|

市場調查報告書

商品編碼

1876588

固態雷射雷達半導體元件市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Solid-State LiDAR Semiconductor Components Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

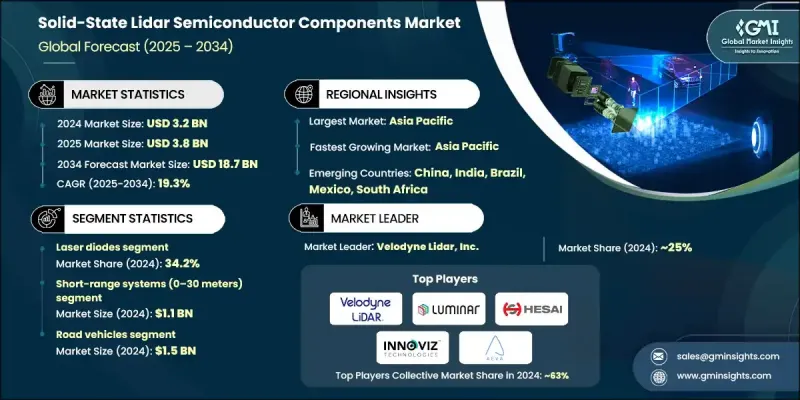

2024 年全球固態雷射雷達半導體元件市場價值為 32 億美元,預計到 2034 年將以 19.3% 的複合年成長率成長至 187 億美元。

這一成長歸功於雷射雷達技術在自動駕駛汽車、高級駕駛輔助系統 (ADAS) 和工業自動化流程中的快速整合。與機械式雷射雷達相比,固態雷射雷達具有更優異的性能、更高的耐用性和更低的成本,因此越來越受到製造商的青睞。其基於半導體的設計支援更快的資料採集、更高的精度以及與車輛和機器人系統的無縫整合。這些特性使得在複雜環境中實現精確的3D地圖繪製、物體識別和導航成為可能,而這些特性對於下一代行動解決方案至關重要。現代車輛中 ADAS 的日益普及推動了對緊湊、節能和高解析度半導體組件的需求,這些組件能夠增強即時環境感知能力。這些組件正成為車輛安全和自動化系統不可或缺的一部分,為自適應巡航控制、碰撞偵測和車道維持輔助等技術的創新提供了支援。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 32億美元 |

| 預測值 | 187億美元 |

| 複合年成長率 | 19.3% |

2024年,雷射二極體市佔率達到34.2%。雷射二極體在發光和測距方面發揮核心作用,是雷射雷達(LiDAR)技術的基礎。它們能夠產生高密度、高強度的光束,從而實現高精度的地圖繪製和目標檢測,這在汽車、機器人和工業領域至關重要。半導體設計和材料工程的持續創新正在幫助提高雷射二極體的效率、熱性能和使用壽命。採用氮化鎵(GaN)和磷化銦(InP)等先進材料進一步最佳化了功率輸出,降低了能耗,並提升了雷射雷達系統的整體性能。這些改進對於滿足自動駕駛和智慧基礎設施應用領域對可靠性和成本效益日益成長的行業需求至關重要。

2024年,短程(0-30公尺)LiDAR系統市場規模預計將達11億美元。這些系統因其在短距離應用中的精度和效率而備受青睞,例如高級駕駛輔助系統(ADAS)、工業機器人和自動化機械。它們能夠提供高解析度資料,對於在擁擠或城市環境中進行障礙物檢測、導航和碰撞預防等任務至關重要。短程LiDAR解決方案因其體積小、功耗低和價格實惠而備受青睞,非常適合整合到車輛、無人機和小型機器人系統中。停車感應器、盲點偵測和行人安全系統等技術的日益普及正在推動其進一步應用。光學整合和半導體小型化技術的不斷進步持續提升著這些短程雷射雷達組件的精度、性能和可靠性。

預計到2024年,北美固態雷射雷達半導體組件市場佔有率將達到29.4%。該地區市場成長的主要驅動力是自動駕駛汽車研發、高級駕駛輔助系統(ADAS)應用以及智慧基礎設施項目的大力投資。先進的研究計畫、政府激勵措施以及技術開發商和半導體製造商之間的合作,正在加速商業化進程。該地區完善的半導體生態系統和製造技術的快速發展,為創新和規模化生產提供了強大支撐。此外,國防、工業自動化和機器人等領域日益成長的需求,也鞏固了北美在高性能雷射雷達半導體組件領域的領先地位。

固態雷射測距儀半導體元件市場的主要企業包括:Aeva Technologies, Inc.、Velodyne LiDAR, Inc.、ams OSRAM AG、LeddarTech Inc.、Innoviz Technologies Ltd.、Broadcom Inc.、Luminar Technologies, Inc.、STMicroelectronics NV、RoboSense(S. Incorporated(現為Coherent Corp.)、Analog Devices, Inc.、Quanergy Systems, Inc.、索尼半導體解決方案公司、瑞薩電子、安森美半導體(onsemi)和合賽科技股份有限公司。這些企業正致力於技術創新、產品多元化和策略合作,以鞏固其市場地位。業界領導者正大力投資研發,以開發高效能半導體材料,例如氮化鎵(GaN)和磷化銦(InP),從而提升雷射雷達(LiDAR)性能並降低生產成本。LiDAR開發商、汽車原始設備製造商(OEM)和半導體製造商之間的策略合作,正在推動自動駕駛和工業應用領域的整合發展。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 產業影響因素

- 成長促進因素

- 自動駕駛汽車的日益普及推動了對高性能固態雷射雷達感測器的需求。

- 高級駕駛輔助系統 (ADAS) 對緊湊、節能的半導體元件的需求日益成長。

- LiDAR在工業自動化和智慧基礎設施項目的應用日益廣泛。

- 半導體材料(如碳化矽 (SiC) 和磷化銦 (InP))的技術進步。

- 產業陷阱與挑戰

- 雷射二極體和光電探測器的製造成本高。

- LiDAR組件供應商之間的標準化和互通性有限。

- 市場機遇

- 自主無人機和機器人領域對固態雷射雷達的需求日益成長。

- 政府資助的智慧城市和基礎設施數位化計畫。

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 美國

- 加拿大

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 北美洲

- 技術格局

- 當前趨勢

- 新興技術

- 管道分析

- 未來市場趨勢

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依產品/組件類型分類,2021-2034年

- 主要趨勢

- 雷射二極體

- 邊發射雷射二極體(EEL)

- 垂直腔面發射雷射(VCSEL)

- 分佈式回饋(DFB)雷射二極體

- 紅外線感測器(固態)

- 單光子雪崩二極體(SPAD)

- 雪崩光電二極體(APD)

- 矽光電倍增管(SiPM)

- InGaAs光電偵測器

- CMOS影像感測器

- 積體電路

- 時間數字轉換器 (TDC)

- 類比數位轉換器(ADC)

- 跨阻放大器(TIA)

- 雷射驅動電路

- 其他

- 光電裝置

第6章:市場估算與預測:依性能等級/範圍等級分類,2021-2034年

- 主要趨勢

- 短程系統(0-30公尺)

- 中程系統(30-150公尺)

- 遠端系統(150-300公尺)

- 超遠端系統(300公尺以上)

第7章:市場估計與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 道路車輛

- 工業製造

- 政府與國防

第8章:市場估算與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Velodyne LiDAR, Inc.

- Luminar Technologies, Inc.

- Aeva Technologies, Inc.

- Innoviz Technologies Ltd.

- Ouster, Inc.

- Quanergy Systems, Inc.

- LeddarTech Inc.

- Hesai Technology Co., Ltd.

- RoboSense (Suteng Innovation Technology Co., Ltd.)

- Sony Semiconductor Solutions Corporation

- Hamamatsu Photonics KK

- ams OSRAM AG

- STMicroelectronics NV

- Infineon Technologies AG

- ON Semiconductor Corporation (onsemi)

- Broadcom Inc.

- Texas Instruments Incorporated

- Analog Devices, Inc.

- II-VI Incorporated (now Coherent Corp.)

- Renesas Electronics Corporation

The Global Solid-State LiDAR Semiconductor Components Market was valued at USD 3.2 billion in 2024 and is estimated to grow at a CAGR of 19.3% to reach USD 18.7 billion by 2034.

The growth is attributed to the rapid integration of LiDAR technology into autonomous vehicles, advanced driver-assistance systems (ADAS), and industrial automation processes. Solid-state LiDAR offers superior performance, greater durability, and lower costs compared to mechanical alternatives, making it increasingly preferred by manufacturers. Its semiconductor-based design supports faster data acquisition, enhanced precision, and seamless integration into vehicles and robotic systems. These features enable accurate 3D mapping, object recognition, and navigation in complex environments, all essential for next-generation mobility solutions. The growing adoption of ADAS in modern vehicles is fueling demand for compact, energy-efficient, and high-resolution semiconductor components that enhance real-time environmental awareness. These components are becoming integral to vehicle safety and automation systems, supporting innovations in adaptive cruise control, collision detection, and lane assistance technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.2 Billion |

| Forecast Value | $18.7 Billion |

| CAGR | 19.3% |

In 2024, the laser diodes segment held a 34.2% share. Laser diodes play a central role in light emission and distance measurement, forming the backbone of LiDAR technology. Their ability to produce concentrated, high-intensity light beams allows for highly accurate mapping and object detection, which are vital in automotive, robotics, and industrial sectors. Continuous innovation in semiconductor design and material engineering is helping improve laser diode efficiency, thermal performance, and operational lifespan. The adoption of advanced materials such as gallium nitride (GaN) and indium phosphide (InP) is further optimizing power output, reducing energy consumption, and enhancing the overall performance of LiDAR systems. These improvements are essential to meet growing industry demands for reliability and cost-effectiveness across autonomous mobility and smart infrastructure applications.

The short-range systems (0-30 meters) segment generated USD 1.1 billion in 2024. These systems are favored for their precision and efficiency in short-distance applications, including ADAS, industrial robotics, and automated machinery. They provide high-resolution data critical for tasks such as obstacle detection, navigation, and collision prevention in congested or urban environments. Short-range LiDAR solutions are valued for their small form factor, lower power requirements, and affordability, making them well-suited for integration into vehicles, drones, and compact robotic systems. The growing deployment of technologies such as parking sensors, blind-spot detection, and pedestrian safety systems is driving further adoption. Ongoing progress in optical integration and semiconductor miniaturization continues to elevate the accuracy, performance, and reliability of these short-range LiDAR components.

North America Solid-State LiDAR Semiconductor Components Market held a 29.4% share in 2024. Market growth in the region is driven by strong investments in autonomous vehicle development, ADAS implementation, and smart infrastructure projects. Advanced research initiatives, coupled with government incentives and collaborations between technology developers and semiconductor manufacturers, are accelerating commercialization. The region's well-established semiconductor ecosystem and rapid advancements in manufacturing technologies are supporting innovation and scalability. Additionally, increasing demand from sectors such as defense, industrial automation, and robotics is reinforcing North America's leadership position in high-performance LiDAR semiconductor components.

Prominent companies operating in the Solid-State LiDAR Semiconductor Components Market include Aeva Technologies, Inc., Velodyne LiDAR, Inc., ams OSRAM AG, LeddarTech Inc., Innoviz Technologies Ltd., Broadcom Inc., Luminar Technologies, Inc., STMicroelectronics N.V., RoboSense (Suteng Innovation Technology Co., Ltd.), Ouster, Inc., Hamamatsu Photonics K.K., Texas Instruments Incorporated, Infineon Technologies AG, II-VI Incorporated (now Coherent Corp.), Analog Devices, Inc., Quanergy Systems, Inc., Sony Semiconductor Solutions Corporation, Renesas Electronics Corporation, ON Semiconductor Corporation (onsemi), and Hesai Technology Co., Ltd. Companies in the Solid-State LiDAR Semiconductor Components Market are focusing on technological innovation, product diversification, and strategic partnerships to strengthen their market position. Leading players are investing heavily in R&D to develop high-efficiency semiconductor materials, such as GaN and InP, that enhance LiDAR performance and reduce production costs. Strategic collaborations between LiDAR developers, automotive OEMs, and semiconductor manufacturers are expanding integration across autonomous and industrial applications.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional Trends

- 2.2.2 Product/Component Type Trends

- 2.2.3 Performance Tier / Range Class Trends

- 2.2.4 Application Trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing adoption of autonomous vehicles fueling demand for high-performance solid-state LiDAR sensors.

- 3.2.1.2 Rising need for compact, energy-efficient semiconductor components in advanced driver-assistance systems (ADAS).

- 3.2.1.3 Increasing integration of LiDAR in industrial automation and smart infrastructure projects.

- 3.2.1.4 Technological advancements in semiconductor materials such as silicon carbide (SiC) and indium phosphide (InP).

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing costs of laser diodes and photodetectors.

- 3.2.2.2 Limited standardization and interoperability across LiDAR component suppliers.

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for solid-state LiDAR in autonomous drones and robotics.

- 3.2.3.2 Government-funded smart city and infrastructure digitization projects.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.4.1 North America

- 3.5 Technology landscape

- 3.5.1 Current trends

- 3.5.2 Emerging technologies

- 3.6 Pipeline analysis

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 Middle East and Africa

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product/Component Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Laser Diodes

- 5.2.1 Edge-Emitting Laser Diodes (EEL)

- 5.2.2 Vertical-Cavity Surface-Emitting Lasers (VCSEL)

- 5.2.3 Distributed Feedback (DFB) Laser Diodes

- 5.3 Infrared Sensors (Solid-State)

- 5.3.1 Single Photon Avalanche Diodes (SPAD)

- 5.3.2 Avalanche Photodiodes (APD)

- 5.3.3 Silicon Photomultipliers (SiPM)

- 5.3.4 InGaAs Photodetectors

- 5.3.5 CMOS Image Sensors

- 5.4 Integrated Microcircuits

- 5.4.1 Time-to-Digital Converters (TDC)

- 5.4.2 Analog-to-Digital Converters (ADC)

- 5.4.3 Transimpedance Amplifiers (TIA)

- 5.4.4 Laser Driver Circuits

- 5.4.5 Others

- 5.5 Optoelectronic Devices

Chapter 6 Market Estimates and Forecast, By Performance Tier / Range Class, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Short-Range Systems (0-30 meters)

- 6.3 Medium-Range Systems (30-150 meters)

- 6.4 Long-Range Systems (150-300 meters)

- 6.5 Ultra-Long-Range Systems (300+ meters)

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Road vehicles

- 7.3 Industrial manufacturing

- 7.4 Government & defense

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Velodyne LiDAR, Inc.

- 9.2 Luminar Technologies, Inc.

- 9.3 Aeva Technologies, Inc.

- 9.4 Innoviz Technologies Ltd.

- 9.5 Ouster, Inc.

- 9.6 Quanergy Systems, Inc.

- 9.7 LeddarTech Inc.

- 9.8 Hesai Technology Co., Ltd.

- 9.9 RoboSense (Suteng Innovation Technology Co., Ltd.)

- 9.10 Sony Semiconductor Solutions Corporation

- 9.11 Hamamatsu Photonics K.K.

- 9.12 ams OSRAM AG

- 9.13 STMicroelectronics N.V.

- 9.14 Infineon Technologies AG

- 9.15 ON Semiconductor Corporation (onsemi)

- 9.16 Broadcom Inc.

- 9.17 Texas Instruments Incorporated

- 9.18 Analog Devices, Inc.

- 9.19 II-VI Incorporated (now Coherent Corp.)

- 9.20 Renesas Electronics Corporation