|

市場調查報告書

商品編碼

1876807

醫療無人機配送服務市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Medical Drone Delivery Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

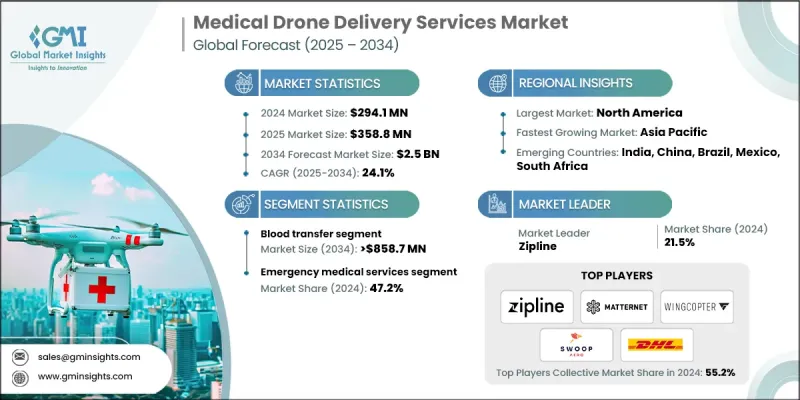

2024 年全球醫療無人機配送服務市場價值為 2.941 億美元,預計到 2034 年將以 24.1% 的複合年成長率成長至 25 億美元。

市場成長的驅動力包括:對快速醫療物資配送日益成長的需求、有利的政府監管政策、技術進步以及無人機在醫療物流領域應用的不斷廣泛。醫療無人機配送服務為醫院、血庫、製藥公司和醫療服務供應商提供創新解決方案,大幅提升配送速度、營運效率和病患療效。這些解決方案包括自主無人機、混合動力垂直起降飛機以及能夠運輸血液、疫苗、實驗室樣本和藥品的整合式配送平台。透過大幅縮短配送時間,這些服務有助於醫療服務提供者提升病患照護水準。此外,完善的監管框架和政府試點計畫也透過簡化空域管理和為商業醫療無人機營運提供資金支持,推動了該領域的成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 2.941億美元 |

| 預測值 | 25億美元 |

| 複合年成長率 | 24.1% |

無人機設計的技術進步,包括自主導航、混合動力垂直起降能力、更大的有效載荷能力以及冷鏈整合,使得敏感醫療用品能夠安全高效地運輸。醫療無人機配送服務依靠無人機快速運送血液、疫苗、實驗室樣本和藥品,為醫院、急救服務機構和醫療保健提供者提供支持,同時改善患者治療效果和營運物流。

由於緊急情況和偏遠地區對快速送血的迫切需求,預計到2024年,血液運輸領域將佔據35.9%的市場佔有率。醫院、血庫和急診中心之間快速可靠的血液運輸對於手術、創傷救治和緊急輸血至關重要,因為任何延誤都可能危及生命。血液運輸與急救醫療服務領域合計佔總市場價值的81.4%以上。與傳統公路運輸相比,無人機顯著縮短了響應時間,而人工智慧路線最佳化、自主導航和即時監控等功能則確保了即使在擁擠的城市地區或偏遠地區也能安全精準地完成配送。

2024年,北美醫療無人機配送服務市佔率將達到33.2%,這得益於該地區在技術、經濟和監管方面的優勢。該地區擁有先進的無人機創新技術,例如自主導航、混合動力垂直起降飛機、人工智慧驅動的路線規劃以及物聯網賦能的有效載荷監控,從而確保血液、疫苗、實驗室樣本和藥品的快速安全配送。

全球醫療無人機配送服務市場的主要參與者包括Matternet、Volansi、Wingcopter、DHL、Apian、Air Taurus、MightyFly、Wing(Alphabet旗下公司)、Flirtey/SkyDrop、Draganfly和Zipline。這些公司正透過多種策略鞏固其市場地位。他們投資先進的無人機技術,包括人工智慧導航、混合動力垂直起降和有效載荷監控系統,以提高效率和可靠性。與醫院、血庫和製藥公司建立策略夥伴關係有助於擴大服務覆蓋範圍並建立信任。此外,各公司也積極參與政府試點項目,以獲得監管支持並儘早獲得市場認可。併購則用於整合技術和擴大營運規模。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 產業影響因素

- 成長促進因素

- 醫療無人機在醫療保健產業的應用日益廣泛

- 政府措施數量不斷增加

- 技術進步

- 公眾接受度不斷提高

- 產業陷阱與挑戰

- 醫療無人機相關併發症

- 市場機遇

- 擴大偏遠和農村地區的醫療保健服務

- 與智慧醫療基礎設施的整合

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 技術格局

- 當前技術趨勢

- 自主無人機導航系統可實現醫療物資的精準配送

- 適用於靈活城市和鄉村作業的混合垂直起降無人機

- 利用物聯網進行追蹤與監控,實現即時配送更新

- 新興技術

- 將區塊鏈技術應用於安全、透明、可追溯的醫療用品物流。

- 利用無人機集群技術同時向多個地點進行配送。

- 用於障礙物偵測和自動避障的先進感測器

- 當前技術趨勢

- 差距分析

- 波特的分析

- PESTEL 分析

- 未來市場趨勢

- 無人機網路擴展與智慧醫院和醫療保健基礎設施相結合

- 緊急醫療服務和遠距醫療服務採用率不斷提高

- 監管協調和空域管理,以支援大規模營運

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 競爭定位矩陣

- 主要市場參與者的競爭分析

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新服務類型推出

- 擴張計劃

第5章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 血液轉移

- 藥物/藥品轉移

- 疫苗接種計劃

- 實驗室樣品

- 其他應用

第6章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 緊急醫療服務

- 血庫

- 其他最終用途

第7章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第8章:公司簡介

- Air Taurus

- Apian

- DHL

- Draganfly

- Flirtey /SkyDrop

- Matternet

- MightyFly

- Swoop Aero

- Volansi

- Wing (Alphabet)

- Wingcopter

- Zipline

The Global Medical Drone Delivery Services Market was valued at USD 294.1 million in 2024 and is estimated to grow at a CAGR of 24.1% to reach USD 2.5 billion by 2034.

The market is driven by the growing need for rapid medical deliveries, favorable government regulations, technological advancements, and increasing adoption of drones in healthcare logistics. Medical drone delivery services offer innovative solutions to hospitals, blood banks, pharmaceutical companies, and healthcare providers, improving delivery speed, operational efficiency, and patient outcomes. These solutions include autonomous drones, hybrid VTOL aircraft, and integrated delivery platforms capable of transporting blood, vaccines, laboratory samples, and medications. By drastically reducing delivery times, these services help healthcare providers enhance patient care. Supportive regulatory frameworks and government pilot programs are also fueling growth by streamlining airspace management and providing funding for commercial medical drone operations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $294.1 Million |

| Forecast Value | $2.5 Billion |

| CAGR | 24.1% |

Technological progress in drone design, including autonomous navigation, hybrid VTOL capabilities, expanded payload capacity, and cold-chain integration, allows sensitive medical supplies to be transported safely and efficiently. Medical drone delivery services rely on unmanned aerial vehicles to move blood, vaccines, lab specimens, and pharmaceuticals quickly, supporting hospitals, emergency services, and healthcare providers while improving patient outcomes and operational logistics.

The blood transfer segment held a 35.9% share in 2024, owing to the critical demand for rapid blood delivery in emergencies and remote regions. Quick, reliable blood transport between hospitals, blood banks, and emergency medical centers is essential for surgeries, trauma care, and urgent transfusions, where delays can be life-threatening. Combined with the emergency medical services segment, the two largest categories accounted for over 81.4% of the total market value. Drones significantly reduce response times compared to traditional road transport, while features like AI-based route optimization, autonomous navigation, and real-time monitoring ensure secure and precise deliveries, even in crowded urban areas or remote locations.

North America Medical Drone Delivery Services Market held a 33.2% share in 2024, benefiting from technological, economic, and regulatory advantages. The region features advanced drone innovations such as autonomous navigation, hybrid VTOL aircraft, AI-powered route planning, and IoT-enabled payload monitoring, ensuring the rapid and safe delivery of blood, vaccines, laboratory specimens, and medications.

Key players operating in the Global Medical Drone Delivery Services Market include Matternet, Volansi, Wingcopter, DHL, Apian, Air Taurus, MightyFly, Wing (Alphabet), Flirtey/SkyDrop, Draganfly, and Zipline. Companies in the Medical Drone Delivery Services Market are strengthening their presence through several strategies. They are investing in advanced drone technologies, including AI navigation, hybrid VTOL, and payload monitoring systems, to enhance efficiency and reliability. Strategic partnerships with hospitals, blood banks, and pharmaceutical firms help expand service coverage and build trust. Firms are also participating in government pilot programs to secure regulatory support and gain early market adoption. Mergers and acquisitions are used to integrate technologies and scale operations.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Application trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing application of medical drone in the healthcare industry

- 3.2.1.2 Rising number of government initiatives

- 3.2.1.3 Technological advancements

- 3.2.1.4 Growing public acceptance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complications associated with medical drone

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in remote and rural healthcare access

- 3.2.3.2 Integration with smart healthcare infrastructure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 LAMEA

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.1.1 Autonomous drone navigation systems enabling precise delivery of medical supplies

- 3.5.1.2 Hybrid VTOL (vertical take-off and landing) drones for flexible urban and rural operations

- 3.5.1.3 IoT-enabled tracking and monitoring for real-time delivery updates

- 3.5.2 Emerging technologies

- 3.5.2.1 Integration of blockchain for secure, transparent, and traceable medical supply logistics.

- 3.5.2.2 Swarm drone technology for simultaneous deliveries to multiple locations.

- 3.5.2.3 Advanced sensors for obstacle detection and automated collision avoidance

- 3.5.1 Current technological trends

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.9.1 Expansion of drone networks integrated with smart hospitals and healthcare infrastructure

- 3.9.2 Increased adoption in emergency medical services and remote healthcare delivery

- 3.9.3 Regulatory harmonization and airspace management to support large-scale operations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New service type launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Blood transfer

- 5.3 Drugs/pharmaceutical transfer

- 5.4 Vaccination program

- 5.5 Lab sample

- 5.6 Other applications

Chapter 6 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Emergency medical services

- 6.3 Blood banks

- 6.4 Other end use

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Air Taurus

- 8.2 Apian

- 8.3 DHL

- 8.4 Draganfly

- 8.5 Flirtey /SkyDrop

- 8.6 Matternet

- 8.7 MightyFly

- 8.8 Swoop Aero

- 8.9 Volansi

- 8.10 Wing (Alphabet)

- 8.11 Wingcopter

- 8.12 Zipline