|

市場調查報告書

商品編碼

1876528

經皮腎鏡取石術市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Percutaneous Nephrolithotomy Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

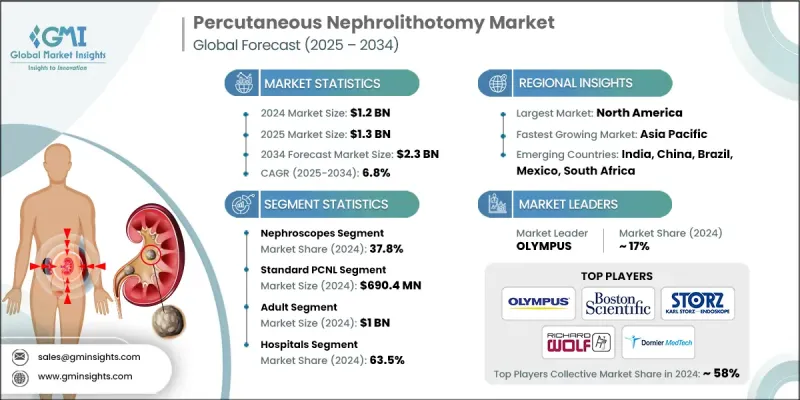

2024 年全球經皮腎鏡取石術市場價值為 12 億美元,預計到 2034 年將以 6.8% 的複合年成長率成長至 23 億美元。

腎結石市場擴張的促進因素包括:腎結石發病率的上升、患者對微創手術的偏好日益成長、經皮腎鏡取石術(PCNL)器械技術的快速發展,以及隨著專科醫療服務可及性的提高而不斷成長的醫療保健支出。微創PCNL手術正逐漸成為治療大型或複雜腎結石的首選方案,尤其適用於無法透過非侵入性或微創技術處理的病例。此手術只需在腎臟上做一個小切口,即可使用腎鏡直接進入腎臟,從而實現精準的結石碎裂和取出,最大限度地減少組織損傷,並縮短恢復時間。發展中國家外科基礎設施的擴建以及政府為改善泌尿外科醫療服務所採取的舉措,進一步推動了手術量的成長,並使更多患者能夠獲得先進的PCNL治療方案。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 12億美元 |

| 預測值 | 23億美元 |

| 複合年成長率 | 6.8% |

由於腎鏡在經皮腎鏡取石術(PCNL)中發揮著不可或缺的作用,預計到2024年,腎鏡市場佔有率將達到37.8%。微型化和數位化腎鏡的日益普及,以及不斷提升視覺化效果和手術精準度的產品創新,鞏固了該領域的領先地位。受肥胖、脫水和高鈉飲食等生活方式因素的影響,泌尿系結石的發生率不斷上升,導致需要進行PCNL手術的患者數量增加,從而直接推動了對高性能腎鏡的需求。

2024年,標準經皮腎鏡取石術(PCNL)市場規模達到6.904億美元,預計2034年將以6.7%的複合年成長率成長。由於其結石清除率優於其他治療方案,標準PCNL仍是去除大於2公分腎結石(包括鹿角狀結石)的首選技術。其已證實的臨床療效確保了該技術在已開發市場和新興市場均持續應用。

2024年,北美經皮腎鏡取石術(PCNL)市佔率達39.8%。該地區是全球腎結石發病率最高的地區之一,其主要促進因素包括肥胖、高鈉攝取、久坐不動的生活方式以及富含加工食品和動物性蛋白質的飲食。這些因素導致PCNL手術需求不斷成長,從而推動了市場的強勁成長。

全球經皮腎鏡取石術市場的主要參與者包括 ADVIN、B. BRAUN、Becton, Dickinson and Company、Boston Scientific、Coloplast、COOK MEDICAL、Dornier MedTech、ELMED、EMS ELECTRO MEDICAL SYSTEMS、KARL STORZ、OLYMPUS、PolyDia0ost、RichardDICAL SYSTEM。經皮腎鏡取石術市場的各公司正透過多種策略措施鞏固其市場地位。他們大力投資研發,以提高設備的效率、小型化程度和成像能力。各公司透過建立合作夥伴關係和開展合作來擴大地域覆蓋範圍並實現產品多元化。策略收購使公司能夠鞏固市場佔有率並獲得創新技術。專注於新興市場能夠抓住新的成長機會。重視先進的數位化和微創解決方案有助於提升競爭優勢。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 產業影響因素

- 成長促進因素

- 腎結石疾病發生率上升

- 微創泌尿外科手術的普及率不斷提高

- PCNL儀器和雷射技術的進步

- 微創經皮腎鏡取石術(mini-PCNL)和微型經皮腎鏡取石術(micro-PCNL)技術越來越受歡迎

- 產業陷阱與挑戰

- PCNL設備和手術費用高昂

- 手術併發症和術後感染的風險

- 市場機遇

- 一次性經皮腎鏡取石術器械的應用日益廣泛

- 新興市場的擴張

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 技術格局

- 當前技術趨勢

- 新興技術

- 報銷方案

- 未來市場趨勢

- 價值鏈分析

- 波特的分析

- PESTEL 分析

- 差距分析

- 創業場景

- 消費者行為洞察

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 亞太地區

- 競爭定位矩陣

- 主要市場參與者的競爭分析

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依產品類型分類,2021-2034年

- 主要趨勢

- 腎鏡

- 死板的

- 靈活的

- 體外碎石系統

- 訪問系統

- 其他產品類型

第6章:市場估計與預測:依手術類型分類,2021-2034年

- 主要趨勢

- 標準PCNL

- 微創經皮腎鏡取石術

- 微型經皮腎鏡取石術

第7章:市場估計與預測:依病患分類,2021-2034年

- 主要趨勢

- 成人

- 兒科

第8章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 醫院

- 門診手術中心

- 其他最終用途

第9章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- ADVIN

- B. BRAUN

- Becton, Dickinson and Company

- Boston Scientific

- Coloplast

- COOK MEDICAL

- Dornier MedTech

- ELMED

- EMS ELECTRO MEDICAL SYSTEMS

- KARL STORZ

- OLYMPUS

- PolyDiagnost

- Richard Wolf

- Teleflex

The Global Percutaneous Nephrolithotomy Market was valued at USD 1.2 billion in 2024 and is estimated to grow at a CAGR of 6.8% to reach USD 2.3 billion by 2034.

Market expansion is driven by the increasing prevalence of kidney stones, growing patient preference for minimally invasive surgical procedures, rapid technological advancements in PCNL devices, and rising healthcare spending with improved access to specialized care. Minimally invasive PCNL procedures are becoming a preferred solution for treating large or complex kidney stones that cannot be addressed by non-invasive or less invasive techniques. The procedure involves a small incision to access the kidney directly using a nephroscope, allowing precise stone fragmentation and removal with minimal tissue damage and reduced recovery time. Expanding surgical infrastructure in developing regions and government initiatives to improve urological care further boost procedure volumes and broaden patient access to advanced PCNL treatment options.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.2 Billion |

| Forecast Value | $2.3 Billion |

| CAGR | 6.8% |

The nephroscopes segment captured a share of 37.8% in 2024 owing to their indispensable role in PCNL procedures. Rising adoption of miniaturized and digital nephroscopes, along with ongoing product innovations enhancing visualization and surgical precision, reinforces the segment's leadership. The growing incidence of urolithiasis, influenced by lifestyle factors such as obesity, dehydration, and high-sodium diets, increases the number of patients requiring PCNL procedures, directly driving demand for high-performance nephroscopes.

The standard PCNL segment generated USD 690.4 million in 2024 and is expected to grow at a CAGR of 6.7% through 2034. Standard PCNL continues to be the preferred technique for removing kidney stones larger than 2 cm, including staghorn stones, due to its superior stone clearance rates compared to other treatment options. Its established clinical effectiveness ensures continued adoption across both developed and emerging markets.

North America Percutaneous Nephrolithotomy Market held a 39.8% share in 2024. The region experiences one of the highest incidences of kidney stones globally, driven by factors such as obesity, high sodium intake, sedentary lifestyles, and diets rich in processed foods and animal protein. These factors contribute to increasing demand for PCNL procedures, supporting strong market growth.

Key players in the Global Percutaneous Nephrolithotomy Market include ADVIN, B. BRAUN, Becton, Dickinson and Company, Boston Scientific, Coloplast, COOK MEDICAL, Dornier MedTech, ELMED, EMS ELECTRO MEDICAL SYSTEMS, KARL STORZ, OLYMPUS, PolyDiagnost, Richard Wolf, and Teleflex. Companies in the Percutaneous Nephrolithotomy Market are strengthening their presence through several strategic approaches. They are investing heavily in research and development to enhance device efficiency, miniaturization, and imaging capabilities. Firms are entering partnerships and collaborations to expand geographic reach and diversify product offerings. Strategic acquisitions allow companies to consolidate market share and acquire innovative technologies. Focused entry into emerging markets captures new growth opportunities. Emphasis on advanced digital and minimally invasive solutions enhances competitive positioning.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Procedure type trends

- 2.2.4 Patient trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of kidney stone disease

- 3.2.1.2 Increasing adoption of minimally invasive urological procedures

- 3.2.1.3 Advancements in PCNL instrumentation and laser technologies

- 3.2.1.4 Growing preference for mini-PCNL and micro-PCNL techniques

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of PCNL equipment and procedures

- 3.2.2.2 Risk of surgical complications and postoperative infections

- 3.2.3 Market opportunities

- 3.2.3.1 Growing adoption of single-use PCNL instruments

- 3.2.3.2 Expansion in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario

- 3.7 Future market trends

- 3.8 Value chain analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Gap analysis

- 3.12 Start-up scenario

- 3.13 Consumer behaviour insights

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Nephroscopes

- 5.2.1 Rigid

- 5.2.2 Flexible

- 5.3 Lithotripsy systems

- 5.4 Access systems

- 5.5 Other product types

Chapter 6 Market Estimates and Forecast, By Procedure Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Standard PCNL

- 6.3 Mini-PCNL

- 6.4 Micro-PCNL

Chapter 7 Market Estimates and Forecast, By Patient, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Adult

- 7.3 Pediatric

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgery centers

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ADVIN

- 10.2 B. BRAUN

- 10.3 Becton, Dickinson and Company

- 10.4 Boston Scientific

- 10.5 Coloplast

- 10.6 COOK MEDICAL

- 10.7 Dornier MedTech

- 10.8 ELMED

- 10.9 EMS ELECTRO MEDICAL SYSTEMS

- 10.10 KARL STORZ

- 10.11 OLYMPUS

- 10.12 PolyDiagnost

- 10.13 Richard Wolf

- 10.14 Teleflex

體外碎石設備市場:依產品類型、方法、應用和最終用戶分類-2026-2032年全球市場預測經經皮腎鏡取石術市場:依產品類型、手術類型、結石類型、入路、病患類型、應用和最終用戶分類-2026-2032年全球市場預測體外震波碎石術市場:依技術、應用、最終用戶、便攜性和治療模式分類-2026-2032年全球市場預測

體外碎石設備市場:依產品類型、方法、應用和最終用戶分類-2026-2032年全球市場預測經經皮腎鏡取石術市場:依產品類型、手術類型、結石類型、入路、病患類型、應用和最終用戶分類-2026-2032年全球市場預測體外震波碎石術市場:依技術、應用、最終用戶、便攜性和治療模式分類-2026-2032年全球市場預測 2026年全球硬式內視鏡碎石市場報告2026年全球體外碎石市場報告

2026年全球硬式內視鏡碎石市場報告2026年全球體外碎石市場報告 2026-2034年全球體外震波碎石設備市場規模、佔有率、趨勢與成長分析報告

2026-2034年全球體外震波碎石設備市場規模、佔有率、趨勢與成長分析報告 體外碎石市場規模、佔有率和成長分析(按手術類型、技術、最終用戶、結石類型和地區分類)-2026-2033年產業預測

體外碎石市場規模、佔有率和成長分析(按手術類型、技術、最終用戶、結石類型和地區分類)-2026-2033年產業預測 體外碎石設備市場-全球產業規模、佔有率、趨勢、機會及預測,依類型、應用、最終用戶、地區及競爭格局分類,2020-2030年預測2025年經皮腎結石全球市場報告

體外碎石設備市場-全球產業規模、佔有率、趨勢、機會及預測,依類型、應用、最終用戶、地區及競爭格局分類,2020-2030年預測2025年經皮腎結石全球市場報告 體外震波碎石術的全球市場

體外震波碎石術的全球市場