|

市場調查報告書

商品編碼

1876548

汽車數位化工廠自動化市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Automotive Digital Factory Automation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

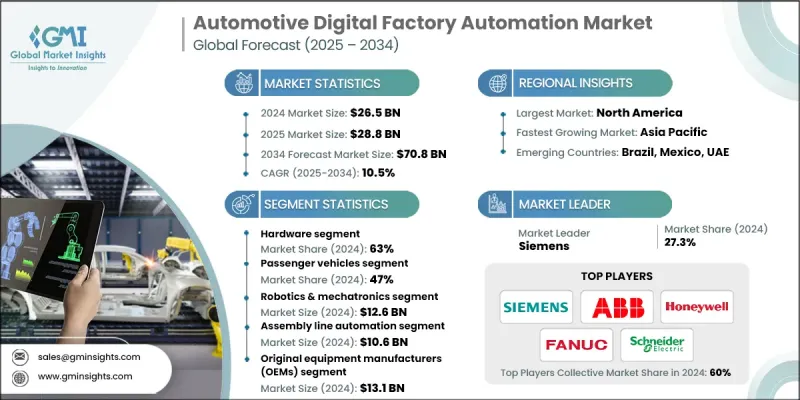

2024 年全球汽車數位化工廠自動化市場價值為 265 億美元,預計到 2034 年將以 10.5% 的複合年成長率成長至 708 億美元。

隨著汽車產業日益擁抱智慧製造和數位轉型,市場正呈現強勁成長動能。製造商正將營運效率、即時資料洞察和靈活的生產系統置於優先地位,以在快速變化的市場環境中保持競爭力。工業4.0技術、人工智慧和物聯網監控平台的整合,正將傳統的汽車工廠轉變為智慧化的、數據驅動的生產環境。這些數位化工廠系統透過預測性維護和自動化過程控制,最佳化生產效率、減少設備停機時間並提升品質保證。透過結合數位孿生模擬、機器人技術、基於人工智慧的分析和物聯網連接,企業實現了整個生產週期的無縫協調。這種融合不僅有助於實現永續發展目標和提高能源效率,還能實現全生命週期可視性、提升合規性並增強製造韌性。對互聯互通、自適應和透明的製造網路日益成長的需求,正推動全球原始設備製造商 (OEM) 和供應商持續投資於數位化工廠自動化。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 265億美元 |

| 預測值 | 708億美元 |

| 複合年成長率 | 10.5% |

2024年,硬體部分約佔市場佔有率的63%,預計2025年至2034年將以10.8%的複合年成長率成長。硬體仍然是汽車數位化工廠自動化的基礎,在實現生產線的即時追蹤、資料採集和機器控制方面發揮著至關重要的作用。關鍵硬體組件包括物聯網感測器、PLC、RFID系統、嵌入式控制器和機器視覺設備,它們確保了無縫運作、預測性維護和高生產力。汽車製造商和供應商依靠這些系統來保持精度、減少誤差並最佳化生產性能,同時實現跨工廠的可擴展數位轉型。

2024年,乘用車市佔率達到47%,預計2025年至2034年間將以11.3%的複合年成長率成長。對電動和混合動力汽車日益成長的需求,以及日益嚴格的環保法規,正在加速乘用車生產自動化領域的投資。汽車製造商正在利用機器人、雲端整合平台和人工智慧分析等數位化工廠解決方案,以提高流程精度、確保合規性並提升生產效率。這些技術能夠即時展現生產指標,並增強企業管理複雜、大量組裝作業的能力,最大限度地減少停機時間。

美國汽車數位化工廠自動化市場佔據88%的市場佔有率,預計2024年市場規模將達85億美元。美國強大的製造業基礎,加上數位化和人工智慧技術的快速普及,正在推動汽車工廠的大規模現代化改造。先進的機器人技術、物聯網監控和數位孿生技術正日益融入生產和供應鏈系統。這種發展有助於提高資源利用率、減少浪費、提升產品質量,同時也有助於實現產業的永續發展和創新目標。

全球汽車數位化工廠自動化市場的主要參與者包括三菱電機、施耐德電氣、發那科、西門子、ABB、艾默生電氣、霍尼韋爾國際、JR自動化技術、羅克韋爾自動化和橫河電機。這些領先企業正致力於技術創新、策略合作和全球擴張,以鞏固其市場地位。他們大力投資先進機器人技術、數位孿生技術和人工智慧驅動的分析,以提高精度並簡化製造流程。自動化供應商與汽車OEM廠商之間的合作正在推動客製化、端到端自動化生態系統的建構。此外,各企業也透過整合節能硬體和利用智慧監控系統最佳化資源利用,來強調永續發展。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 成本結構

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 緩解勞動力短缺的要求

- 品質和一致性改進要求

- 生產靈活性和客製化需求

- 降低成本和提高營運效率的壓力

- 產業陷阱與挑戰

- 高額的初始資本投資要求

- 遺留系統整合挑戰

- 市場機遇

- 工廠中的 5G 網路部署

- 邊緣運算與即時分析

- 區塊鏈輔助供應鏈可追溯性

- 人工智慧驅動的預測性維護擴展

- 成長促進因素

- 成長潛力分析

- 監管環境

- 安全和品質標準

- 環境與永續發展法規

- 資料隱私和網路安全

- 行業特定標準

- 波特的分析

- PESTEL 分析

- 技術與創新格局

- 5G網路在製造業的整合

- 邊緣運算與即時分析

- 區塊鏈輔助供應鏈透明化

- 擴增實境和虛擬實境應用

- 工業系統中的網路安全演變

- 人機介面技術進步

- 數位孿生演化與元宇宙融合

- 自主工廠概念

- 價格趨勢

- 按地區

- 依產品

- 生產統計

- 生產中心

- 消費中心

- 進出口

- 成本細分分析

- 專利分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

- 風險評估框架

- 網路安全風險管理

- 營運風險評估

- 財務風險分析

- 供應鏈風險緩解

- 最佳情況

- 未來展望與策略建議

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估算與預測:依組件分類,2021-2034年

- 主要趨勢

- 硬體

- 工業機器人

- 控制系統

- 感測器和視覺系統

- 人機介面(HMI)

- 其他

- 軟體

- 製造執行系統(MES)

- 數位孿生與模擬軟體

- 預測性維護和分析平台

- 人工智慧和機器學習平台

- ERP/雲端整合

- 服務

- 安裝與調試

- 維護與支援

- 諮詢與系統整合

- 改造和現代化服務

- 培訓與勞動力發展

第6章:市場估價與預測:依車輛類型分類,2021-2034年

- 主要趨勢

- 搭乘用車

- 掀背車

- 轎車

- SUV

- 商用車輛

- 輕型商用車(LCV)

- 中型商用車(MCV)

- 重型商用車(HCV)

- 二輪車

第7章:市場估計與預測:依技術分類,2021-2034年

- 主要趨勢

- 機器人與機電一體化

- 工業物聯網及感測器

- 人工智慧與機器學習

- 數位孿生與仿真

- 雲端運算和邊緣運算

第8章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 裝配線自動化

- 焊接和連接作業

- 塗裝工藝

- 品質控制與檢驗

- 物料搬運與物流

第9章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 原始設備製造商(OEM)

- 一級供應商

- 二級供應商

- 售後市場

第10章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 比利時

- 荷蘭

- 瑞典

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 新加坡

- 韓國

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第11章:公司簡介

- Global Player

- ABB

- Bosch Rexroth

- Emerson Electric

- FANUC

- General Electric

- Honeywell International

- Rockwell Automation

- Schneider Electric

- Siemens

- Regional Player

- Festo

- JR Automation Technologies

- Keyence

- KUKA

- Mitsubishi Electric

- Omron

- UL Solutions

- Vention

- Yokogawa Electric

- 新興參與者

- Augury Systems

- Bright Machines

- MachineMetrics

- Path Robotics

- Sight Machine

- Standard Bots

- Tulip Interfaces

The Global Automotive Digital Factory Automation Market was valued at USD 26.5 billion in 2024 and is estimated to grow at a CAGR of 10.5% to reach USD 70.8 billion by 2034.

The market is experiencing strong momentum as the automotive industry increasingly embraces smart manufacturing and digital transformation. Manufacturers are prioritizing operational efficiency, real-time data insights, and flexible production systems to stay competitive in a rapidly evolving landscape. The integration of Industry 4.0 technologies, artificial intelligence, and IoT-enabled monitoring platforms is transforming traditional automotive facilities into intelligent, data-driven production environments. These digital factory systems optimize productivity, reduce equipment downtime, and enhance quality assurance through predictive maintenance and automated process control. By combining digital twin simulations, robotics, AI-based analytics, and IoT connectivity, companies are achieving seamless coordination across the entire production cycle. This convergence not only supports sustainability goals and energy efficiency but also enables full lifecycle visibility, improved compliance, and greater manufacturing resilience. The growing need for interconnected, adaptive, and transparent manufacturing networks is driving continued investment in digital factory automation across both OEMs and suppliers worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $26.5 Billion |

| Forecast Value | $70.8 Billion |

| CAGR | 10.5% |

The hardware segment accounted for about 63% of the market in 2024 and is anticipated to expand at a CAGR of 10.8% from 2025 to 2034. Hardware remains the foundation of automotive digital factory automation, playing a critical role in enabling real-time tracking, data collection, and machine control throughout production lines. Key hardware elements include IoT sensors, PLCs, RFID systems, embedded controllers, and machine vision devices that ensure seamless operation, predictive maintenance, and high productivity. Automakers and suppliers depend on these systems to maintain precision, reduce errors, and optimize production performance while enabling scalable digital transformation across facilities.

The passenger vehicle segment held 47% share in 2024 and is expected to grow at a CAGR of 11.3% between 2025 and 2034. Rising demand for electric and hybrid vehicles, coupled with stricter environmental regulations, is accelerating automation investments in passenger vehicle production. Automotive manufacturers are leveraging digital factory solutions such as robotics, cloud-integrated platforms, and AI-powered analytics to improve process accuracy, ensure compliance, and increase output efficiency. These technologies provide real-time visibility into production metrics and enhance the ability to manage complex, high-volume assembly operations with minimal downtime.

U.S. Automotive Digital Factory Automation Market held 88% share and generated USD 8.5 billion in 2024. The nation's strong manufacturing base, combined with rapid adoption of digital and AI technologies, is fueling large-scale modernization of automotive plants. Advanced robotics, IoT-enabled monitoring, and digital twin technologies are being increasingly integrated into production and supply chain systems. This expansion supports better resource utilization, reduced waste, and improved product quality while reinforcing the industry's sustainability and innovation goals.

Key players operating in the Global Automotive Digital Factory Automation Market include Mitsubishi Electric, Schneider Electric, FANUC, Siemens, ABB, Emerson Electric, Honeywell International, JR Automation Technologies, Rockwell Automation, and Yokogawa Electric. Leading companies in the Global Automotive Digital Factory Automation Market are focusing on technological innovation, strategic partnerships, and global expansion to strengthen their market presence. They are investing heavily in advanced robotics, digital twin technologies, and AI-driven analytics to enhance precision and streamline manufacturing processes. Collaborations between automation providers and automotive OEMs are enabling the creation of customized, end-to-end automation ecosystems. Companies are also emphasizing sustainability by integrating energy-efficient hardware and optimizing resource utilization through smart monitoring systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 Technology

- 2.2.5 Application

- 2.2.6 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Labor shortage mitigation requirements

- 3.2.1.2 Quality & consistency improvement demands

- 3.2.1.3 Production flexibility & customization needs

- 3.2.1.4 Cost reduction & operational efficiency pressures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial capital investment requirements

- 3.2.2.2 Legacy system integration challenges

- 3.2.3 Market opportunities

- 3.2.3.1 5G network implementation in factories

- 3.2.3.2 Edge computing & real-time analytics

- 3.2.3.3 Blockchain for supply chain traceability

- 3.2.3.4 AI-driven predictive maintenance expansion

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Safety and Quality Standards

- 3.4.2 Environmental and Sustainability Regulations

- 3.4.3 Data Privacy and Cybersecurity

- 3.4.4 Industry-specific Standards

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 5G Network Integration in Manufacturing

- 3.7.2 Edge Computing & Real-time Analytics

- 3.7.3 Blockchain for Supply Chain Transparency

- 3.7.4 Augmented Reality & Virtual Reality Applications

- 3.7.5 Cybersecurity Evolution in Industrial Systems

- 3.7.6 Human-Machine Interface Advancements

- 3.7.7 Digital Twin Evolution & Metaverse Integration

- 3.7.8 Autonomous Factory Concepts

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

- 3.14 Risk assessment framework

- 3.14.1 Cybersecurity risk management

- 3.14.2 Operational risk assessment

- 3.14.3 Financial risk analysis

- 3.14.4 Supply chain risk mitigation

- 3.15 Best case scenarios

- 3.16 Future Outlook & Strategic Recommendations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($ Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Industrial robots

- 5.2.2 Control systems

- 5.2.3 Sensors & vision systems

- 5.2.4 Human-machine interface (HMI)

- 5.2.5 Others

- 5.3 Software

- 5.3.1 Manufacturing execution systems (MES)

- 5.3.2 Digital twin & simulation software

- 5.3.3 Predictive maintenance & analytics platforms

- 5.3.4 AI & machine learning platforms

- 5.3.5 ERP / cloud integration

- 5.4 Services

- 5.4.1 Installation & commissioning

- 5.4.2 Maintenance & support

- 5.4.3 Consulting & system integration

- 5.4.4 Retrofit & modernization services

- 5.4.5 Training & workforce development

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($ Bn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchbacks

- 6.2.2 Sedans

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCV)

- 6.3.2 Medium commercial vehicles (MCV)

- 6.3.3 Heavy commercial vehicles (HCV)

- 6.4 Two-Wheelers

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($ Bn, Units)

- 7.1 Key trends

- 7.2 Robotics & mechatronics

- 7.3 Industrial IoT & sensors

- 7.4 AI & machine learning

- 7.5 Digital twin & simulation

- 7.6 Cloud & edge computing

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($ Bn, Units)

- 8.1 Key trends

- 8.2 Assembly line automation

- 8.3 Welding & joining operations

- 8.4 Painting & coating processes

- 8.5 Quality control & inspection

- 8.6 Material handling & logistics

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($ Bn, Units)

- 9.1 Key trends

- 9.2 Original equipment manufacturers (OEMs)

- 9.3 Tier 1 Suppliers

- 9.4 Tier 2 Suppliers

- 9.5 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($ Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Singapore

- 10.4.6 South Korea

- 10.4.7 Vietnam

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Global Player

- 11.1.1 ABB

- 11.1.2 Bosch Rexroth

- 11.1.3 Emerson Electric

- 11.1.4 FANUC

- 11.1.5 General Electric

- 11.1.6 Honeywell International

- 11.1.7 Rockwell Automation

- 11.1.8 Schneider Electric

- 11.1.9 Siemens

- 11.2 Regional Player

- 11.2.1 Festo

- 11.2.2 JR Automation Technologies

- 11.2.3 Keyence

- 11.2.4 KUKA

- 11.2.5 Mitsubishi Electric

- 11.2.6 Omron

- 11.2.7 UL Solutions

- 11.2.8 Vention

- 11.2.9 Yokogawa Electric

- 11.3 Emerging Players

- 11.3.1 Augury Systems

- 11.3.2 Bright Machines

- 11.3.3 MachineMetrics

- 11.3.4 Path Robotics

- 11.3.5 Sight Machine

- 11.3.6 Standard Bots

- 11.3.7 Tulip Interfaces

人工智慧工廠檢測市場預測至2034年—按部署類型、組件、技術、應用、最終用戶和地區分類的全球分析AI數位化工廠平台市場預測至2034年—按組件、部署模式、技術、應用、最終用戶和地區分類的全球分析數位工廠平台市場預測至2034年—按平台類型、應用、最終用戶和地區分類的全球分析

人工智慧工廠檢測市場預測至2034年—按部署類型、組件、技術、應用、最終用戶和地區分類的全球分析AI數位化工廠平台市場預測至2034年—按組件、部署模式、技術、應用、最終用戶和地區分類的全球分析數位工廠平台市場預測至2034年—按平台類型、應用、最終用戶和地區分類的全球分析 汽車儀錶群市場規模、佔有率、趨勢和預測:叢集類型、車輛類型、銷售管道、應用和地區分類,2026-2034年

汽車儀錶群市場規模、佔有率、趨勢和預測:叢集類型、車輛類型、銷售管道、應用和地區分類,2026-2034年 全球儀錶叢集市場規模、佔有率、趨勢和成長分析報告(2026-2034)汽車智慧工廠市場:策略洞察與預測(2026-2031年)

全球儀錶叢集市場規模、佔有率、趨勢和成長分析報告(2026-2034)汽車智慧工廠市場:策略洞察與預測(2026-2031年) 數位儀錶叢集市場:按顯示技術、解析度、叢集類型、銷售管道和車輛類別分類-2026-2032年全球預測

數位儀錶叢集市場:按顯示技術、解析度、叢集類型、銷售管道和車輛類別分類-2026-2032年全球預測 數位儀錶叢集市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終用戶、功能、安裝類型、解決方案分類2026-2034年全球汽車儀錶叢集市場規模、佔有率、趨勢及成長分析報告

數位儀錶叢集市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終用戶、功能、安裝類型、解決方案分類2026-2034年全球汽車儀錶叢集市場規模、佔有率、趨勢及成長分析報告 2026年全球儀錶叢集市場報告

2026年全球儀錶叢集市場報告