|

市場調查報告書

商品編碼

1871308

後生元補充劑市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Postbiotic Supplements Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

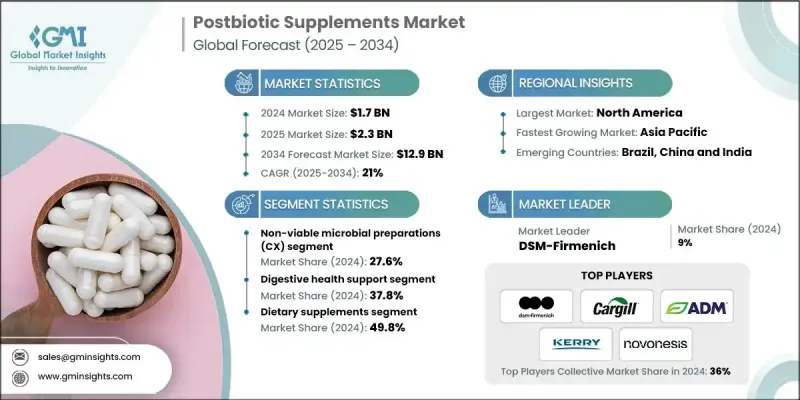

2024 年全球後生元補充劑市場價值為 17 億美元,預計到 2034 年將以 21% 的複合年成長率成長至 129 億美元。

根據國際益生菌和益生元科學協會 (ISAPP) 的官方定義,後生元是指非活性微生物和/或其成分的製劑,它們在失去活性後仍能保持生物活性,從而為宿主帶來健康益處。越來越多的科學證據表明,後生元對健康人群和弱勢群體的消化、免疫和代謝健康都有積極作用。臨床驗證正在加速推進,研究表明,後生元能夠改善糞便品質、腸道屏障功能和呼吸系統健康。這些不斷累積的證據增強了市場信心,並推動了產品線的拓展,從傳統的膠囊和粉末擴展到功能性飲料、能量棒和即食產品,充分利用後生元的熱穩定性,將其融入日常營養補充中。後生元的安全性和穩定性使其特別適用於嬰幼兒、免疫功能低下患者和老年人,臨床試驗進一步證實了其透過短鏈脂肪酸等代謝產物促進腸道健康和發炎控制,從而有益於兒童生長發育和健康老化。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 17億美元 |

| 預測值 | 129億美元 |

| 複合年成長率 | 21% |

2024年,複雜的非活性微生物製劑(CX)佔據了27.6%的市場佔有率,預計到2034年將以20.5%的複合年成長率成長。這些完全去活化的製劑保留了細胞結構和代謝產物,使其能夠達到甚至超越通常由活性益生菌帶來的健康益處。製造商透過採用可控發酵,然後使用經過驗證的去活化方法(通常是熱去活化)來實現這一點,從而保留了膠囊和食品配方中使用的生物活性成分。

膳食補充劑市場佔據49.8%的市場佔有率,預計到2034年將以20.8%的複合年成長率成長。後生元生物活性化合物因其穩定性、安全性和適應性而備受青睞,使其成為膳食補充劑、功能性食品和飲料的理想成分。食品生產商正擴大在零食、飲料和乳製品替代品中添加後生元,以滿足消費者對清潔標籤和有益於腸道菌群產品的需求。膳食補充劑以膠囊、粉末和軟糖等方便服用的形式提供,有助於增強免疫力和促進新陳代謝。後生元在各種加工條件下的穩定性為創新和更廣泛的商業應用鋪平了道路。

2024年,北美後生元補充劑市佔率達41%。這一領先地位得益於臨床醫生的高度認可、消費者意識的提升以及美國和加拿大廣泛的零售管道。美國市場的成長主要由功能性飲料和能量棒推動,這得益於膳食補充劑標籤和健康聲明方面明確的監管指南。在加拿大,消費者對清潔標籤產品的偏好以及對免疫和消化健康的日益關注,支撐了對無需冷藏、劑量簡便且穩定的非活性產品的需求。醫療保健從業者通路的持續高階化以及主流產品上市數量的增加,預計將在預測期內推動市場成長。

全球益生元補充品市場的主要參與者包括:Immuse Health(麒麟控股/協和發酵生物)、Biofarma集團、Culturelle(i-Health公司)、帝斯曼-菲美意、Kerry集團、Metagenics、Probi AB、Ritua、SCD Probiotics、Archers Midland (ADMSLs Midland (ADM)、Samine、Scoson、Sakovs Midland (ADM)、Acoceland (ADM)、Scorpus、Acoson、Sakovs Midland (ADM)。這些公司正積極採取各種策略來鞏固市場地位並維持成長。這些策略包括大力投資研發,以開發具有安全性、有效性和創新健康益處的臨床驗證配方。與學術機構和臨床研究機構的合作有助於加速產品驗證和監管批准。各公司致力於拓展產品組合,推出飲料、能量棒和即食產品等創新形式,以滿足不斷變化的消費者生活方式和偏好。與零售商和醫療保健機構建立策略夥伴關係,有助於擴大分銷範圍並提升消費者信任度。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 消費者對腸腦軸健康益處的認知不斷提高

- 與益生菌相比,具有更優異的穩定性和更長的保存期限。

- ISAPP共識定義後的監管清晰度

- 產業陷阱與挑戰

- 產品表徵的標準化分析方法有限

- 針對特定菌株的臨床驗證需要高額的研發成本

- 市場機遇

- 尚未開發的兒科和老年人群體

- 拓展至功能性食品及飲料應用領域

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品類型

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼說明:僅提供重點國家的貿易統計)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依產品類型分類,2021-2034年

- 主要趨勢

- 複雜的非活性微生物製劑(CX)

- 微生物代謝產物(MM)

- 完整的非活性微生物細胞(IC)

- 微生物細胞碎片(FC)

- 特殊配方

第6章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 消化系統健康支持

- 免疫系統支持

- 代謝健康支持

- 心理健康與認知支持

- 皮膚健康與抗衰老

第7章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 膳食補充劑行業

- 功能性食品和飲料

- 臨床營養

- 化妝品及個人護理

- 動物營養與飼料

第8章:市場估算與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- DSM-Firmenich

- Cargill, Incorporated

- Archer Daniels Midland (ADM)

- Kerry Group Plc

- Chr. Hansen A/S (now Novonesis)

- Immuse Health (Kirin Holdings/Kyowa Hakko Bio)

- SCD Probiotics

- Biofarma Group

- Probi AB

- Culturelle (i-Health, Inc.)

- VSL Pharmaceuticals

- Ritual

- Metagenics

The Global Postbiotic Supplements Market was valued at USD 1.7 billion in 2024 and is estimated to grow at a CAGR of 21% to reach USD 12.9 billion by 2034.

Postbiotics, as officially defined by the International Scientific Association for Probiotics and Prebiotics (ISAPP) are preparations of non-living microorganisms and/or their components that provide health benefits to the host by preserving bioactivity despite the absence of viability. Mounting scientific evidence supports their positive effects on digestive, immune, and metabolic health across both healthy individuals and vulnerable groups. Clinical validation is gaining momentum, with studies showing improvements in stool quality, gut barrier function, and respiratory health. This growing body of proof is driving market confidence and broadening product offerings beyond traditional capsules and powders to include functional beverages, bars, and ready-to-eat products, leveraging the heat stability of postbiotics for daily nutrition integration. Their safety and stability make them especially suitable for infants, immunocompromised patients, and older adults, with clinical trials reinforcing their benefits for pediatric growth and healthy aging through metabolites like short-chain fatty acids that support gut health and inflammation control.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.7 Billion |

| Forecast Value | $12.9 Billion |

| CAGR | 21% |

The complex non-viable microbial preparations (CX) held a 27.6% share in 2024 and are expected to grow at a CAGR of 20.5% through 2034. These fully inactivated preparations maintain cellular structures and metabolites, enabling them to meet or even exceed the health benefits typically attributed to live probiotics. Manufacturers achieve this by employing controlled fermentation followed by validated inactivation methods, often thermal, which preserves the bioactive components used in capsule and food formulations.

The dietary supplements segment held a 49.8% share and is forecasted to grow at a CAGR of 20.8% through 2034. Postbiotic bioactive compounds are favored for their stability, safety, and adaptability, making them ideal for use in dietary supplements, functional foods, and beverages. Food producers are increasingly incorporating postbiotics to fortify snacks, drinks, and dairy alternatives, responding to consumer demand for clean-label and microbiome-supportive products. Supplements are offered in user-friendly forms like capsules, powders, and gummies, supporting immune health and metabolic function. The resilience of postbiotics under various processing conditions paves the way for innovation and wider commercial availability.

North America Postbiotic Supplements Market held a 41% share in 2024. This leadership is fueled by strong clinician acceptance, heightened consumer awareness, and extensive retail distribution across the U.S. and Canada. The U.S. market is driving growth through functional beverages and bars, supported by clear regulatory guidelines on labeling and health claims in dietary supplements. In Canada, the preference for clean-label products and growing interest in immune and digestive wellness sustain demand for stable, non-viable formats that do not require refrigeration and offer simple dosing. The ongoing premiumization within healthcare practitioner channels, combined with expanding mainstream product launches, is expected to propel market growth during the forecast period.

Key industry players in the Global Postbiotic Supplements Market include Immuse Health (Kirin Holdings/Kyowa Hakko Bio), Biofarma Group, Culturelle (i-Health, Inc.), DSM-Firmenich, Kerry Group Plc, Metagenics, Probi AB, Ritua, SCD Probiotics, Archer Daniels Midland (ADM), Cargill, Incorporated, Chr. Hansen A/S (now Novonesis), VSL Pharmaceuticals, and Labcorp. Companies in the Postbiotic Supplements Market are actively adopting strategies to strengthen their market presence and sustain growth. These include investing heavily in R&D to develop clinically validated formulations that highlight safety, efficacy, and novel health benefits. Collaborations with academic institutions and clinical research organizations help accelerate product validation and regulatory approval. Firms focus on expanding product portfolios by launching innovative formats such as beverages, bars, and ready-to-eat items that cater to evolving consumer lifestyles and preferences. Strategic partnerships with retailers and healthcare providers enhance distribution reach and consumer trust.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application

- 2.2.4 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing consumer awareness of gut-brain axis health benefits

- 3.2.1.2 Superior stability & shelf-life advantages over probiotics

- 3.2.1.3 Regulatory clarity following ISAPP consensus definition

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited standardized analytical methods for product characterization

- 3.2.2.2 High R&D costs for strain-specific clinical validation

- 3.2.3 Market opportunities

- 3.2.3.1 Untapped pediatric & elderly population segments

- 3.2.3.2 Expansion into functional foods & beverage applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Complex non-viable microbial preparations (CX)

- 5.3 Microbial metabolic products (MM)

- 5.4 Intact non-viable microbial cells (IC)

- 5.5 Fragmented microbial cells (FC)

- 5.6 Specialized formulations

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Digestive health support

- 6.3 Immune system support

- 6.4 Metabolic health support

- 6.5 Mental health & cognitive support

- 6.6 Skin health & anti-aging

Chapter 7 Market Estimates and Forecast, By End Use, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Dietary supplements industry

- 7.3 Functional foods & beverages

- 7.4 Clinical nutrition

- 7.5 Cosmetics & personal care

- 7.6 Animal nutrition & feed

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 DSM-Firmenich

- 9.2 Cargill, Incorporated

- 9.3 Archer Daniels Midland (ADM)

- 9.4 Kerry Group Plc

- 9.5 Chr. Hansen A/S (now Novonesis)

- 9.6 Immuse Health (Kirin Holdings/Kyowa Hakko Bio)

- 9.7 SCD Probiotics

- 9.8 Biofarma Group

- 9.9 Probi AB

- 9.10 Culturelle (i-Health, Inc.)

- 9.11 VSL Pharmaceuticals

- 9.12 Ritual

- 9.13 Metagenics