|

市場調查報告書

商品編碼

1876616

車輛側翻預防系統市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Vehicle Rollover Prevention System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

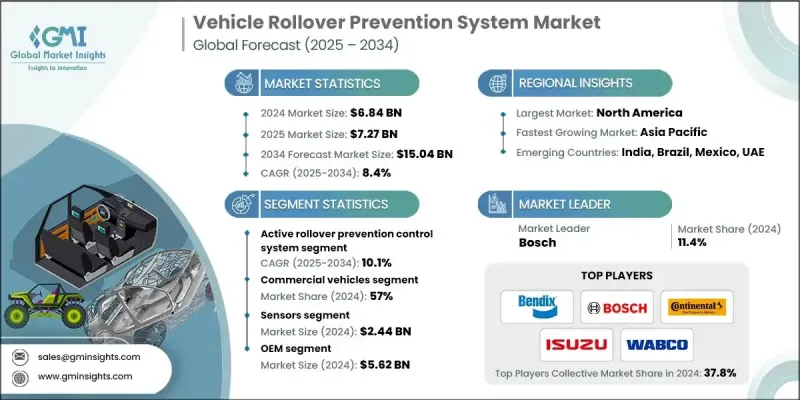

2024 年全球車輛翻車預防系統市場價值為 68.4 億美元,預計到 2034 年將以 8.4% 的複合年成長率成長至 150.4 億美元。

SUV、皮卡和重型商用車等高重心車輛的日益普及推動了市場的穩定擴張,這些車輛的翻車風險也隨之增加。這一趨勢促使汽車製造商和零件供應商將先進的電子穩定控制系統和側翻預防系統整合到車輛設計中。現代安全解決方案採用運動感測技術、預測演算法和智慧煞車系統來偵測和減輕側翻事故。全球範圍內日益嚴格的政府安全法規,特別是那些強制要求配備電子穩定控制系統 (ESC) 和其他翻車預防措施的法規,正在加速此類系統在新車中的創新和應用。這些法規已在主要汽車市場實施,促使製造商開發高度整合且反應迅速的安全平台,旨在降低道路交通事故死亡率。 MEMS 感測器技術、即時資料分析和機器學習演算法的不斷進步進一步提高了這些系統的精確度和響應速度。這些改進透過降低誤報率、最佳化車輛穩定性以及提高系統經濟性來推動市場需求,從而共同促進乘用車和商用車領域的更廣泛應用。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 68.4億美元 |

| 預測值 | 150.4億美元 |

| 複合年成長率 | 8.4% |

主動防側翻控制系統市場預計在2025年至2034年間將以10.1%的複合年成長率成長。這些系統將電子穩定控制系統(ESC)與智慧型感測器和執行器網路結合,提供主動式車輛穩定性管理。它們持續分析側傾角、橫向力和偏航運動,以檢測潛在的側翻情況。一旦識別到不穩定情況,系統會自動施加選擇性煞車或降低引擎扭矩,以穩定車輛並防止側翻,從而確保在動態駕駛條件下獲得更好的操控性。

感測器領域佔據35.7%的市場佔有率,預計2024年市場規模將達24.4億美元。該領域的成長主要得益於微機電系統(MEMS)技術的快速發展,這項技術在提高感測器精度的同時降低了成本。諸如內建機器學習核心等創新技術使感測器能夠自主檢測駕駛模式並即時識別側翻風險。這些進步為感測器與先進駕駛輔助系統(ADAS)和連網汽車平台的無縫整合鋪平了道路,從而提升了車輛安全性和跨多個動態功能的性能協同效應。

2024年,美國車輛翻車預防系統市場佔87.3%的市場佔有率,營收達18.9億美元。美國在該領域的領先地位得益於其完善的汽車安全法規、成熟的技術生態系統以及乘用車和商用車車隊對先進安全系統的廣泛應用。美國市場持續受益於其多元化的車輛結構和對創新的重視,未來十年將擁有巨大的成長潛力。

全球車輛翻車預防系統市場的主要參與者包括博世、大陸集團、威伯科、奧托立夫、皓龍、曼恩商用車、瑪魯蒂鈴木、五十鈴汽車和本迪克斯。這些領導企業正致力於透過技術進步、合作和市場擴張來提升自身的競爭優勢。許多企業正大力投資研發,以開發更智慧、更具適應性的控制系統,利用機器學習和先進感測器實現車輛的即時監控。汽車製造商與技術供應商之間的策略合作正在推動整合安全平台的構建,將側翻預防功能與更廣泛的穩定性控制功能相結合。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基準估算和計算

- 基準年計算

- 市場估算的關鍵趨勢

- 初步研究和驗證

- 原始資料

- 預報

- 研究假設和局限性

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- SUV和卡車需求不斷成長

- 更嚴格的全球安全法規

- 感測器和人工智慧技術的進步

- 消費者和安全意識提高

- 商業和非道路應用領域的成長

- 產業陷阱與挑戰

- 系統成本高且整合複雜

- 各地區標準化程度有限

- 市場機遇

- 與自動駕駛和ADAS平台整合

- 電動和混合動力汽車的擴張

- 車隊安全和遠端資訊處理技術應用成長

- 透過在地化實現新興市場採納

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 資料隱私與監管合規

- 波特的分析

- PESTEL 分析

- 技術與創新格局

- 目前技術

- 新興技術

- 感測器技術演進與路線圖

- 按車輛細分市場分類的技術採納曲線

- 專利分析

- 價格趨勢分析

- 按組件

- 按地區

- 成本分解分析

- 生產統計

- 生產中心

- 消費中心

- 進出口

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

- 車輛翻車事故統計及趨勢

- 安全影響評估與生命挽救分析

- 軟體演算法開發趨勢

- 風險評估與市場波動框架

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 重要新聞和舉措

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估算與預測:依系統分類,2021-2034年

- 主要趨勢

- 翻車偵測及預警系統

- 主動防側翻控制系統

- 橫滾穩定性控制系統(RSC)

- 翻滾保護結構(ROPS)

第6章:市場估價與預測:依車輛類型分類,2021-2034年

- 主要趨勢

- 搭乘用車

- 轎車

- 掀背車

- SUV

- 商用車輛

- 低容量性狀

- MCV

- C型肝炎

第7章:市場估計與預測:依組件分類,2021-2034年

- 主要趨勢

- 感應器

- 電子控制單元

- 執行器和煞車模組

- 其他

第8章:市場估算與預測:依銷售管道分類,2021-2034年

- 主要趨勢

- 原始設備製造商(OEM)

- 售後市場

第9章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 個人車輛所有者

- 車隊營運商和物流公司

- 政府和公共交通機構

- 工業和建築公司

第10章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐

- 荷蘭

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳新銀行

- 新加坡

- 泰國

- 越南

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- 全球參與者

- Bosch

- Continental

- WABCO

- Knorr-Bremse

- Advics

- ZF Friedrichshafen

- Hyundai Mobis

- Mando

- 區域玩家

- Bendix

- Isuzu Motors

- MAN Truck & Bus

- Maruti Suzuki

- Autoliv

- Infineon Technologies

- STMicroelectronics

- 新興及小眾玩家

- Tenneco

- Schaeffler

- BorgWarner

- Haldex

- BWI

The Global Vehicle Rollover Prevention System Market was valued at USD 6.84 billion in 2024 and is estimated to grow at a CAGR of 8.4% to reach USD 15.04 billion by 2034.

The steady expansion of the market is driven by the rising adoption of SUVs, pickup trucks, and heavy commercial vehicles with higher centers of gravity, which increases rollover risks. This trend has encouraged automakers and component suppliers to integrate advanced electronic stability and rollover prevention systems into vehicle design. Modern safety solutions now employ motion-sensing technologies, predictive algorithms, and intelligent braking systems to detect and mitigate rollover incidents. Increasingly stringent government safety mandates worldwide, particularly those enforcing electronic stability control (ESC) and other rollover countermeasures, are accelerating innovation and deployment of such systems in new vehicles. These mandates, implemented across major automotive regions, are pushing manufacturers to develop highly integrated and responsive safety platforms aimed at reducing road fatalities. Continuous advancements in MEMS sensor technology, real-time data analytics, and machine learning algorithms are further enhancing the precision and responsiveness of these systems. This improvement is driving market demand by lowering false alarms, optimizing vehicle stability performance, and improving system affordability, which collectively support broader adoption across both passenger and commercial vehicle segments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.84 Billion |

| Forecast Value | $15.04 Billion |

| CAGR | 8.4% |

The active rollover prevention control system segment is projected to grow at a CAGR of 10.1% from 2025 to 2034. These systems merge electronic stability control (ESC) with smart sensors and actuator networks to provide proactive vehicle stability management. They continuously analyze roll angles, lateral forces, and yaw movements to detect potential rollover conditions. When instability is identified, the system automatically applies selective braking or reduces engine torque to stabilize the vehicle and prevent rollover, ensuring improved control under dynamic driving conditions.

The sensors segment held a 35.7% share, valued at USD 2.44 billion in 2024. The segment's growth is driven by rapid progress in Micro-Electro-Mechanical Systems (MEMS) technology, which enhances sensor accuracy while reducing costs. Innovations such as built-in machine learning cores enable sensors to autonomously detect driving patterns and identify rollover risks in real time. These advancements are paving the way for seamless integration into advanced driver assistance systems (ADAS) and connected vehicle platforms, promoting enhanced vehicle safety and performance synergy across multiple dynamic functions.

United States Vehicle Rollover Prevention System Market held 87.3% share in 2024, generating USD 1.89 billion in revenue. The country's leadership is supported by well-established automotive safety regulations, a mature technology ecosystem, and significant adoption of advanced safety systems in both passenger and commercial fleets. The US market continues to benefit from its robust vehicle mix and focus on innovation, offering substantial opportunities for further growth in the next decade.

Major companies active in the Global Vehicle Rollover Prevention System Market include Bosch, Continental, WABCO, Autoliv, Haldex, MAN Truck & Bus, Maruti Suzuki, Isuzu Motors, and Bendix. Leading companies in the Vehicle Rollover Prevention System Market are pursuing strategies focused on technological advancement, collaboration, and market expansion to enhance their competitive positioning. Many are investing heavily in R&D to develop smarter, more adaptive control systems that leverage machine learning and advanced sensors for real-time vehicle monitoring. Strategic partnerships between automakers and technology providers are fostering integrated safety platforms combining rollover prevention with broader stability control functions.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 System

- 2.2.2 Vehicle

- 2.2.3 Component

- 2.2.4 Sales channel

- 2.2.5 End Use

- 2.2.6 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising SUV and truck demand

- 3.2.1.2 Stricter global safety regulations

- 3.2.1.3 Advancements in sensor and AI technologies

- 3.2.1.4 Increased consumer and safety awareness

- 3.2.1.5 Growth in commercial and off-road applications

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High system cost and complex integration

- 3.2.2.2 Limited standardization across regions

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with autonomous and ADAS platforms

- 3.2.3.2 Expansion in electric and hybrid vehicles

- 3.2.3.3 Growth in fleet safety and telematics adoption

- 3.2.3.4 Emerging market adoption through localization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle east and Africa

- 3.4.6 Data Privacy & Regulatory Compliance

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technology

- 3.7.2 Emerging technology

- 3.7.3 Sensor Technology Evolution & Roadmap

- 3.7.4 Technology Adoption Curves by Vehicle Segment

- 3.8 Patent analysis

- 3.9 Price Trends Analysis

- 3.9.1 By component

- 3.9.2 By region

- 3.10 Cost Breakdown Analysis

- 3.11 Production statistics

- 3.11.1 Production hubs

- 3.11.2 Consumption hubs

- 3.11.3 Export and import

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

- 3.14 Vehicle Rollover Accident Statistics & Trends

- 3.15 Safety Impact Assessment & Lives Saved Analysis

- 3.16 Software Algorithm Development Trends

- 3.17 Risk Assessment & Market Volatility Framework

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key news and initiatives

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By System, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Rollover detection & warning system

- 5.3 Active rollover prevention control system

- 5.4 Roll stability control (RSC) system

- 5.5 Rollover protection structure (ROPS)

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Sedan

- 6.2.2 Hatchback

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 LCV

- 6.3.2 MCV

- 6.3.3 HCV

Chapter 7 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Sensors

- 7.3 Electronic control unit

- 7.4 Actuators & braking module

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Original Equipment Manufacturer (OEM)

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 Individual Vehicle Owners

- 9.3 Fleet Operators & Logistics Companies

- 9.4 Government & Public Transport Agencies

- 9.5 Industrial & Construction Firms

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Netherlands

- 10.3.8 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 ANZ

- 10.4.5 Singapore

- 10.4.6 Thailand

- 10.4.7 Vietnam

- 10.4.8 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Bosch

- 11.1.2 Continental

- 11.1.3 WABCO

- 11.1.4 Knorr-Bremse

- 11.1.5 Advics

- 11.1.6 ZF Friedrichshafen

- 11.1.7 Hyundai Mobis

- 11.1.8 Mando

- 11.2 Regional Players

- 11.2.1 Bendix

- 11.2.2 Isuzu Motors

- 11.2.3 MAN Truck & Bus

- 11.2.4 Maruti Suzuki

- 11.2.5 Autoliv

- 11.2.6 Infineon Technologies

- 11.2.7 STMicroelectronics

- 11.3 Emerging & Niche Players

- 11.3.1 Tenneco

- 11.3.2 Schaeffler

- 11.3.3 BorgWarner

- 11.3.4 Haldex

- 11.3.5 BWI

汽車車道警報系統市場 - 全球產業規模、佔有率、趨勢、機會、預測:按功能類型、需求類別、車輛類型、感測器類型、地區和競爭格局分類,2021-2031年

汽車車道警報系統市場 - 全球產業規模、佔有率、趨勢、機會、預測:按功能類型、需求類別、車輛類型、感測器類型、地區和競爭格局分類,2021-2031年 碰撞警報系統市場:按組件、車輛類型、技術、銷售管道和應用分類-2026-2032年全球市場預測

碰撞警報系統市場:按組件、車輛類型、技術、銷售管道和應用分類-2026-2032年全球市場預測 2026年全球汽車前向碰撞警報系統市場報告2026年全球汽車車道警報系統市場報告2026年全球自動軌道預警系統市場報告2026年全球駕駛員疲勞偵測攝影機市場報告堆高機行人警示系統市場:按組件、技術、最終用戶和銷售管道分類-2026-2032年全球市場預測主動和被動車輛安全系統市場(按主動系統、被動系統、公路車輛和非公路車輛分類),全球預測,2026-2032年按分銷管道、車輛類型、自動駕駛等級和技術分類的前向碰撞警報系統市場-2026-2032年全球預測

2026年全球汽車前向碰撞警報系統市場報告2026年全球汽車車道警報系統市場報告2026年全球自動軌道預警系統市場報告2026年全球駕駛員疲勞偵測攝影機市場報告堆高機行人警示系統市場:按組件、技術、最終用戶和銷售管道分類-2026-2032年全球市場預測主動和被動車輛安全系統市場(按主動系統、被動系統、公路車輛和非公路車輛分類),全球預測,2026-2032年按分銷管道、車輛類型、自動駕駛等級和技術分類的前向碰撞警報系統市場-2026-2032年全球預測 自動軌道警告系統的全球市場

自動軌道警告系統的全球市場