurance claim & fraud detection

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals and clinics

- 8.3 Pharmaceutical companies

- 8.4 Insurance providers

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Rest of the world (RoW)

Chapter 10 Company Profiles

- 10.1 Avaneer HEALTH

- 10.2 burstIQ

- 10.3 Chronicled

- 10.4 embleema

- 10.5 Factom

- 10.6 Guardtime

- 10.7 IBM

- 10.8 Microsoft

- 10.9 Oracle Corporation

- 10.10 patientory inc.

- 10.11 SOLULAB

- 10.12 SOLVE CARE