|

市場調查報告書

商品編碼

1876552

汽車空氣清淨系統市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Automotive Air Purification System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

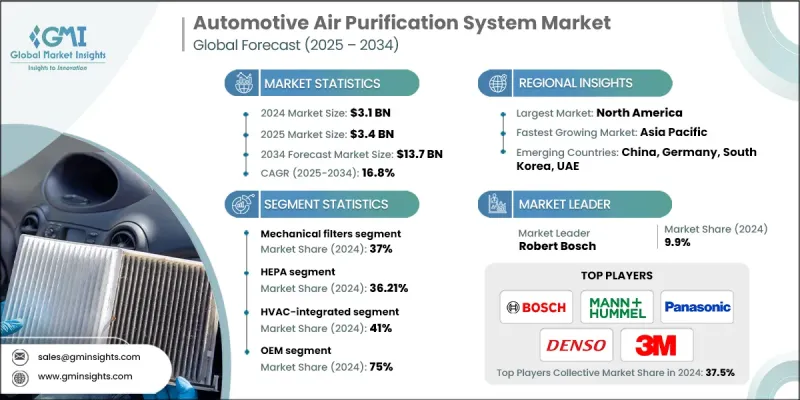

2024 年全球汽車空氣清淨系統市場價值為 31 億美元,預計到 2034 年將以 16.8% 的複合年成長率成長至 137 億美元。

市場成長得益於感測器技術的進步、人工智慧賦能的空氣品質管理以及環保過濾材料的研發。領先的製造商正大力投資於節能、節省空間且智慧化的淨化模組,這些模組能夠與現代暖通空調系統和車載電子設備無縫整合。電裝(Denso)、3M、松下(Panasonic)、博世(Robert Bosch)和曼胡默爾(MANN+HUMMEL)等行業領導者正在推動多級淨化系統的創新,這些系統融合了高效能空氣微粒過濾器(HEPA)、活性碳、電離和紫外線殺菌技術。這些系統不僅提升了乘客的舒適度,還透過可回收的過濾材料和低功耗電子控制,幫助永續發展。城市化進程加快、空氣污染加劇以及消費者對車內空氣品質日益成長的關注,正在推動全球市場需求,而汽車製造商則在新車中整合感測器驅動的空氣管理單元,以滿足消費者對更安全、更健康出行體驗的日益成長的需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 31億美元 |

| 預測值 | 137億美元 |

| 複合年成長率 | 16.8% |

2024 年機械過濾器市佔率為 37%,預計 2025 年至 2034 年將以 13% 的複合年成長率成長。這些過濾器能有效捕捉細懸浮微粒(PM2.5 和 PM10),由於其價格實惠且可靠,因此在OEM和售後市場系統中廣泛應用。

2024 年,HEPA 過濾細分市場佔據 36.21% 的市場佔有率,預計到 2034 年將以 14.3% 的複合年成長率成長。 HEPA 過濾器因其能夠有效捕捉過敏原和細小顆粒,在成本和性能之間實現了最佳平衡,仍然是首選,即使融合多種技術的混合系統越來越受歡迎。

亞太地區汽車空氣清淨系統市場在2024年佔據了48.1%的市場。預計該地區將以17.9%的複合年成長率實現最快成長,到2034年市場規模將達到72.2億美元。強勁的汽車產量、快速的城市化進程以及主要城市的高污染水平是推動市場普及的關鍵因素。日益增強的環保意識、可支配收入的增加以及國內外製造商對空氣淨化技術的積極投資,進一步促進了市場擴張。

汽車空氣清淨系統市場的主要參與者包括3M、夏普、曼胡默爾、博世、松下、電裝、馬瑞利、瑞典CabinAir、SKF和霍尼韋爾。這些公司正採取多種策略來提升市場地位並擴大商業版圖。他們大力投資研發,以開發適用於現代汽車架構的多層淨化系統、節能模組和緊湊型設計。與汽車OEM廠商建立策略合作夥伴關係,確保先進的空氣清淨裝置能夠無縫整合到新車型中。製造商也致力於拓展全球分銷網路,並加強售後市場服務,以滿足持續成長的需求。採用人工智慧賦能的空氣品質管理和混合過濾解決方案是另一項關鍵策略,旨在實現產品差異化並為消費者提供附加價值。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基準估算和計算

- 基準年計算

- 市場估算的關鍵趨勢

- 初步研究和驗證

- 原始資料

- 預測模型

- 研究假設和局限性

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 空氣污染程度上升與健康意識增強

- 嚴格的車輛排放法規和車內空氣品質標準

- 消費者對高階汽車功能的需求不斷成長

- 電動車普及及其獨特的暖通空調需求

- 產業陷阱與挑戰

- 先進淨化技術高昂的初始投資成本

- 與現有暖通空調系統的整合複雜性

- 維護要求及濾芯更換成本

- 新興市場消費者意識有限

- 市場機遇

- 重型設備和採礦業符合 ISO 23875 標準

- 針對現有車隊的售後改裝解決方案

- 與連網車輛技術和物聯網系統的整合

- 新興市場機動化與城市空氣品質問題

- 成長促進因素

- 成長潛力分析

- 監管環境

- 區域一體化法規

- 國際標準協調

- 波特的分析

- PESTEL 分析

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 技術生命週期與成熟度評估

- 依純化方法分類的技術成熟度

- 創新通路與新興技術

- 專利到期時間表與技術商品化

- 顛覆性技術威脅及市場顛覆潛力

- 專利分析

- 成本細分分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

- 顧客行為與購買決策分析

- OEM決策標準和供應商選擇流程

- 售後市場消費者偏好及價格敏感性

- 車隊營運商的要求與投資報酬率考量

- 客戶優先事項的區域差異

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估算與預測:依產品分類,2021-2034年

- 主要趨勢

- 機械過濾器

- 吸附

- 主動滅菌

- 電離和靜電系統

- 整合系統

- 感測器和電子元件

第6章:市場估計與預測:依技術分類,2021-2034年

- 主要趨勢

- 高效能空氣過濾器

- 吸附

- 靜電

- 紫外線/光催化

- 混合

第7章:市場估計與預測:按年計算,2021-2034年

- 主要趨勢

- 暖通空調整合

- 儀表板

- 間接費用

- 座椅下方

- 便攜的

第8章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 個人消費者/零售

- 車隊所有者和租賃營運商

- 大眾運輸業者

- 商業企業

- 政府/緊急服務

第9章:市場估算與預測:依銷售管道分類,2021-2034年

- 主要趨勢

- OEM

- 售後市場

第10章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐

- 葡萄牙

- 克羅埃西亞

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 新加坡

- 泰國

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

第11章:公司簡介

- 全球參與者

- Panasonic

- Denso

- 3 M

- Honeywell

- Robert Bosch

- MANN+HUMMEL

- Sharp

- Marelli

- CabinAir Sweden

- SKF

- Valeo

- Freudenberg Filtration

- BorgWarner

- Donaldson

- 區域玩家

- Hengst

- Camfil

- Hanon Systems

- Visteon

- Parker Hannifin

- K&N Engineering

- 新興參與者

- Philips Automotive

- Johnson Electric

- Filtron

- Sanden

The Global Automotive Air Purification System Market was valued at USD 3.1 billion in 2024 and is estimated to grow at a CAGR of 16.8% to reach USD 13.7 billion by 2034.

Market growth is fueled by advancements in sensor technology, AI-enabled air quality management, and the development of eco-friendly filtration materials. Leading manufacturers are heavily investing in energy-efficient, space-saving, and intelligent purification modules that can seamlessly integrate with modern HVAC systems and vehicle electronics. Industry leaders such as Denso, 3M, Panasonic, Robert Bosch, and MANN+HUMMEL are driving innovation in multi-stage purification systems that incorporate HEPA filters, activated carbon, ionization, and UV sterilization technologies. These systems not only improve passenger comfort but also support sustainability initiatives through recyclable filter materials and low-power electronic controls. Growing urbanization, increasing air pollution, and rising consumer awareness of in-cabin air quality are driving demand globally, while automakers are incorporating sensor-driven air management units in new vehicles to meet the rising need for safer and healthier mobility experiences.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.1 Billion |

| Forecast Value | $13.7 Billion |

| CAGR | 16.8% |

The mechanical filters segment held a 37% share in 2024 and is expected to grow at a CAGR of 13% from 2025 to 2034. These filters efficiently capture fine particulate matter (PM2.5 and PM10) and are widely used in both OEM and aftermarket systems due to their affordability and reliability.

The HEPA filtration segment held a 36.21% share in 2024 and is projected to grow at a CAGR of 14.3% through 2034. HEPA filters remain the preferred choice for their proven ability to trap allergens and fine particles, offering an optimal balance between cost and performance, even as hybrid systems incorporating multiple technologies gain popularity.

Asia-Pacific Automotive Air Purification System Market held a 48.1% share in 2024. The region is expected to achieve the fastest growth at a CAGR of 17.9%, reaching USD 7.22 billion by 2034. Strong automotive production, rapid urbanization, and high pollution levels in major cities are key factors driving adoption. Rising environmental awareness, higher disposable incomes, and active investments from both local and international manufacturers in air purification technologies are further boosting market expansion.

Key players in the Automotive Air Purification System Market include 3M, Sharp, MANN+HUMMEL, Robert Bosch, Panasonic, Denso, Marelli, CabinAir Sweden, SKF, and Honeywell. Companies in the Automotive Air Purification System Market are employing multiple strategies to enhance their market position and expand their footprint. They are investing heavily in R&D to develop multi-stage purification systems, energy-efficient modules, and compact designs suitable for modern vehicle architectures. Strategic partnerships with automotive OEMs ensure seamless integration of advanced air purification units in new vehicle models. Manufacturers are also focusing on expanding their global distribution networks and strengthening aftermarket offerings to capture recurring demand. Adoption of AI-enabled air quality management and hybrid filtration solutions is another key strategy to differentiate products and offer added value to consumers.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Technology

- 2.2.4 Mounting

- 2.2.5 End use

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing Air pollution levels & health awareness

- 3.2.1.2 Stringent vehicle emissions regulations & interior air quality standards

- 3.2.1.3 Rising consumer demand for premium vehicle features

- 3.2.1.4 Electric vehicle adoption & unique HVAC requirements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Initial Investment Costs for Advanced Purification Technologies

- 3.2.2.2 Integration Complexity with Existing HVAC Systems

- 3.2.2.3 Maintenance Requirements & Filter Replacement Costs

- 3.2.2.4 Limited Consumer Awareness in Emerging Markets

- 3.2.3 Market opportunities

- 3.2.3.1 Heavy equipment & mining industry compliance with iso 23875

- 3.2.3.2 Aftermarket retrofit solutions for existing vehicle fleets

- 3.2.3.3 Integration with connected vehicle technologies & iot systems

- 3.2.3.4 Emerging markets motorization & urban air quality concerns

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Regional integration regulations

- 3.4.2 International standards harmonization

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.7.3 Technology Lifecycle & Maturity Assessment

- 3.7.3.1 Technology readiness levels by purification method

- 3.7.3.2 Innovation pipeline & emerging technologies

- 3.7.3.3 Patent expiration timeline & technology commoditization

- 3.7.3.4 Disruptive technology threats & market disruption potential

- 3.8 Patent analysis

- 3.9 Cost breakdown analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.11 Carbon footprint considerations

- 3.12 Customer Behavior & Purchasing Decision Analysis

- 3.12.1 OEM decision-making criteria & vendor selection process

- 3.12.2 Aftermarket consumer preferences & price sensitivity

- 3.12.3 Fleet operator requirements & roi considerations

- 3.12.4 Regional variations in customer priorities

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 (USD Mn, Units)

- 5.1 Key trends

- 5.2 Mechanical filters

- 5.3 Adsorption

- 5.4 Active sterilization

- 5.5 Ionization & electrostatic systems

- 5.6 Integrated systems

- 5.7 Sensors & electronics

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 (USD Mn, Units)

- 6.1 Key trends

- 6.2 HEPA

- 6.3 Adsorption

- 6.4 Electrostatic

- 6.5 UV / photocatalysis

- 6.6 Hybrid

Chapter 7 Market Estimates & Forecast, By Mounting, 2021 - 2034 (USD Mn, Units)

- 7.1 Key trends

- 7.2 HVAC-integrated

- 7.3 Dashboard

- 7.4 Overhead

- 7.5 Under-seat

- 7.6 Portable

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Mn, Units)

- 8.1 Key trends

- 8.2 Individual consumers / retail

- 8.3 Fleet owners & rental operators

- 8.4 Public transport operators

- 8.5 Commercial enterprise

- 8.6 Government / emergency services

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 (USD Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.3.8 Portugal

- 10.3.9 Croatia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Turkey

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Panasonic

- 11.1.2 Denso

- 11.1.3. 3 M

- 11.1.4 Honeywell

- 11.1.5 Robert Bosch

- 11.1.6 MANN+HUMMEL

- 11.1.7 Sharp

- 11.1.8 Marelli

- 11.1.9 CabinAir Sweden

- 11.1.10 SKF

- 11.1.11 Valeo

- 11.1.12 Freudenberg Filtration

- 11.1.13 BorgWarner

- 11.1.14 Donaldson

- 11.2 Regional Players

- 11.2.1 Hengst

- 11.2.2 Camfil

- 11.2.3 Hanon Systems

- 11.2.4 Visteon

- 11.2.5 Parker Hannifin

- 11.2.6 K&N Engineering

- 11.3 Emerging Players

- 11.3.1 Philips Automotive

- 11.3.2 Johnson Electric

- 11.3.3 Filtron

- 11.3.4 Sanden

車載空氣清淨機市場:全球市場預測(按產品類型、技術、電源、車輛類型和銷售管道)- 2026-2032年

車載空氣清淨機市場:全球市場預測(按產品類型、技術、電源、車輛類型和銷售管道)- 2026-2032年 2026年全球高能源效率汽車空氣清淨機市場報告

2026年全球高能源效率汽車空氣清淨機市場報告 車載空氣品質感測器市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測全球汽車空氣清淨機市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

車載空氣品質感測器市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測全球汽車空氣清淨機市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 汽車空氣清淨機市場規模、佔有率和成長分析(按類型、技術、車輛類型、銷售管道和地區分類)-2026-2033年產業預測

汽車空氣清淨機市場規模、佔有率和成長分析(按類型、技術、車輛類型、銷售管道和地區分類)-2026-2033年產業預測 車載空氣品質感測器市場規模、佔有率和成長分析(按感測器類型、技術、車輛類型、銷售管道、應用和地區分類):產業預測(2026-2033 年)

車載空氣品質感測器市場規模、佔有率和成長分析(按感測器類型、技術、車輛類型、銷售管道、應用和地區分類):產業預測(2026-2033 年) 全球商用車空氣乾燥機市場全球車內空氣品質感知器市場全球車用空氣清淨機市場

全球商用車空氣乾燥機市場全球車內空氣品質感知器市場全球車用空氣清淨機市場 自動駕駛汽車感測器市場中的人工智慧,按感測器類型、按車輛類型、按應用、按自主程度、按最終用戶、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測

自動駕駛汽車感測器市場中的人工智慧,按感測器類型、按車輛類型、按應用、按自主程度、按最終用戶、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測