|

市場調查報告書

商品編碼

1876567

Omega-3脂肪酸市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Omega-3 Fatty Acids Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

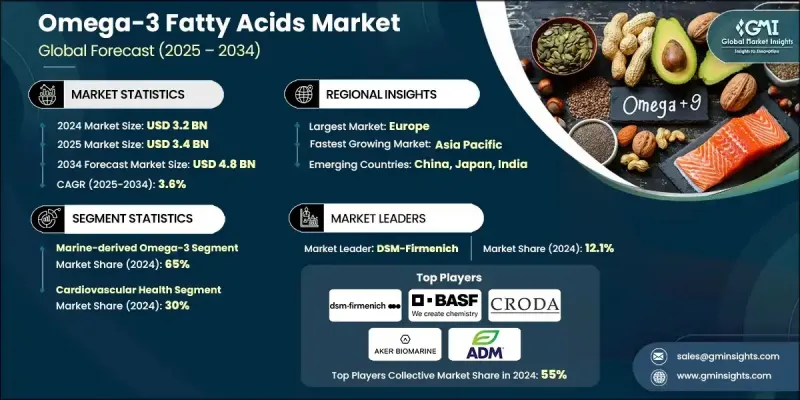

2024 年全球 Omega-3 脂肪酸市場價值為 32 億美元,預計到 2034 年將以 3.6% 的複合年成長率成長至 48 億美元。

越來越多的科學研究凸顯了ω-3脂肪酸的健康益處,這是推動市場成長的主要動力。目前已有超過4萬篇關於EPA和DHA的同儕審查研究,其中包括數千項臨床試驗,證實了它們對心血管、大腦和眼睛健康的積極作用,消費者對ω-3的認知度持續提升。大眾對預防性健康和營養的日益重視,推動了對ω-3補充劑的需求,尤其是那些針對心臟和認知健康的補充劑。人們對功能性食品和強化食品的廣泛興趣進一步促進了市場發展,食品和飲料生產商將ω-3成分添加到烘焙食品、乳製品和飲料等日常食品中。人們逐漸將ω-3納入日常營養,而非僅依賴膳食補充劑,這正在拓展市場應用範圍,並為各地區的長期成長前景奠定基礎。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 32億美元 |

| 預測值 | 48億美元 |

| 複合年成長率 | 3.6% |

受消費者對永續和植物來源產品的強勁需求推動,藻類來源的ω-3產品市場預計到2034年將以3.9%的複合年成長率成長。微藻養殖技術的快速發展和人們環保意識的不斷增強提升了該品類的吸引力。藻油是更乾淨、更濃縮的EPA和DHA來源,因此只需服用少量即可,並消除了傳統海洋來源ω-3產品的常見魚腥味等問題。這項優勢正助力植物來源的ω-3產品在膳食補充劑和強化食品配方領域獲得更大的市場佔有率。

2024年,一般保健品和膳食補充劑佔據了24%的市場佔有率,反映出消費者對omega-3產品在維持整體健康和預防慢性疾病方面的認可度很高。這些品類繼續受益於零售和線上通路的高可及性,儘管不同學名藥的臨床療效仍存在差異。功能性食品和強化食品約佔16%的市場佔有率,這得益於製造商不斷進行產品創新,將omega-3添加到飲料、烘焙食品和乳製品中,以滿足消費者對營養便捷食品的需求。

2024年美國ω-3脂肪酸市場規模為7.813億美元,預計到2034年將達到11億美元。北美市場環境成熟,消費者擁有完善的膳食補充劑消費習慣,並且對健康益處的認知度不斷提高。美國是該地區市場的領頭羊,佔據北美約83%的市場佔有率,這得益於其廣泛的零售分銷、直銷模式以及醫療專業人士的推薦。美國的監管環境保持穩定,FDA的監管以及ω-3成分的GRAS(公認安全)認證進一步增強了消費者的信心。

全球ω-3脂肪酸市場的主要參與者包括帝斯曼-菲美意(DSM-Firmenich)、巴斯夫(BASF SE)、科萊恩(Croda International)、阿克生物海洋(Aker BioMarine)、ADM(Archer Daniels Midland)、嘉吉(Cargill)、科比恩(Corbion)、歐米加製藥公司(Ogam)集團。 ω-3脂肪酸市場的領導企業正積極推行策略舉措,以鞏固其市場地位並拓展全球業務。許多企業正致力於永續採購,投資藻類ω-3生產,以減少對海洋資源的依賴。此外,各公司也透過先進的純化技術提升產品品質,並最佳化EPA/DHA濃度水平,以滿足消費者多樣化的需求。策略併購和合作正幫助主要生產商拓展供應鏈網路,並進入新的區域市場。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 產業陷阱與挑戰

- 市場機遇

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場規模及預測:依產品類型分類,2021-2034年

- 主要趨勢

- 海洋來源的ω-3

- 魚油

- 濃縮魚油

- 磷蝦油和磷脂形式

- 其他

- 藻類來源的ω-3

- 微藻油

- 發酵法提取的EPA和DHA

- 植物性ω-3(ALA)

- 亞麻仁油

- 奇亞籽油

- 其他

- 處方ω-3藥物

- 濃縮和純化形式

第6章:市場規模及預測:依應用領域分類,2021-2034年

- 主要趨勢

- 心血管健康

- 第一級預防產品

- 二級預防方案

- 血壓管理

- 預防心律不整

- 高三酸甘油脂血症治療

- 嚴重高三酸甘油酯血症

- 中度高三酸甘油酯血症

- 一般健康與膳食補充劑

- 每日營養

- 大腦健康與認知功能

- 眼部健康與視力支持

- 關節健康與炎症

- 功能性食品與強化

- 乳製品

- 烘焙食品和糖果

- 飲料強化

- 肉類和家禽

- 嬰幼兒及孕產婦營養

- 嬰兒配方奶粉應用

- 懷孕及產後補充劑

- 兒科營養產品

- 動物飼料和水產養殖

- 水產飼料

- 寵物食品

- 牲畜飼料

第7章:市場規模及預測:依最終用途產業分類,2021-2034年

- 主要趨勢

- 製藥業

- 營養保健品和膳食補充品產業

- 食品飲料業

- 動物飼料業

第8章:市場規模及預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- DSM-Firmenich

- BASF SE

- Croda International

- Aker BioMarine

- Archer Daniels Midland

- Cargill

- Corbion

- Omega Protein Corporation

- Epax

- KD Pharma Group

- Polaris Nutritional Lipids

- Solutex

- Veramaris

- Yield10 Bioscience

- AlgaeCytes

- Fermentalg

- Qualitas Health

The Global Omega-3 Fatty Acids Market was valued at USD 3.2 billion in 2024 and is estimated to grow at a CAGR of 3.6% to reach USD 4.8 billion by 2034.

The expanding body of scientific research highlighting the health advantages of omega-3 fatty acids is a major driver of market growth. With over 40,000 peer-reviewed studies on EPA and DHA, including thousands of clinical trials confirming their positive effects on cardiovascular, brain, and eye health, consumer awareness continues to rise. Increasing public awareness of preventive health and nutrition is fueling demand for omega-3 supplements, particularly those targeting heart and cognitive health. The broader interest in functional and fortified food products further propels the market, as food and beverage manufacturers integrate omega-3 ingredients into everyday items such as baked goods, dairy, and beverages. The move toward incorporating omega-3 into daily nutrition rather than relying solely on dietary supplements is expanding market applications and supporting long-term growth prospects across regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.2 Billion |

| Forecast Value | $4.8 Billion |

| CAGR | 3.6% |

The algal-derived omega-3 segment is expected to grow at a CAGR of 3.9% through 2034, driven by strong consumer interest in sustainable and plant-based sources. The rapid advancement of microalgae cultivation technologies and increasing awareness of environmental concerns have boosted this category's appeal. Algal oil offers a cleaner and more concentrated source of EPA and DHA, enabling smaller doses and eliminating issues such as the fishy odor often associated with traditional marine-based omega-3 products. This advantage is helping plant-based alternatives gain greater traction in both dietary supplements and fortified food formulations.

In 2024, the general wellness and dietary supplements held a 24% share, reflecting strong consumer acceptance of omega-3 products for maintaining overall health and preventing chronic conditions. These categories continue to benefit from high accessibility through retail and online channels, although the clinical efficacy among different generic products remains variable. Functional foods and fortification represented around 16% of the market, supported by ongoing product innovation as manufacturers incorporate omega-3 into beverages, bakery items, and dairy products to meet consumer demand for nutritious and convenient options.

United States Omega-3 Fatty Acids Market was valued at USD 781.3 million in 2024 and is projected to reach USD 1.1 billion by 2034. North America represents a mature market environment, characterized by well-established supplement consumption habits and heightened consumer awareness of health and wellness benefits. The United States leads the regional market, holding around 83% of North American sales, supported by extensive retail distribution, direct-to-consumer marketing, and medical professional recommendations. The regulatory landscape in the U.S. remains stable, and consumer confidence is reinforced through FDA oversight and GRAS (Generally Recognized as Safe) certifications for omega-3 ingredients.

Key participants in the Global Omega-3 Fatty Acids Market include DSM-Firmenich, BASF SE, Croda International, Aker BioMarine, Archer Daniels Midland, Cargill, Corbion, Omega Protein Corporation, Epax, and KD Pharma Group. Leading players in the Omega-3 Fatty Acids Market are pursuing strategic initiatives to strengthen their market positions and expand global reach. Many are focusing on sustainable sourcing by investing in algal-based omega-3 production to reduce dependence on marine resources. Companies are also enhancing product quality through advanced purification technologies and optimizing EPA/DHA concentration levels to meet diverse consumer needs. Strategic mergers, acquisitions, and partnerships are helping major manufacturers expand supply networks and enter new regional markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product Type

- 2.2.2 Application

- 2.2.3 End Use Industry

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Size and Forecast, By Product Type, 2021-2034 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Marine-derived omega-3

- 5.2.1 Fish oil

- 5.2.2 Concentrated fish oil

- 5.2.3 Krill oil & phospholipid forms

- 5.2.4 Others

- 5.3 Algal-derived omega-3

- 5.3.1 Microalgae oil

- 5.3.2 Fermentation-derived EPA & DHA

- 5.4 Plant-based omega-3 (ALA)

- 5.4.1 Flaxseed oil

- 5.4.2 Chia seed oil

- 5.4.3 Others

- 5.5 Prescription omega-3 drugs

- 5.6 Concentrated & purified forms

Chapter 6 Market Size and Forecast, By Application, 2021-2034 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Cardiovascular health

- 6.2.1 Primary prevention products

- 6.2.2 Secondary prevention formulations

- 6.2.3 Blood pressure management

- 6.2.4 Arrhythmia prevention

- 6.3 Hypertriglyceridemia treatment

- 6.3.1 Severe hypertriglyceridemia

- 6.3.2 Moderate hypertriglyceridemia

- 6.4 General wellness & dietary supplements

- 6.4.1 Daily nutrition

- 6.4.2 Brain health & cognitive function

- 6.4.3 Eye health & vision support

- 6.4.4 Joint health & inflammation

- 6.5 Functional foods & fortification

- 6.5.1 Dairy product

- 6.5.2 Bakery & confectionery

- 6.5.3 Beverage fortification

- 6.5.4 Meat & poultry

- 6.6 Infant & maternal nutrition

- 6.6.1 Infant formula applications

- 6.6.2 Prenatal & postnatal supplements

- 6.6.3 Pediatric nutrition products

- 6.7 Animal feed & aquaculture

- 6.7.1 Aquaculture feed

- 6.7.2 Pet food

- 6.7.3 Livestock feed

Chapter 7 Market Size and Forecast, By End Use Industry, 2021-2034 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Pharmaceutical industry

- 7.3 Nutraceutical & dietary supplement industry

- 7.4 Food & beverage industry

- 7.5 Animal feed industry

Chapter 8 Market Size and Forecast, By Region, 2021-2034 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 DSM-Firmenich

- 9.2 BASF SE

- 9.3 Croda International

- 9.4 Aker BioMarine

- 9.5 Archer Daniels Midland

- 9.6 Cargill

- 9.7 Corbion

- 9.8 Omega Protein Corporation

- 9.9 Epax

- 9.10 KD Pharma Group

- 9.11 Polaris Nutritional Lipids

- 9.12 Solutex

- 9.13 Veramaris

- 9.14 Yield10 Bioscience

- 9.15 AlgaeCytes

- 9.16 Fermentalg

- 9.17 Qualitas Health

魚油Omega-3市場報告:趨勢、預測與競爭分析(至 2035 年)

魚油Omega-3市場報告:趨勢、預測與競爭分析(至 2035 年) Omega-3 Omega-3市場規模、佔有率和成長分析:按類型、來源、應用和地區分類-2026年至2033年產業預測

Omega-3 Omega-3市場規模、佔有率和成長分析:按類型、來源、應用和地區分類-2026年至2033年產業預測 Omega-3 原料市場:按類型、原料、應用和地區分類Omega-3軟糖市場:按成分、年齡層、應用、分銷管道和地區分類Omega-3產品市場:依產品類型、通路、原料及地區分類

Omega-3 原料市場:按類型、原料、應用和地區分類Omega-3軟糖市場:按成分、年齡層、應用、分銷管道和地區分類Omega-3產品市場:依產品類型、通路、原料及地區分類 全球Omega-3市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球Omega-3市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 全球Omega-3市場(按類型、來源、應用、形式、製造技術和地區分類)- 預測至 2030 年

全球Omega-3市場(按類型、來源、應用、形式、製造技術和地區分類)- 預測至 2030 年 藻類Omega-3輸液市場預測(至 2032 年):按類型、輸液形式、來源、分銷管道、應用、最終用戶和地區進行的全球分析

藻類Omega-3輸液市場預測(至 2032 年):按類型、輸液形式、來源、分銷管道、應用、最終用戶和地區進行的全球分析 Omega-3和 Omega-6 的全球市場全球微膠囊Omega-3粉市場

Omega-3和 Omega-6 的全球市場全球微膠囊Omega-3粉市場