|

市場調查報告書

商品編碼

1876810

肽類藥物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Peptide Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

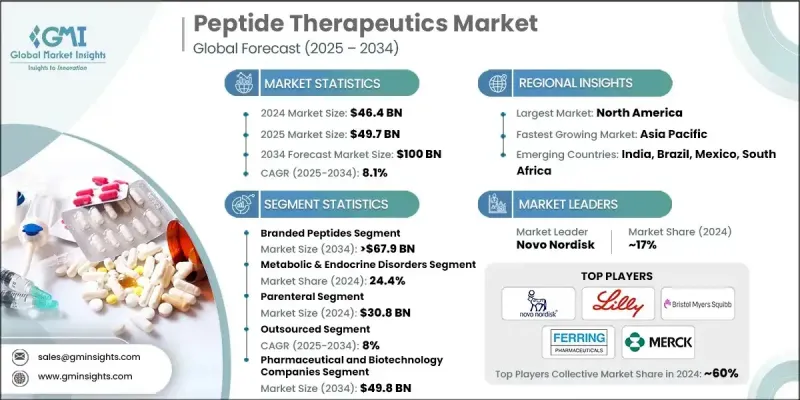

2024 年全球胜肽類藥物市場價值為 464 億美元,預計到 2034 年將以 8.1% 的複合年成長率成長至 1000 億美元。

慢性病和生活型態相關疾病(包括糖尿病、癌症和肥胖症)的日益普遍是推動胜肽類藥物市場成長的重要因素。肽類藥物由短鏈胺基酸組成,針對特定的分子通路,與傳統療法相比,具有更高的療效和更低的副作用。這些療法已應用於多種治療領域,例如代謝失調、心血管疾病、胃腸道疾病、傳染病、癌症和罕見遺傳疾病。電子健康記錄、基於人工智慧的臨床決策工具和真實世界證據平台的整合正在重塑胜肽類藥物的研發、監測和處方模式。政府計畫和公私合作計畫提高了分子診斷、個人化醫療和罕見疾病治療的可及性,進一步加速了胜肽類藥物市場的成長。隨著對生物啟發式和精準醫療需求的不斷成長,肽類藥物憑藉其安全性、特異性和廣泛的治療潛力,正在成為現代醫療保健的關鍵解決方案。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 464億美元 |

| 預測值 | 1000億美元 |

| 複合年成長率 | 8.1% |

2024年,品牌胜肽類藥物市佔率預計將達到69.2%,這主要得益於其對創新、高特異性和已證實的臨床療效的重視。這些療法在治療複雜和慢性疾病方面越來越受歡迎,因為精準標靶和最小的脫靶效應至關重要。品牌胜肽類藥物受益於強大的研發管線、持續的製劑改良和先進的遞送機制,從而提升了患者的治療效果和療效的可靠性。

由於胜肽類藥物穩定性差、口服生物利用度低,靜脈注射、皮下注射或肌肉注射成為首選給藥途徑,因此,2024年腸外給藥市場規模預計將達到308億美元。腸外給藥可確保藥物快速吸收、劑量精準,並能有效治療代謝失調、癌症及罕見內分泌疾病等關鍵適應症。

預計到2024年,北美肽類藥物市場將佔據42.1%的佔有率。該地區的成長得益於先進的生物製藥基礎設施、早期法規核准、強勁的研發投入以及癌症、代謝紊亂和罕見患者病率的上升。美國和加拿大等國家品牌化和創新胜肽類藥物的開發,支撐了對標靶性強、低毒性治療的需求。

全球胜肽類藥物市場的主要參與者包括諾和諾德、PolyPeptide Group、Rhythm Pharmaceuticals、Ascendis Pharma、Zydus Lifesciences、Ferring Pharmaceuticals、阿斯特捷利康、X-GEN Pharmaceuticals、禮來公司、Repligen Corporation、賽諾菲、安進、百時施貴克、PeptiDam、PeptiDam、PeptiDam、PeptiDam、PeptiDam、PeptiDam、PeptiDam、PeptiDam、PeptiD這些公司正積極採取各種策略,例如投資研發以開發新型胜肽製劑、與生物技術新創公司合作以加速創新,以及建立策略聯盟以實現全球分銷。許多公司致力於拓展產品組合,以涵蓋罕見疾病和慢性病領域,同時提升高純度胜肽的生產能力。市場參與者正日益利用數位化平台和人工智慧技術進行精準藥物研發、病患監測和真實世界資料收集。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 每個階段的價值增加

- 影響價值鏈的因素

- 產業影響因素

- 成長促進因素

- 癌症發生率不斷上升

- 代謝和內分泌疾病發生率上升

- 加大對新型藥物研發的投入

- 肽類藥物的技術進步

- 產業陷阱與挑戰

- 藥品核准有嚴格的監理要求

- 藥物研發成本高昂

- 市場機遇

- 肽-藥物偶聯物和放射性標記肽的創新

- 擴大口服和長效胜肽製劑的供應

- 成長促進因素

- 成長潛力分析

- 監管環境

- 未來市場趨勢

- 技術格局

- 目前技術

- 新興技術

- 專利分析

- 管道分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依類型分類,2021-2034年

- 主要趨勢

- 品牌胜肽

- 通用胜肽

第6章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 代謝和內分泌紊亂

- 癌症

- 心血管疾病

- 胃腸道疾病

- 中樞神經系統疾病

- 呼吸系統疾病

- 疼痛管理

- 其他應用

第7章:市場估計與預測:依給藥途徑分類,2021-2034年

- 主要趨勢

- 腸外

- 口服

- 其他給藥途徑

第8章:市場估算與預測:依製造商類型分類,2021-2034年

- 主要趨勢

- 內部

- 外包

第9章:市場估算與預測:基於合成技術,2021-2034年

- 主要趨勢

- 液相肽合成(LPPS)

- 固相胜肽合成(SPPS)

- 混合技術

第10章:市場估計與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 醫院和診所

- 製藥和生物技術公司

- 其他最終用途

第11章:市場估計與預測:按地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- Amgen

- Ascendis Pharma

- AstraZeneca

- Bristol-Myers Squibb

- Eli Lilly and Company

- Ferring Pharmaceuticals

- Merck & Co.

- Novo Nordisk

- PeptiDream

- PolyPeptide Group

- Repligen Corporation

- Rhythm Pharmaceuticals

- Sanofi

- X-GEN Pharmaceuticals

- Zydus Lifesciences

The Global Peptide Therapeutics Market was valued at USD 46.4 billion in 2024 and is estimated to grow at a CAGR of 8.1% to reach USD 100 billion by 2034.

The increasing prevalence of chronic and lifestyle-related diseases, including diabetes, cancer, and obesity, is a significant growth driver. Peptide therapeutics, composed of short chains of amino acids, target specific molecular pathways, offering high efficacy and reduced side effects compared to conventional therapies. These treatments are applied across diverse therapeutic areas such as metabolic disorders, cardiovascular diseases, gastrointestinal conditions, infectious diseases, cancer, and rare genetic disorders. The integration of electronic health records, AI-based clinical decision-making tools, and real-world evidence platforms is reshaping the development, monitoring, and prescription of peptide therapies. Government programs and public-private partnerships enhancing access to molecular diagnostics, personalized medicine, and rare disease treatments further accelerate growth. With rising demand for biologically inspired and precision medicines, peptide therapeutics are emerging as critical solutions in modern healthcare due to their safety, specificity, and wide-ranging therapeutic potential.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $46.4 Billion |

| Forecast Value | $100 Billion |

| CAGR | 8.1% |

The branded peptides segment held a 69.2% share in 2024, driven by its strong focus on innovation, high specificity, and proven clinical efficacy. These therapies are increasingly preferred for the treatment of complex and chronic conditions, where precise targeting and minimal off-target effects are essential. Branded peptides benefit from robust research and development pipelines, continuous formulation improvements, and advanced delivery mechanisms, which enhance patient outcomes and therapeutic reliability.

The parenteral segment generated USD 30.8 billion in 2024, owing to the poor stability and low oral bioavailability of peptides, making intravenous, subcutaneous, or intramuscular administration the preferred delivery method. Parenteral delivery ensures rapid absorption, accurate dosing, and high efficacy for critical indications such as metabolic disorders, cancer, and rare endocrine conditions.

North America Peptide Therapeutics Market held a 42.1% share in 2024. Growth in the region is fueled by advanced biopharmaceutical infrastructure, early regulatory approvals, strong R&D investments, and the rising prevalence of cancer, metabolic disorders, and rare diseases. The development of branded and innovative peptide therapies in countries like the U.S. and Canada supports demand for targeted, low-toxicity treatments.

Key players in the Global Peptide Therapeutics Market include Novo Nordisk, PolyPeptide Group, Rhythm Pharmaceuticals, Ascendis Pharma, Zydus Lifesciences, Ferring Pharmaceuticals, AstraZeneca, X-GEN Pharmaceuticals, Eli Lilly and Company, Repligen Corporation, Sanofi, Amgen, Bristol-Myers Squibb, PeptiDream, and Merck & Co. Companies in the Peptide Therapeutics Market are adopting strategies such as investing in research and development to create novel peptide formulations, collaborating with biotech startups to accelerate innovation, and forming strategic alliances for global distribution. Many firms focus on expanding their product portfolios to cover rare and chronic diseases while enhancing manufacturing capabilities for high-purity peptides. Market participants are increasingly leveraging digital platforms and AI for precision drug development, patient monitoring, and real-world data collection.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumption and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Application trends

- 2.2.4 Route of administration trends

- 2.2.5 Manufacturer type trends

- 2.2.6 Synthesis technology trends

- 2.2.7 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of cancer

- 3.2.1.2 Rising incidences of metabolic & endocrine disorders

- 3.2.1.3 Increasing investments in research and development of novel drugs

- 3.2.1.4 Technological advancement in peptide therapeutics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory requirements for drug approval

- 3.2.2.2 High cost for drug development

- 3.2.3 Market opportunities

- 3.2.3.1 Innovation in peptide-drug conjugates and radiolabelled peptides

- 3.2.3.2 Expansion of oral and long-acting peptide formulations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Future market trends

- 3.6 Technological landscape

- 3.6.1 Current technologies

- 3.6.2 Emerging technologies

- 3.7 Patent analysis

- 3.8 Pipeline analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Branded peptides

- 5.3 Generic peptides

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Metabolic & endocrine disorders

- 6.3 Cancer

- 6.4 Cardiovascular disorders

- 6.5 Gastrointestinal disorders

- 6.6 Central nervous system disorders

- 6.7 Respiratory disorders

- 6.8 Pain management

- 6.9 Other applications

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Parenteral

- 7.3 Oral

- 7.4 Other route of administration

Chapter 8 Market Estimates and Forecast, By Manufacturer Type, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 In-house

- 8.3 Outsourced

Chapter 9 Market Estimates and Forecast, By Synthesis Technology, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Liquid phase peptide synthesis (LPPS)

- 9.3 Solid phase peptide synthesis (SPPS)

- 9.4 Hybrid technology

Chapter 10 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Hospitals and clinics

- 10.3 Pharmaceutical and biotechnology companies

- 10.4 Other end use

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Amgen

- 12.2 Ascendis Pharma

- 12.3 AstraZeneca

- 12.4 Bristol-Myers Squibb

- 12.5 Eli Lilly and Company

- 12.6 Ferring Pharmaceuticals

- 12.7 Merck & Co.

- 12.8 Novo Nordisk

- 12.9 PeptiDream

- 12.10 PolyPeptide Group

- 12.11 Repligen Corporation

- 12.12 Rhythm Pharmaceuticals

- 12.13 Sanofi

- 12.14 X-GEN Pharmaceuticals

- 12.15 Zydus Lifesciences

肽類藥物市場:按產品類型、合成技術、給藥途徑、應用和最終用戶分類-2026-2032年全球市場預測動物抗菌胜肽市場:按產品類型、應用和最終用戶分類-2026-2032年全球市場預測

肽類藥物市場:按產品類型、合成技術、給藥途徑、應用和最終用戶分類-2026-2032年全球市場預測動物抗菌胜肽市場:按產品類型、應用和最終用戶分類-2026-2032年全球市場預測 肽類治療市場:依產品類型、應用、給藥途徑及地區分類

肽類治療市場:依產品類型、應用、給藥途徑及地區分類 肽類治療藥物市場規模、佔有率、趨勢和預測:按類型、製造商、合成技術、給藥途徑、應用和地區分類,2026-2034年

肽類治療藥物市場規模、佔有率、趨勢和預測:按類型、製造商、合成技術、給藥途徑、應用和地區分類,2026-2034年 全球胜肽類治療藥物市場:市場規模、佔有率和趨勢分析(按類型、應用、製造商、給藥途徑、合成技術和地區分類),細分市場預測(2026-2033 年)

全球胜肽類治療藥物市場:市場規模、佔有率和趨勢分析(按類型、應用、製造商、給藥途徑、合成技術和地區分類),細分市場預測(2026-2033 年) 肽類藥物市場-全球產業規模、佔有率、趨勢、機會及預測(按應用、類型、製造商、給藥途徑、合成技術、地區和競爭格局分類,2021-2031年)日本胜肽類藥物市場報告(按類型、製造商類型、合成技術、給藥途徑、應用和地區分類,2026-2034年)

肽類藥物市場-全球產業規模、佔有率、趨勢、機會及預測(按應用、類型、製造商、給藥途徑、合成技術、地區和競爭格局分類,2021-2031年)日本胜肽類藥物市場報告(按類型、製造商類型、合成技術、給藥途徑、應用和地區分類,2026-2034年) 肽類藥物市場:產業趨勢及全球預測(至2040年)-依給藥途徑、治療領域及地區劃分

肽類藥物市場:產業趨勢及全球預測(至2040年)-依給藥途徑、治療領域及地區劃分 全球蛋白質和胜肽類藥物治療市場成長機會:2030 年預測雙環毒素偶聯物的全球市場 - 臨床試驗,獨自平台,市場機會(2025年)

全球蛋白質和胜肽類藥物治療市場成長機會:2030 年預測雙環毒素偶聯物的全球市場 - 臨床試驗,獨自平台,市場機會(2025年)