|

市場調查報告書

商品編碼

1876796

傷口護理治療設備市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Wound Care Therapy Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

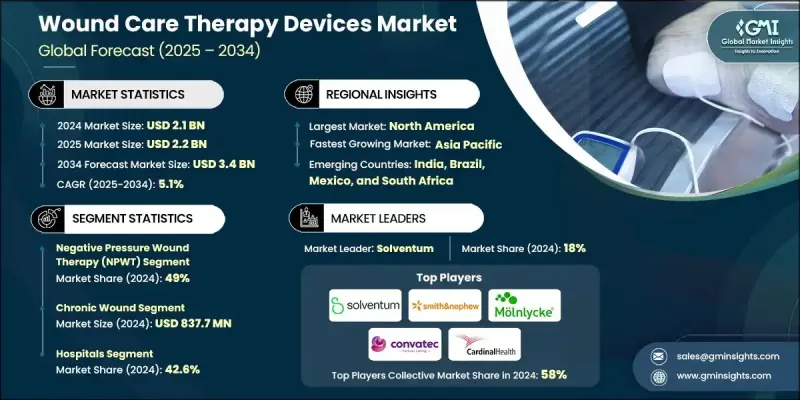

2024 年全球傷口護理治療設備市場價值為 21 億美元,預計到 2034 年將以 5.1% 的複合年成長率成長至 34 億美元。

慢性傷口,尤其是老年人群中慢性傷口的日益普遍,是推動市場擴張的主要因素。傷口護理治療設備是先進的醫療系統,旨在促進和加速急性和慢性傷口的癒合。與傳統傷口敷料不同,這些技術透過負壓、氧氣輸送或電刺激等方式主動調節傷口環境。這些機制有助於增強組織再生,最大限度地降低感染風險,並促進更快康復。持續的技術進步使得智慧傷口治療系統得以開發,能夠即時追蹤傷口溫度、濕度和感染指標等參數。這些創新使臨床醫生能夠及時、精準地做出治療決策,從而改善癒合效果並減少併發症。攜帶式傷口護理系統,包括小型負壓傷口治療(NPWT)設備,在家庭護理和門診環境中越來越受歡迎,從而減少了對醫院的依賴和醫療保健支出。糖尿病患者數量的增加,以及他們患有糖尿病足潰瘍等慢性傷口的風險增加,進一步推動了市場的持續成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 21億美元 |

| 預測值 | 34億美元 |

| 複合年成長率 | 5.1% |

負壓傷口治療(NPWT)在2024年佔了49%的市場。此療法透過將傷口邊緣拉攏、刺激組織肉芽形成並促進傷口部位血液循環來增強傷口癒合。 NPWT能夠有效清除液體、滲出液和細菌,從而最大限度地降低感染風險並加速癒合,使其在治療創傷或手術造成的複雜傷口方面尤為有效。

2024年,醫院市佔率比42.6%,預計到2034年將達到15億美元。醫院仍然是傷口護理管理的主要中心,為外科傷口、急性傷口和慢性傷口提供全面的治療。醫院能夠獲得包括負壓傷口治療系統、電刺激裝置和氧氣治療方案在內的各種先進治療設備,這鞏固了其作為市場領先終端用戶的地位。

2024年,美國傷口護理治療設備市場規模達6.974億美元。美國糖尿病發生率的不斷攀升顯著推動了市場成長,因為糖尿病患者容易患有慢性潰瘍,需要先進的傷口治療系統。人們對現代化、高效傷口管理技術的日益青睞,也持續鞏固了美國在全球市場的領先地位。

全球傷口照護治療設備市場的主要參與者包括Accel-Heal Technologies、Cardinal Health、ConvaTec、DeRoyal Industries、Medaxis、Molnlycke Health Care、Sky Medical Technology、Smith+Nephew、Solventum、Talley Group和WoundEL Health Care。這些領導企業正優先考慮創新、合作和產品多元化,以鞏固其市場地位。持續的研發投入使他們能夠推出更強大、更便攜、更舒適的先進傷口癒合解決方案。許多公司正在擴展其產品組合,推出整合感測器和數位連接功能的智慧傷口管理系統,用於遠端監測和資料分析。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 每個階段的價值增加

- 影響價值鏈的因素

- 產業影響因素

- 成長促進因素

- 慢性傷口發生率上升

- 外科手術數量不斷增加

- 政府加強進行傷口護理治療相關舉措

- 傷口護理治療設備的技術進步

- 產業陷阱與挑戰

- 先進設備成本高昂

- 缺乏熟練的醫療保健專業人員

- 市場機遇

- 智慧科技的融合

- 家庭醫療保健和遠端監測

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 亞太地區

- 歐洲

- 拉丁美洲

- 中東和非洲

- 技術格局

- 當前技術趨勢

- 新興技術

- 未來市場趨勢

- 2024年定價分析

- 專利分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 亞太地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀錶板

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依產品分類,2021-2034年

- 主要趨勢

- 負壓傷口治療

- 氧氣和高壓氧設備

- 電刺激裝置

- 壓力釋放裝置

- 其他產品

第6章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 慢性傷口

- 糖尿病足潰瘍

- 壓瘡

- 靜脈性腿部潰瘍

- 其他慢性傷口

- 急性傷口

- 手術傷口

- 創傷性傷口

- 燒傷

第7章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 醫院

- 專科診所

- 家庭護理機構

- 其他最終用途

第8章:市場估算與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Accel-Heal Technologies

- Cardinal Health

- ConvaTec

- DeRoyal Industries

- Medaxis

- Molnlycke Health Care

- Sky Medical Technology

- Smith+Nephew

- Solventum

- Talley Group

- WoundEL Health Care

The Global Wound Care Therapy Devices Market was valued at USD 2.1 billion in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 3.4 billion by 2034.

The growing prevalence of chronic wounds, particularly among elderly populations, is a major driver of market expansion. Wound care therapy devices are advanced medical systems developed to facilitate and accelerate healing in both acute and chronic wounds. Unlike conventional wound dressings, these technologies actively regulate the wound environment through methods such as negative pressure, oxygen delivery, or electrical stimulation. Such mechanisms help enhance tissue regeneration, minimize the risk of infection, and support faster recovery. Ongoing technological progress has enabled the development of smart wound therapy systems capable of tracking wound parameters like temperature, moisture, and infection indicators in real time. These innovations enable clinicians to make timely and precise treatment decisions, improving healing outcomes and reducing complications. Portable wound care systems, including compact negative pressure wound therapy (NPWT) devices, are becoming increasingly popular for use in homecare and outpatient settings, reducing hospital dependency and healthcare expenses. The rising number of diabetic patients who are at higher risk of developing chronic wounds such as diabetic foot ulcers further contributes to the market's continued growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.1 Billion |

| Forecast Value | $3.4 Billion |

| CAGR | 5.1% |

The negative pressure wound therapy (NPWT) accounted for a 49% share in 2024. This therapy enhances wound closure by drawing wound edges together, stimulating tissue granulation, and promoting improved blood circulation at the site. By efficiently removing fluids, exudates, and bacteria, NPWT minimizes the chances of infection and accelerates healing, making it particularly valuable in managing complex wounds caused by trauma or surgery.

The hospitals segment held 42.6% share in 2024 and is expected to reach USD 1.5 billion by 2034. Hospitals continue to be the primary centers for wound care management, offering comprehensive treatment for surgical, acute, and chronic wounds. Their access to a wide range of advanced therapy devices including NPWT systems, electrical stimulation units, and oxygen-based treatment solutions consolidates their position as the leading end users within the market.

U.S. Wound Care Therapy Devices Market reached USD 697.4 million in 2024. The increasing rate of diabetes in the U.S. has substantially influenced market growth, as diabetic patients are prone to chronic ulcers that require advanced wound therapy systems. The growing preference for modern, efficient wound management technologies continues to strengthen the country's leadership in the global market.

Prominent players operating in the Global Wound Care Therapy Devices Market include Accel-Heal Technologies, Cardinal Health, ConvaTec, DeRoyal Industries, Medaxis, Molnlycke Health Care, Sky Medical Technology, Smith+Nephew, Solventum, Talley Group, and WoundEL Health Care. Leading companies in the Global Wound Care Therapy Devices Market are prioritizing innovation, partnerships, and product diversification to strengthen their market presence. Continuous investment in research and development enables them to introduce advanced wound healing solutions with enhanced functionality, portability, and patient comfort. Many firms are expanding their portfolios with smart wound management systems that incorporate sensors and digital connectivity for remote monitoring and data analysis.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 End Use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of chronic wounds

- 3.2.1.2 Increasing number of surgical procedures

- 3.2.1.3 Surge in government initiatives regarding wound care treatment

- 3.2.1.4 Technological advancements in wound care therapy devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced devices

- 3.2.2.2 Lack of skilled healthcare professionals

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of smart technologies

- 3.2.3.2 Home healthcare and remote monitoring

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Asia Pacific

- 3.4.3 Europe

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Pricing analysis, 2024

- 3.8 Patent analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.7 Key developments

- 4.7.1 Mergers and acquisitions

- 4.7.2 Partnerships and collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Negative pressure wound therapy

- 5.3 Oxygen and hyperbaric oxygen equipment

- 5.4 Electric stimulation devices

- 5.5 Pressure relief devices

- 5.6 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Chronic wounds

- 6.2.1 Diabetic foot ulcers

- 6.2.2 Pressure ulcers

- 6.2.3 Venous legs ulcers

- 6.2.4 Other chronic wounds

- 6.3 Acute wounds

- 6.3.1 Surgical wounds

- 6.3.2 Traumatic wounds

- 6.3.3 Burns

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Specialty clinics

- 7.4 Home care settings

- 7.5 Other End Use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Accel-Heal Technologies

- 9.2 Cardinal Health

- 9.3 ConvaTec

- 9.4 DeRoyal Industries

- 9.5 Medaxis

- 9.6 Molnlycke Health Care

- 9.7 Sky Medical Technology

- 9.8 Smith+Nephew

- 9.9 Solventum

- 9.10 Talley Group

- 9.11 WoundEL Health Care

2026年全球傷口護理設備市場報告2026年全球兒童動畫創可貼市場報告2026年全球術前感染預防與傷口清潔設備市場報告

2026年全球傷口護理設備市場報告2026年全球兒童動畫創可貼市場報告2026年全球術前感染預防與傷口清潔設備市場報告 瘢痕疙瘩治療市場分析及預測(至2035年):依類型、產品類型、服務、技術、應用、最終用戶、製程、設備、解決方案、模式

瘢痕疙瘩治療市場分析及預測(至2035年):依類型、產品類型、服務、技術、應用、最終用戶、製程、設備、解決方案、模式 全球急性創傷護理市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球抗菌傷口敷料市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球急性創傷護理市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球抗菌傷口敷料市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 日本創傷護理市場規模、佔有率、趨勢和預測:按產品類型、傷口類型、最終用戶和地區分類,2026-2034年

日本創傷護理市場規模、佔有率、趨勢和預測:按產品類型、傷口類型、最終用戶和地區分類,2026-2034年 全球創傷護理市場按產品類型、分銷管道、應用、最終用戶、國家和地區分類-產業分析、市場規模、佔有率和預測(2025-2032年)

全球創傷護理市場按產品類型、分銷管道、應用、最終用戶、國家和地區分類-產業分析、市場規模、佔有率和預測(2025-2032年) 傷口護理器材市場-全球產業規模、佔有率、趨勢、機會、預測:按傷口類型、產品、最終用戶、地區和競爭對手分類,2021-2031年抗菌創傷護理敷料市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、應用、最終用戶、地區和競爭對手分類,2021-2031年

傷口護理器材市場-全球產業規模、佔有率、趨勢、機會、預測:按傷口類型、產品、最終用戶、地區和競爭對手分類,2021-2031年抗菌創傷護理敷料市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、應用、最終用戶、地區和競爭對手分類,2021-2031年