|

市場調查報告書

商品編碼

1876639

公用事業通訊市場機會、成長促進因素、產業趨勢分析及預測(2025-2034 年)Utility Communication Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

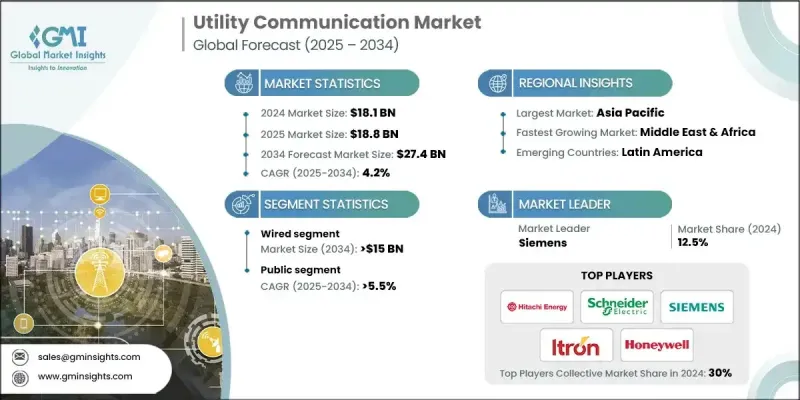

2024 年全球公用事業通訊市場價值為 181 億美元,預計到 2034 年將以 4.2% 的複合年成長率成長至 274 億美元。

推動這一市場擴張的,是政府主導的各項舉措,這些舉措旨在推廣先進的通訊技術,例如專用LTE/5G網路、光纖、射頻網狀網路以及基於物聯網的遙測系統。這些技術在建構更智慧、更互聯的公用事業網路中發揮著至關重要的作用,從而支援再生能源併網和電網現代化。隨著全球電氣化和清潔能源專案在永續發展議程的推動下加速推進,公用事業通訊系統對於高效的電力分配和監控變得不可或缺。歐盟的數位化路線圖和美國聯邦政府的資助計畫等政策,正引導大量投資湧入現代電網通訊基礎設施。這包括自動計量、電網自動化和專用網路部署等舉措,這些舉措能夠增強安全性、可擴展性和即時運行可視性。向分散式電力系統轉型以及分散式能源的整合,正在公用事業生態系統中催生新的通訊需求。隨著智慧電網的演進,公用事業公司越來越依賴無縫的資料連接來協調發電、儲能和用電環節的運行,從而確保全球電網的可靠性和效率。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 181億美元 |

| 預測值 | 274億美元 |

| 複合年成長率 | 4.2% |

預計到2034年,有線通訊市場規模將達到150億美元,主要歸功於這些系統帶來的許多營運優勢。包括光纖、乙太網路和電力線通訊在內的有線技術構成了關鍵電網基礎設施的骨幹。它們提供卓越的頻寬、低延遲和高抗干擾能力,使其成為變電站自動化、SCADA系統和廣域電網管理等應用中即時控制的關鍵要素。其強大的性能和可靠性是推動公用事業營運中對其需求持續成長的關鍵因素。

預計到2034年,公共事業板塊的複合年成長率將達到5.5%。由於公共事業部門負責大規模的電力傳輸和分配網路,因此在通訊領域中扮演著至關重要的角色。為了維持效率和可靠性,這些機構高度依賴先進的通訊系統,以實現有效的電網監控、自動化和維護。智慧電網技術的持續推廣,包括智慧變電站和高階計量基礎設施,凸顯了能夠大規模處理複雜互聯電力系統的通訊平台的重要性日益成長。

2024年,美國公用事業通訊市場規模預計達37億美元。美國透過大規模採用智慧電網解決方案,並在先進的政策和資金機制的支持下,繼續在塑造市場方向方面發揮領導作用。全美各地的公用事業公司都在大力投資有線和無線通訊網路,以提高電網可靠性、支援需量反應計劃並管理分散式能源。美國的監管框架鼓勵創新,同時強調網路安全和營運效率。

全球公用事業通訊市場的主要企業包括Itron, Inc.、思科系統、施耐德電氣、西門子、摩托羅拉解決方案、Doxim、日立能源、霍尼韋爾、Ribbon Communications、Utility Communications Inc.、Hexagon、Kontron、Zenner International、Hexaware Technologies和Morcom International。這些企業正採取多種策略來鞏固其競爭地位。許多企業專注於產品創新,並整合物聯網、人工智慧驅動的分析和專用5G網路等下一代技術,以提高公用事業的營運效率和連接性。它們也積極尋求與公用事業供應商和政府進行策略合作,以實施智慧電網專案和大規模通訊升級。此外,各公司透過併購和研發投資來拓展業務範圍,從而增強其全球影響力和技術實力。同時,它們也致力於開發網路安全增強型解決方案,以保護關鍵基礎設施。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 監管環境

- 產業影響因素

- 成長促進因素

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL 分析

- 新興機會與趨勢

- 數位化與物聯網整合

- 新興市場滲透

- 投資分析及未來展望

第4章:競爭格局

- 介紹

- 按地區分類的公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 策略舉措

- 競爭基準描述

- 策略儀錶板

- 創新與技術格局

第5章:市場規模及預測:依技術分類,2021-2034年

- 主要趨勢

- 有線

- 無線的

第6章:市場規模及預測:依公用事業分類,2021-2034年

- 主要趨勢

- 民眾

- 私人的

第7章:市場規模及預測:依組件分類,2021-2034年

- 主要趨勢

- 硬體

- 軟體

第8章:市場規模及預測:依應用領域分類,2021-2034年

- 主要趨勢

- 民眾

- 私人輸配電

- 石油和天然氣公用事業

- 其他

第9章:市場規模及預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 法國

- 德國

- 義大利

- 俄羅斯

- 西班牙

- 亞太地區

- 中國

- 澳洲

- 印度

- 日本

- 韓國

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 南非

- 埃及

- 拉丁美洲

- 巴西

- 阿根廷

第10章:公司簡介

- Cisco System

- Doxim

- Hexagon

- Hexaware Technologies

- Hitachi Energy

- Honeywell

- Itron, Inc.

- Kontron

- Morcom International

- Motorola Solutions

- Ribbon Communications

- Schneider Electric

- Siemens

- Utility Communications Inc.

- Zenner International

The Global Utility Communication Market was valued at USD 18.1 billion in 2024 and is estimated to grow at a CAGR of 4.2% to reach USD 27.4 billion by 2034.

The expansion of this market is driven by government-led initiatives promoting advanced communication technologies such as private LTE/5G networks, fiber optics, RF mesh, and IoT-based telemetry systems. These technologies play a critical role in enabling smarter, more connected utility networks that support renewable integration and grid modernization. As global electrification and clean energy projects accelerate under sustainability agendas across regions, utility communication systems are becoming indispensable for efficient power distribution and monitoring. Policies like the EU's digitalization roadmap and U.S. federal funding programs are channeling significant investments into modern grid communication infrastructure. This includes initiatives such as automated metering, grid automation, and private network deployments that enhance security, scalability, and real-time operational visibility. The ongoing transition toward decentralized power systems, coupled with the integration of distributed energy resources, is creating new communication demands within the utility ecosystem. As smart grids evolve, utilities are increasingly relying on seamless data connectivity to coordinate operations across generation, storage, and consumption points, ensuring grid reliability and efficiency on a global scale.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $18.1 Billion |

| Forecast Value | $27.4 Billion |

| CAGR | 4.2% |

The wired communication segment is expected to reach USD 15 billion by 2034, attributed to the multiple operational benefits these systems offer. Wired technologies, including fiber optics, Ethernet, and power line communication, form the backbone of critical grid infrastructure. They provide superior bandwidth, low latency, and high resistance to interference, making them essential for real-time control in applications such as substation automation, SCADA systems, and wide-area grid management. Their robust performance and reliability are key factors driving their sustained demand in utility operations.

The public utility segment is forecasted to grow at a CAGR of 5.5% through 2034. Public utilities hold a pivotal role in the communication landscape due to their responsibility for large-scale power transmission and distribution networks. To maintain efficiency and reliability, these entities rely heavily on advanced communication systems that enable effective grid supervision, automation, and maintenance. The continuous rollout of smart grid technologies, including intelligent substations and advanced metering infrastructure, underscores the growing importance of communication platforms that can handle complex, interconnected power systems at scale.

U.S. Utility Communication Market was valued at USD 3.7 billion in 2024. The United States continues to play a leading role in shaping the market's direction through large-scale adoption of smart grid solutions supported by progressive policies and funding mechanisms. Utilities across the country are investing heavily in both wired and wireless communication networks to enhance grid reliability, support demand response initiatives, and manage distributed energy resources. The U.S. regulatory framework encourages innovation while emphasizing cybersecurity and operational efficiency.

Prominent companies operating in the Global Utility Communication Market include Itron, Inc., Cisco Systems, Schneider Electric, Siemens, Motorola Solutions, Doxim, Hitachi Energy, Honeywell, Ribbon Communications, Utility Communications Inc., Hexagon, Kontron, Zenner International, Hexaware Technologies, and Morcom International. Companies in the Utility Communication Market are employing multiple strategies to solidify their competitive position. Many are focusing on product innovation and integrating next-generation technologies such as IoT, AI-driven analytics, and private 5G networks to improve operational efficiency and connectivity for utilities. Strategic collaborations with utility providers and governments are being pursued to implement smart grid projects and large-scale communication upgrades. Firms are expanding their portfolios through mergers, acquisitions, and R&D investments to strengthen their global presence and technological capabilities. Additionally, emphasis is being placed on developing cybersecurity-enhanced solutions to protect critical infrastructure.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Emerging opportunities & trends

- 3.7.1 Digitalization & IoT integration

- 3.7.2 Emerging market penetration

- 3.8 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by Region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking depictions

- 4.5 Strategy dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Technology, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Wired

- 5.3 Wireless

Chapter 6 Market Size and Forecast, By Utility, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Public

- 6.3 Private

Chapter 7 Market Size and Forecast, By Component, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Hardware

- 7.3 Software

Chapter 8 Market Size and Forecast, By Application, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 Public

- 8.3 Private transmission & distribution

- 8.4 Oil & gas utilities

- 8.5 Others

Chapter 9 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 France

- 9.3.3 Germany

- 9.3.4 Italy

- 9.3.5 Russia

- 9.3.6 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Australia

- 9.4.3 India

- 9.4.4 Japan

- 9.4.5 South Korea

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 Turkey

- 9.5.4 South Africa

- 9.5.5 Egypt

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Argentina

Chapter 10 Company Profiles

- 10.1 Cisco System

- 10.2 Doxim

- 10.3 Hexagon

- 10.4 Hexaware Technologies

- 10.5 Hitachi Energy

- 10.6 Honeywell

- 10.7 Itron, Inc.

- 10.8 Kontron

- 10.9 Morcom International

- 10.10 Motorola Solutions

- 10.11 Ribbon Communications

- 10.12 Schneider Electric

- 10.13 Siemens

- 10.14 Utility Communications Inc.

- 10.15 Zenner International

公用事業通訊市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類

公用事業通訊市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類 公用事業通訊市場 - 全球產業規模、佔有率、趨勢、機會和預測(按技術、公用事業、組件、應用、最終用途、地區和競爭格局分類),2021-2031年

公用事業通訊市場 - 全球產業規模、佔有率、趨勢、機會和預測(按技術、公用事業、組件、應用、最終用途、地區和競爭格局分類),2021-2031年 公用事業通訊市場(按通訊技術、公用事業類型、應用、部署類型和最終用戶分類)—2025-2032 年全球預測

公用事業通訊市場(按通訊技術、公用事業類型、應用、部署類型和最終用戶分類)—2025-2032 年全球預測 全球工業公用事業通訊市場

全球工業公用事業通訊市場 公用事業通訊市場規模、佔有率和趨勢分析報告:按技術、組件、實用程序、應用、最終用途、地區和細分市場預測,2025 年至 2033 年

公用事業通訊市場規模、佔有率和趨勢分析報告:按技術、組件、實用程序、應用、最終用途、地區和細分市場預測,2025 年至 2033 年 全球公用事業通訊市場規模研究(按技術、公用事業、組件、應用、最終用途和 2022-2032 年區域預測)

全球公用事業通訊市場規模研究(按技術、公用事業、組件、應用、最終用途和 2022-2032 年區域預測)