|

市場調查報告書

商品編碼

1876600

數位表現型分析市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Digital Phenotyping Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

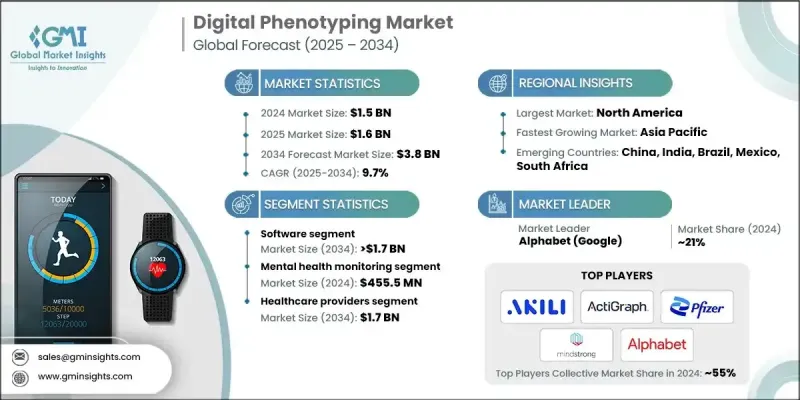

2024 年全球數位表現型市場價值為 15 億美元,預計到 2034 年將以 9.7% 的複合年成長率成長至 38 億美元。

慢性病和精神健康問題的日益增多,以及智慧型手機和穿戴式健康設備的廣泛普及,推動了市場成長。這些技術透過感測器被動地、持續地收集資料,追蹤運動、心率、睡眠模式和位置。收集到的資料構成了數位表現型系統的基礎,支持健康監測和行為分析。人工智慧 (AI) 和機器學習 (ML) 的日益融合,透過實現預測分析、個人化治療和疾病早期檢測,進一步改變了市場格局。此外,數位表現型透過行動裝置互動、語音和活動資料捕捉人類行為的細微變化,正在重新定義行為研究和臨床試驗。這一新興領域正在革新醫療保健,提供以往難以客觀衡量的患者健康和生活方式模式的洞察。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 15億美元 |

| 預測值 | 38億美元 |

| 複合年成長率 | 9.7% |

2024年,軟體領域佔據43.3%的市場佔有率,預計到2034年將達到17億美元,複合年成長率(CAGR)為10.1%。此領域涵蓋雲端平台和本地部署平台。軟體在數位表現型分析中發揮著至關重要的作用,它能夠利用智慧型手機和穿戴式感測器即時收集和分析行為及生理資料。這些系統中的人工智慧和機器學習技術有助於進行預測建模、異常檢測和持續行為監測。該領域的成長動力源於其能夠為臨床醫生和研究人員提供超越傳統臨床環境的可操作性見解,從而改善患者參與度和健康管理效果,並應用於心理和生理健康領域。

2024年,心理健康監測市場規模預計將達到4.555億美元。焦慮症、憂鬱症和躁鬱症等心理健康問題的盛行率在全球範圍內持續上升,加速了對可擴展、技術驅動心理健康解決方案的需求。新冠疫情的持續影響進一步加劇了這一需求,促使人們更多地採用能夠進行持續客觀監測的數位化工具。數位表現型分析應用程式利用智慧型手機資料和人機互動來評估心理健康狀況,從而提供早期預警訊號,提示可能出現的困擾或行為變化。這種方法透過提供經濟實惠、遠距且無歧視的替代方案,有助於彌合心理健康服務可近性方面的差距,取代傳統的治療模式。

預計到2024年,北美數位表現型分析市場將佔據44.6%的佔有率。該地區的領先地位得益於強大的醫療基礎設施、智慧型手機的高普及率以及穿戴式技術的早期應用。北美企業正迅速將人工智慧和機器學習功能融入數位表現型分析平台,實現個人化治療方案的製定、預測性分析以及提升患者參與度。先進的技術生態系統和積極的醫療創新相結合,使該地區成為數位表現型分析應用的關鍵成長中心。

全球數位表現型分析市場的主要參與者包括 Akili Interactive Labs、AliveCor、Fitbit、羅氏、葛蘭素史克、ActiGraph、HumanAPI、Mindstrong、Alphabet(Google)、Onnela Lab、諾華、賽諾菲、武田製藥和輝瑞。數位表現型分析市場的領導企業正採用多種策略來增強其競爭優勢和市場地位。許多企業正在投資先進的人工智慧和機器學習演算法,以提升預測能力並提供個人化的健康洞察。各公司正在擴大與醫療服務提供者、研究機構和數位健康新創公司的策略合作,以加速資料整合和臨床驗證。此外,各公司也致力於產品多元化,提供基於雲端和混合平台的服務,以滿足不同終端用戶的需求。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 每個階段的價值增加

- 影響價值鏈的因素

- 產業影響因素

- 成長促進因素

- 精神健康和慢性疾病盛行率不斷上升

- 智慧型手機和穿戴式裝置的日益普及

- 轉向以價值為導向和預防性醫療的轉變日益明顯

- 遠距醫療和遠距監測的日益普及

- 產業陷阱與挑戰

- 資料隱私問題、監管挑戰

- 缺乏標準化

- 市場機遇

- 拓展至臨床試驗及製藥領域

- 日益關注行為研究與人口健康分析

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 美國

- 加拿大

- 歐洲

- 亞太地區

- 北美洲

- 技術格局

- 當前技術趨勢

- 新興技術

- 未來市場趨勢

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依組件分類,2021-2034年

- 主要趨勢

- 硬體

- 穿戴式裝置

- 生物感測器

- 其他連接的設備

- 軟體

- 基於雲端的

- 現場

- 服務

第6章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 心理健康監測

- 慢性病管理

- 行為研究

- 睡眠和運動分析

- 神經退化性疾病

- 其他應用

第7章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 醫療保健提供者

- 付款人

- 製藥公司

- 其他最終用途

第8章:市場估算與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Akili Interactive Labs

- ActiGraph

- AliveCor

- Alphabet (Google)

- F. Hoffmann-La Roche

- Fitbit

- GlaxoSmithKline

- HumanAPI

- Mindstrong

- Novartis

- Onnela lab

- Pfizer

- Sanofi

- Takeda Pharmaceuticals

The Global Digital Phenotyping Market was valued at USD 1.5 billion in 2024 and is estimated to grow at a CAGR of 9.7% to reach USD 3.8 billion by 2034.

Market growth is propelled by the increasing incidence of chronic diseases and mental health conditions, along with the widespread adoption of smartphones and wearable health devices. These technologies enable passive, continuous data collection through sensors that track movement, heart rate, sleep patterns, and location. The collected data form the foundation of digital phenotyping systems, supporting health monitoring and behavioral analysis. The growing integration of artificial intelligence (AI) and machine learning (ML) is further transforming the market by enabling predictive analytics, personalized treatments, and early disease detection. Additionally, digital phenotyping is redefining behavioral research and clinical trials by capturing subtle changes in human behavior through mobile device interactions, speech, and activity data. This evolving field is revolutionizing healthcare by providing insights into patient health and lifestyle patterns that were previously difficult to measure objectively.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $3.8 Billion |

| CAGR | 9.7% |

The software segment held a 43.3% share in 2024 and is expected to reach USD 1.7 billion by 2034, growing at a CAGR of 10.1%. This segment includes both cloud-based and on-premises platforms. Software plays a critical role in digital phenotyping by enabling the real-time collection and analysis of behavioral and physiological data using smartphone and wearable sensors. AI and ML technologies within these systems facilitate predictive modeling, anomaly detection, and continuous behavioral monitoring. The segment's growth is driven by its ability to provide actionable insights for clinicians and researchers beyond traditional clinical settings, improving patient engagement and health management outcomes across both mental and physical health applications.

The mental health monitoring segment captured USD 455.5 million in 2024. The prevalence of mental health disorders such as anxiety, depression, and bipolar disorder continues to rise worldwide, accelerating the need for scalable, technology-driven mental health solutions. The lingering effects of the COVID-19 pandemic have amplified this demand, leading to increased adoption of digital tools that allow for continuous and objective monitoring. Digital phenotyping applications use smartphone-based data and human-computer interactions to evaluate mental well-being, providing early warning signs of distress or behavioral changes. This approach helps bridge accessibility gaps in mental healthcare by offering affordable, remote, and stigma-free alternatives to traditional therapy models.

North America Digital Phenotyping Market held a 44.6% share in 2024. The region's leadership is driven by strong healthcare infrastructure, high smartphone usage, and early adoption of wearable technologies. Companies in North America are rapidly incorporating AI and ML capabilities into digital phenotyping platforms, enabling personalized treatment planning, predictive analysis, and improved patient engagement. The combination of advanced technological ecosystems and proactive healthcare innovation has positioned the region as a key growth hub for digital phenotyping adoption.

Major players in the Global Digital Phenotyping Market include Akili Interactive Labs, AliveCor, Fitbit, F. Hoffmann-La Roche, GlaxoSmithKline, ActiGraph, HumanAPI, Mindstrong, Alphabet (Google), Onnela Lab, Novartis, Sanofi, Takeda Pharmaceuticals, and Pfizer. Leading companies in the Digital Phenotyping Market are employing multiple strategies to strengthen their competitive edge and market position. Many are investing in advanced AI and ML algorithms to enhance predictive capabilities and deliver personalized health insights. Firms are expanding strategic collaborations with healthcare providers, research organizations, and digital health startups to accelerate data integration and clinical validation. Companies are also focusing on product diversification, offering cloud-based and hybrid platforms to serve varied end users.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Component trends

- 2.2.3 Application trends

- 2.2.4 End Use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Value addition at each stage

- 3.1.2 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of mental health and chronic conditions

- 3.2.1.2 Increasing proliferation of smartphones and wearables

- 3.2.1.3 Growing shift toward value-based and preventive care

- 3.2.1.4 Increasing expansion of telehealth and remote monitoring

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data privacy concerns, regulatory challenges

- 3.2.2.2 Lack of standardization

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into clinical trials and pharma

- 3.2.3.2 Growing focus on behavioral research and population health analytics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Component, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Wearables

- 5.2.2 Biosensors

- 5.2.3 Other connected devices

- 5.3 Software

- 5.3.1 Cloud-based

- 5.3.2 On-premises

- 5.4 Services

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Mental health monitoring

- 6.3 Chronic disease management

- 6.4 Behavioral research

- 6.5 Sleep and movement analysis

- 6.6 Neurodegenerative disorders

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Healthcare providers

- 7.3 Payers

- 7.4 Pharmaceutical companies

- 7.5 Other End Use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Akili Interactive Labs

- 9.2 ActiGraph

- 9.3 AliveCor

- 9.4 Alphabet (Google)

- 9.5 F. Hoffmann-La Roche

- 9.6 Fitbit

- 9.7 GlaxoSmithKline

- 9.8 HumanAPI

- 9.9 Mindstrong

- 9.10 Novartis

- 9.11 Onnela lab

- 9.12 Pfizer

- 9.13 Sanofi

- 9.14 Takeda Pharmaceuticals

數位心理治療市場規模、佔有率和成長分析:按產品、適應症、交付方式、最終用戶、年齡層、部署模式和地區分類-2026-2033年產業預測

數位心理治療市場規模、佔有率和成長分析:按產品、適應症、交付方式、最終用戶、年齡層、部署模式和地區分類-2026-2033年產業預測 2034年強迫症(OCD)數位治療藥物市場預測:按治療方法、給藥平台、經營模式、最終用戶和地區分類的全球分析

2034年強迫症(OCD)數位治療藥物市場預測:按治療方法、給藥平台、經營模式、最終用戶和地區分類的全球分析 精準精神科市場-全球產業規模、佔有率、趨勢、機會、預測:生物標記、樣本、技術、應用、終端用戶、區域及競爭格局,2021-2031年數位心理治療市場預測至2034年—按類型、解決方案、經營模式、應用、最終用戶和地區分類的全球分析數位表現型分析市場-全球產業規模、佔有率、趨勢、機會和預測:按資料流、設備類型、應用、地區和競爭格局分類,2021-2031年

精準精神科市場-全球產業規模、佔有率、趨勢、機會、預測:生物標記、樣本、技術、應用、終端用戶、區域及競爭格局,2021-2031年數位心理治療市場預測至2034年—按類型、解決方案、經營模式、應用、最終用戶和地區分類的全球分析數位表現型分析市場-全球產業規模、佔有率、趨勢、機會和預測:按資料流、設備類型、應用、地區和競爭格局分類,2021-2031年 個人化心理健康醫療市場:按類型、治療領域和地區分類

個人化心理健康醫療市場:按類型、治療領域和地區分類 精準精神病學市場報告:按產品類型、檢體、生物標記類型、技術、應用、最終用戶和地區分類(2026-2034 年)

精準精神病學市場報告:按產品類型、檢體、生物標記類型、技術、應用、最終用戶和地區分類(2026-2034 年) 個人化精神病學市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、最終用戶、部署方式和設備分類數位心理治療市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、最終用戶、部署類型和功能分類

個人化精神病學市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、最終用戶、部署方式和設備分類數位心理治療市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、最終用戶、部署類型和功能分類 隔離罐市場規模、佔有率和成長分析(按類型、材質、應用、價格範圍、通路和地區分類)-2026-2033年產業預測

隔離罐市場規模、佔有率和成長分析(按類型、材質、應用、價格範圍、通路和地區分類)-2026-2033年產業預測