|

市場調查報告書

商品編碼

1876617

富勒烯基特種化學品市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Fullerene-Based Specialty Chemicals Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

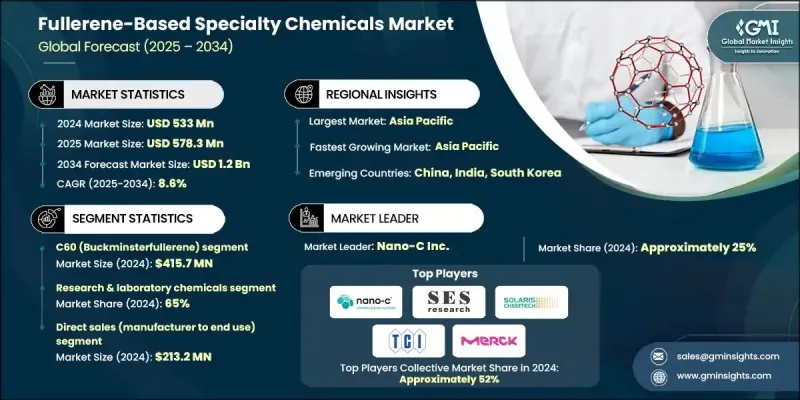

2024 年全球富勒烯基特種化學品市場價值為 5.33 億美元,預計到 2034 年將以 8.6% 的複合年成長率成長至 12 億美元。

成長動能主要得益於有機光伏(OPV)及相關電子應用領域不斷擴大的機遇,而富勒烯功能化和合成技術的顯著進步也為此提供了有力支撐。 C60和C70富勒烯溶解性、穩定性和電子受體性能的提升,正加速其在有機電子和能源系統中的應用。奈米技術研究經費的充足投入,以及監管架構和政策激勵措施的日益完善,持續拓展富勒烯基材料在能源、電子和製藥研發領域的應用範圍。隨著對高性能奈米材料需求的不斷成長,富勒烯及其衍生物在下一代裝置、軟性電子元件和先進化學配方等領域的巨大潛力日益受到認可。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 5.33億美元 |

| 預測值 | 12億美元 |

| 複合年成長率 | 8.6% |

2024年,電子和有機光伏(OPV)領域創造了1.173億美元的收入,佔市場佔有率的22%。該領域持續蓬勃發展,得益於有機電子技術的進步以及溶液加工型富勒烯衍生物的日益普及,這些進步確保了裝置可擴展性和性能的提升。這些先進材料在軟性節能技術中的應用,正在推動多個產業對這些材料的需求。

2024 年,直銷通路價值 2.132 億美元,佔 40% 的市場佔有率,預計到 2034 年將以 8.6% 的複合年成長率成長。由於富勒烯產品的高度專業化特性,該通路仍佔據主導地位。富勒烯產品通常需要客製化規格、嚴格的品質控制,以及製造商與最終用戶(如研究機構、電子公司和製藥公司)之間的密切合作。

2024年,亞太地區富勒烯基特種化學品市場規模達2.559億美元,市佔率48%。預計該地區在2025年至2034年間將以10.2%的複合年成長率成長。強勁的成長得益於該地區強大的電子製造能力、完善的化學品供應體係以及政府積極推動奈米材料和下一代光伏技術研究的舉措。中國、日本、韓國和印度在生產和創新方面仍處於領先地位,這得益於其充滿活力的新創企業生態系統和先進的研發項目。

全球富勒烯基特種化學品市場的主要參與者包括Nano-C Inc.、SES Research Inc.、Solaris Chem、TCI(東京化成工業株式會社)、Sigma-Aldrich / Merck KGaA、American Elements、Strem Chemicals、Ossila、Alfa Aesar(賽默飛世爾科技)、Aberial Carbon Corporation。這些公司積極投資研發,以提升材料性能並拓展應用領域。他們正透過建立策略合作關係和長期供應協議來提高生產效率並確保產品品質的穩定性。一些企業正透過開發高純度和功能化衍生物來豐富其產品組合,以滿足先進電子和光伏應用領域不斷變化的需求。此外,許多公司也在最佳化其分銷網路,專注於與關鍵終端用戶建立直接合作關係,以提供客製化解決方案和技術支援。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 陷阱與挑戰

- 機會

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按產品規格

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依產品分類,2021-2034年

- 主要趨勢

- C60(富勒烯)

- 95%純度等級

- 99%純度

- 純度99.5%級

- 純度99.9%

- C70富勒烯

- 標準級

- 高純度

- 官能化富勒烯衍生物

- PCBM([6,6]-苯基-C61-丁酸甲酯)

- ICBA(茚-C60雙加成物)

- 水溶性富勒烯衍生物

- 客製化功能化衍生物

第6章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 研究和實驗室化學品

- 學術與大學研究

- 藥物研發應用

- 材料科學研究

- 政府研究機構

- 商業研究服務

- 電子與有機光伏

- 有機光伏(OPV)應用

- 半導體應用

- 電子元件整合

- 顯示技術應用

- 專業工業應用

- 先進催化劑應用

- 特種塗料及材料

- 摩擦學應用

- 小眾工業用途

- 合約研究與客製合成

- 醫藥合約研究

- 科技公司研發支持

- 客製化衍生品開發

- 專業研究化學服務

第7章:市場估計與預測:依配銷通路分類,2021-2034年

- 主要趨勢

- 直接銷售(製造商對最終用戶)

- 化學品分銷商

- 特種化學品供應商

- 線上化學品市場

第8章:市場估算與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- Nano-C Inc.

- SES Research Inc.

- Solaris Chem

- TCI (Tokyo Chemical Industry)

- Sigma-Aldrich / Merck KGaA

- American Elements

- Strem Chemicals

- Ossila

- Alfa Aesar (Thermo Fisher)

- Frontier Carbon Corporation

- ACS Material

- Abvigen Inc.

The Global Fullerene-Based Specialty Chemicals Market was valued at USD 533 million in 2024 and is estimated to grow at a CAGR of 8.6% to reach USD 1.2 billion by 2034.

Growth momentum is primarily driven by expanding opportunities in organic photovoltaics (OPV) and related electronic applications, supported by significant advancements in fullerene functionalization and synthesis. Enhanced solubility, stability, and electron-accepting properties of C-60 and C-70 fullerenes are accelerating their integration into organic electronics and energy systems. The strong research funding for nanotechnology, coupled with maturing regulatory frameworks and policy incentives, continues to expand the scope of fullerene-based materials across energy, electronics, and pharmaceutical R&D. As the demand for high-performance nanomaterials rises, fullerenes and their derivatives are increasingly recognized for their potential in next-generation devices, flexible electronics, and advanced chemical formulations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $533 Million |

| Forecast Value | $1.2 Billion |

| CAGR | 8.6% |

In 2024, the electronics and OPV segment generated USD 117.3 million, representing a 22% share. The segment continues to thrive on advancements in organic electronics and the growing adoption of solution-processable fullerene derivatives that ensure improved scalability and device performance. The use of these advanced materials in flexible and energy-efficient technologies is fueling further demand across multiple sectors.

The direct sales channel was valued at USD 213.2 million in 2024, captured a 40% share, and is forecast to grow at an 8.6% CAGR through 2034. This channel remains dominant due to the highly specialized nature of fullerene products, which often require tailored specifications, rigorous quality control, and close collaboration between manufacturers and end users such as research organizations, electronics firms, and pharmaceutical companies.

Asia-Pacific Fullerene-Based Specialty Chemicals Market generated USD 255.9 million and held a 48% share in 2024. The region is expected to grow at a 10.2% CAGR during 2025-2034. Strong growth is supported by robust electronics manufacturing capabilities, an extensive chemical supply infrastructure, and active government initiatives promoting nanomaterials and next-generation photovoltaic research. China, Japan, South Korea, and India remain at the forefront of production and innovation, supported by dynamic start-up ecosystems and advanced R&D programs.

Key players operating in the Global Fullerene-Based Specialty Chemicals Market include Nano-C Inc., SES Research Inc., Solaris Chem, TCI (Tokyo Chemical Industry), Sigma-Aldrich / Merck KGaA, American Elements, Strem Chemicals, Ossila, Alfa Aesar (Thermo Fisher), Frontier Carbon Corporation, ACS Material, and Abvigen Inc. Companies in the Fullerene-Based Specialty Chemicals Market are actively investing in research and development to enhance material performance and expand their application base. Strategic collaborations and long-term supply agreements are being formed to strengthen production efficiency and ensure consistent product quality. Several players are diversifying their product portfolios by developing high-purity and functionalized derivatives to meet the evolving needs of advanced electronic and photovoltaic applications. Many firms are also optimizing their distribution networks, focusing on direct partnerships with key end users to provide customized solutions and technical support.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product trends

- 2.2.2 Application trends

- 2.2.3 Distribution Channel trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Drivers

- 3.2.2 Pitfalls & Challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product format

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product, 2021-2034 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 C60 (buckminsterfullerene)

- 5.2.1 95% purity grade

- 5.2.2 99% purity grade

- 5.2.3 99.5% purity grade

- 5.2.4 99.9% purity grade

- 5.3 C70 fullerene

- 5.3.1 Standard grade

- 5.3.2 High purity grade

- 5.4 Functionalized Fullerene Derivatives

- 5.4.1 PCBM ([6,6]-Phenyl-C61-butyric Acid Methyl Ester)

- 5.4.2 ICBA (Indene-C60 Bisadduct)

- 5.4.3 Water-soluble fullerene derivatives

- 5.4.4 Custom functionalized derivatives

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 Research & laboratory chemicals

- 6.2.1 Academic & university research

- 6.2.2 Pharmaceutical R&D applications

- 6.2.3 Material science research

- 6.2.4 Government research institutes

- 6.2.5 Commercial research services

- 6.3 Electronics & organic photovoltaics

- 6.3.1 Organic photovoltaic (OPV) applications

- 6.3.2 Semiconductor applications

- 6.3.3 Electronic component integration

- 6.3.4 Display technology applications

- 6.4 Specialty industrial applications

- 6.4.1 Advanced catalyst applications

- 6.4.2 Specialty coatings & materials

- 6.4.3 Tribological applications

- 6.4.4 Niche industrial uses

- 6.5 Contract research & custom synthesis

- 6.5.1 Pharmaceutical contract research

- 6.5.2 Technology company R&D support

- 6.5.3 Custom derivative development

- 6.5.4 Specialized research chemical services

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021-2034 (USD Million & Kilo Tons)

- 7.1 Key trends

- 7.2 Direct sales (manufacturer to end use)

- 7.3 Chemical distributors

- 7.4 Specialty chemical suppliers

- 7.5 Online chemical marketplaces

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Million & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Nano-C Inc.

- 9.2 SES Research Inc.

- 9.3 Solaris Chem

- 9.4 TCI (Tokyo Chemical Industry)

- 9.5 Sigma-Aldrich / Merck KGaA

- 9.6 American Elements

- 9.7 Strem Chemicals

- 9.8 Ossila

- 9.9 Alfa Aesar (Thermo Fisher)

- 9.10 Frontier Carbon Corporation

- 9.11 ACS Material

- 9.12 Abvigen Inc.